S-ar putea să vă placă și

- Forex A) Foreign Exchange Exposure and Risk Management: Prof. Archana KhetanDocument3 paginiForex A) Foreign Exchange Exposure and Risk Management: Prof. Archana KhetanTito BanerjeeÎncă nu există evaluări

- Forex 1 PDFDocument3 paginiForex 1 PDFgatÎncă nu există evaluări

- Forex A) Foreign Exchange Exposure and Risk Management: Prof. Archana KhetanDocument3 paginiForex A) Foreign Exchange Exposure and Risk Management: Prof. Archana KhetanTito BanerjeeÎncă nu există evaluări

- The Time Value of Money (Part Two)Document41 paginiThe Time Value of Money (Part Two)TakouhiÎncă nu există evaluări

- Answer FIN 401 Exam2 Fall15 V1Document7 paginiAnswer FIN 401 Exam2 Fall15 V1mahmudÎncă nu există evaluări

- Práctica 1 Fin I 2021Document2 paginiPráctica 1 Fin I 2021Brenda123Încă nu există evaluări

- Managerial Finance - Session 3Document6 paginiManagerial Finance - Session 3Ahmed el GhandourÎncă nu există evaluări

- Basic Long Term Financial Concepts Materials 4 4qDocument7 paginiBasic Long Term Financial Concepts Materials 4 4qJanna GunioÎncă nu există evaluări

- BBA VI Sem. - International Finance - Practical ProblemsDocument16 paginiBBA VI Sem. - International Finance - Practical ProblemsdeepeshmahajanÎncă nu există evaluări

- Business Finance - Loan AmortizationDocument30 paginiBusiness Finance - Loan AmortizationJo HarahÎncă nu există evaluări

- Activity Sheet In: Business FinanceDocument8 paginiActivity Sheet In: Business FinanceCatherine Larce100% (1)

- 03 - Time Value QDocument4 pagini03 - Time Value Qrehaliya15Încă nu există evaluări

- Problem Set 1 - Bonds and Time Value of MoneyDocument4 paginiProblem Set 1 - Bonds and Time Value of Moneymattgodftey1Încă nu există evaluări

- Business Finance: Basic Long-Term Financial ConceptsDocument33 paginiBusiness Finance: Basic Long-Term Financial ConceptsAce BautistaÎncă nu există evaluări

- Fin440 Chapter 6 v.2Document51 paginiFin440 Chapter 6 v.2Lutfun Nesa AyshaÎncă nu există evaluări

- Calculus For Business Part 2 Time Value of MoneyDocument2 paginiCalculus For Business Part 2 Time Value of MoneyGletzmar IgcasamaÎncă nu există evaluări

- Time Value of Money: Abm5 - Business FinanceDocument34 paginiTime Value of Money: Abm5 - Business FinanceBarbie BleuÎncă nu există evaluări

- Summative Gen Math 1 KeyDocument4 paginiSummative Gen Math 1 KeyJohn Mar CeaÎncă nu există evaluări

- SFM GRP 3Document108 paginiSFM GRP 3anisasheikh83Încă nu există evaluări

- Final Exam Review QuestionsDocument18 paginiFinal Exam Review QuestionsArchiePatelÎncă nu există evaluări

- Questions and AnswersDocument3 paginiQuestions and AnswersSenelwa AnayaÎncă nu există evaluări

- Lecture10 ES301 Engineering EconomicsDocument21 paginiLecture10 ES301 Engineering EconomicsLory Liza Bulay-ogÎncă nu există evaluări

- Effective Annual Rate (EAR)Document4 paginiEffective Annual Rate (EAR)abdiel100% (1)

- The Time Value of Money (Part Two)Document41 paginiThe Time Value of Money (Part Two)Karthik HegdeÎncă nu există evaluări

- Chapter 4Document50 paginiChapter 422GayeonÎncă nu există evaluări

- Mid TermAnswersDocument9 paginiMid TermAnswersMoulee DattaÎncă nu există evaluări

- Lab Solutions - Chapter 5 and 7Document5 paginiLab Solutions - Chapter 5 and 7Abdullah alhamaadÎncă nu există evaluări

- Business Finance WorksheetsDocument9 paginiBusiness Finance WorksheetsShiny NatividadÎncă nu există evaluări

- TVM - Recap QuestionsDocument7 paginiTVM - Recap QuestionsLalalaÎncă nu există evaluări

- Solution Chapter 6 International FinanceDocument6 paginiSolution Chapter 6 International FinanceHương Lan TrịnhÎncă nu există evaluări

- Itech Tutoring Comm 308 BookletDocument117 paginiItech Tutoring Comm 308 BookletAytekin AkolÎncă nu există evaluări

- BES 001 ReviewDocument3 paginiBES 001 ReviewAC Joyce SaulÎncă nu există evaluări

- Practice Problems For Chapter 2Document5 paginiPractice Problems For Chapter 2Lacey Blankenship100% (2)

- FM CH - IiiDocument18 paginiFM CH - IiiGizaw BelayÎncă nu există evaluări

- Práctica 2 Fin I 2021Document4 paginiPráctica 2 Fin I 2021Brenda123Încă nu există evaluări

- General Quarter 2 - Week 2: ZZZZZZDocument14 paginiGeneral Quarter 2 - Week 2: ZZZZZZJakim LopezÎncă nu există evaluări

- ACCT1002 M3 Homework SolutionsDocument7 paginiACCT1002 M3 Homework SolutionsMadeline WheelerÎncă nu există evaluări

- 33 Comm 308 Final Exam (Summer 1 2018) SolutionsDocument13 pagini33 Comm 308 Final Exam (Summer 1 2018) SolutionsCarl-Henry FrancoisÎncă nu există evaluări

- Solutions For All Modules of FMDocument125 paginiSolutions For All Modules of FMAtul KashyapÎncă nu există evaluări

- Tutorial 2 Financial Management 1Document39 paginiTutorial 2 Financial Management 1VignashÎncă nu există evaluări

- Fin202 Quiz 2 QuestionsDocument3 paginiFin202 Quiz 2 QuestionsLe Thi Hong Anh K16HLÎncă nu există evaluări

- Problem ForexDocument8 paginiProblem ForexKushal SharmaÎncă nu există evaluări

- Test - Chapter 2 Time Value of MoneyDocument18 paginiTest - Chapter 2 Time Value of Moneyk60.2112150055Încă nu există evaluări

- Tut Lec 5 - Chap 80Document6 paginiTut Lec 5 - Chap 80Bella SeahÎncă nu există evaluări

- Wednesday WK 2Document35 paginiWednesday WK 2Smriti LalÎncă nu există evaluări

- INTERESTDocument25 paginiINTERESTabdiel50% (2)

- 4th QTR Week 4-5 - Time Value Money (Part 1)Document47 pagini4th QTR Week 4-5 - Time Value Money (Part 1)Nichole Joy XielSera TanÎncă nu există evaluări

- Activity 5Document5 paginiActivity 5Riane Angelie SaligÎncă nu există evaluări

- 302time Value of MoneyDocument69 pagini302time Value of MoneypujaadiÎncă nu există evaluări

- A Case Study On Time Value of Money.: Sakshi Bezalwar-09 MMS 1 (Div-A)Document10 paginiA Case Study On Time Value of Money.: Sakshi Bezalwar-09 MMS 1 (Div-A)Sakshi BezalwarÎncă nu există evaluări

- Accounting Concepts and Applications 11th Edition Albrecht Test Bank Full Chapter PDFDocument67 paginiAccounting Concepts and Applications 11th Edition Albrecht Test Bank Full Chapter PDFKristenGilbertpoir100% (13)

- Chapter 6 - Accounting and The Time Value of MoneyDocument96 paginiChapter 6 - Accounting and The Time Value of MoneyTyas Widyanti100% (2)

- Accounting Concepts and Applications 11th Edition Albrecht Test BankDocument78 paginiAccounting Concepts and Applications 11th Edition Albrecht Test Bankformeretdoveshipx9yi8100% (28)

- Contemporary Financial Management 13th Edition Moyer Solutions Manual 1Document36 paginiContemporary Financial Management 13th Edition Moyer Solutions Manual 1thomasbuckley11072002asg100% (25)

- Chapter 61674Document52 paginiChapter 61674ramana02Încă nu există evaluări

- Simple Annuities (Revised)Document6 paginiSimple Annuities (Revised)Juliana CanonigoÎncă nu există evaluări

- Homework Notes Unit 3 MBA 615Document9 paginiHomework Notes Unit 3 MBA 615Kevin NyasogoÎncă nu există evaluări

- BusinessFinance M7-EDITED Removed-1Document21 paginiBusinessFinance M7-EDITED Removed-1Darren PulidoÎncă nu există evaluări

- Financial Risk Management: A Simple IntroductionDe la EverandFinancial Risk Management: A Simple IntroductionEvaluare: 4.5 din 5 stele4.5/5 (7)

- Audit Report: Ca Kanika KhetanDocument14 paginiAudit Report: Ca Kanika KhetanChandreshÎncă nu există evaluări

- 36 Nature of Accounts As Per Traditional Modern ApproachDocument2 pagini36 Nature of Accounts As Per Traditional Modern ApproachChandresh100% (1)

- AccountancyDocument40 paginiAccountancydher1234Încă nu există evaluări

- Hsslive Xii Ch1 Accouting For Nop Organisation SignedDocument4 paginiHsslive Xii Ch1 Accouting For Nop Organisation SignedChandreshÎncă nu există evaluări

- Ipcc Acc 28 Sep 2015 PDFDocument16 paginiIpcc Acc 28 Sep 2015 PDFChandreshÎncă nu există evaluări

- Hsslive-Chapter 2 Theory Base of Acc 1Document5 paginiHsslive-Chapter 2 Theory Base of Acc 1ChandreshÎncă nu există evaluări

- BrochureDocument2 paginiBrochureChandreshÎncă nu există evaluări

- Accounting For Non-Profit Organization: Presenting by Mohammed Nasih B.MDocument8 paginiAccounting For Non-Profit Organization: Presenting by Mohammed Nasih B.MChandreshÎncă nu există evaluări

- Retirement and Death of A PartnerDocument25 paginiRetirement and Death of A PartnerChandreshÎncă nu există evaluări

- Hsslive XII Accountancy Ch1 Not For Profit OrganizationDocument4 paginiHsslive XII Accountancy Ch1 Not For Profit OrganizationChandreshÎncă nu există evaluări

- Marathon Batch Final With Cover and Index PDFDocument106 paginiMarathon Batch Final With Cover and Index PDFChandreshÎncă nu există evaluări

- Joint Venture AccountsDocument17 paginiJoint Venture AccountsChandreshÎncă nu există evaluări

- Hsslive-Chapter 12 Not For Profit OrganisationsDocument7 paginiHsslive-Chapter 12 Not For Profit OrganisationsChandreshÎncă nu există evaluări

- Declaration and Payment of DividendDocument5 paginiDeclaration and Payment of DividendChandreshÎncă nu există evaluări

- As-1 and As-2 Summary NotesDocument7 paginiAs-1 and As-2 Summary NotesChandreshÎncă nu există evaluări

- Accountancy Ebook - Class 12 - Part 1 PDFDocument130 paginiAccountancy Ebook - Class 12 - Part 1 PDFChandreshÎncă nu există evaluări

- As Quick PDFDocument23 paginiAs Quick PDFChandreshÎncă nu există evaluări

- Unit 13 Joint Venture Accounts: 13.0 ObjectivesDocument22 paginiUnit 13 Joint Venture Accounts: 13.0 ObjectivesChandreshÎncă nu există evaluări

- CA IPCC Costing & FM Quick Revision NotesDocument21 paginiCA IPCC Costing & FM Quick Revision NotesChandreshÎncă nu există evaluări

- CA IPC Capital Budgeting Most Important Questions 1TR8KKBFDocument12 paginiCA IPC Capital Budgeting Most Important Questions 1TR8KKBFChandreshÎncă nu există evaluări

- How Can Calculate Exchange RateDocument12 paginiHow Can Calculate Exchange RateHoney SinghÎncă nu există evaluări

- FX MarketsDocument59 paginiFX MarketsAndreea Zamfir100% (1)

- Efficient Replication of Factor ReturnsDocument19 paginiEfficient Replication of Factor Returnstachyon007_mechÎncă nu există evaluări

- Financial Performance Evaluation of Some Selected Jordanian Commercial BanksDocument14 paginiFinancial Performance Evaluation of Some Selected Jordanian Commercial BanksAtiaTahiraÎncă nu există evaluări

- Chemfab Alkalies PDFDocument118 paginiChemfab Alkalies PDFSoundaryaÎncă nu există evaluări

- Bitcoin Price PredictionDocument3 paginiBitcoin Price PredictionAlaa' Deen ManasraÎncă nu există evaluări

- Malawi DeloitteDocument14 paginiMalawi DeloitteMwawiÎncă nu există evaluări

- Two Goals, Three Laws and Five Steps - Trading The Wyckoff MethodDocument14 paginiTwo Goals, Three Laws and Five Steps - Trading The Wyckoff MethodUDAYAN SHAH100% (1)

- Risk Management in Financial MarketDocument49 paginiRisk Management in Financial MarketAashika ShahÎncă nu există evaluări

- Euro Bond MarketDocument30 paginiEuro Bond MarketSharath PoojariÎncă nu există evaluări

- Prepared By: Puneet Sharma Vinay Patidar Viyappu Tharun Siddharth Khandelwal Rishu SinghDocument23 paginiPrepared By: Puneet Sharma Vinay Patidar Viyappu Tharun Siddharth Khandelwal Rishu SinghVasantha NaikÎncă nu există evaluări

- Societe Generale-Mind Matters-James Montier-Vanishing Value-Has The Market Rallied Too Far, Too Fast - 090520Document6 paginiSociete Generale-Mind Matters-James Montier-Vanishing Value-Has The Market Rallied Too Far, Too Fast - 090520yhlung2009Încă nu există evaluări

- ReturnDocument15 paginiReturnNurqasrina AisyahÎncă nu există evaluări

- IIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER ADocument88 paginiIIFL - India Info Line - FUNCTION'S OF STOCK MARKET IN INDIA (WITH RESPECT TO LEVEL OF CUSTOMER AVajir BajiÎncă nu există evaluări

- Comparative Performance Evaluation of Selected Mutual Funds in IndiaDocument80 paginiComparative Performance Evaluation of Selected Mutual Funds in IndiaManish GargÎncă nu există evaluări

- Finstreet - Finance Committee, Kjsimsr: Where Knowledge & Learning Are Key To SuccessDocument7 paginiFinstreet - Finance Committee, Kjsimsr: Where Knowledge & Learning Are Key To SuccessShalu PurswaniÎncă nu există evaluări

- High Frequency Trading: by Veloxpro Limited. Page 1 of 34Document34 paginiHigh Frequency Trading: by Veloxpro Limited. Page 1 of 34Karan Goyal100% (1)

- Private Placement MemorandumDocument12 paginiPrivate Placement MemorandumChrissy SabellaÎncă nu există evaluări

- Afm Revision NotesDocument50 paginiAfm Revision NotesNaomi KabutuÎncă nu există evaluări

- Nism Series XV - Research Analyst Certification ExamDocument17 paginiNism Series XV - Research Analyst Certification ExamRohit ShetÎncă nu există evaluări

- Foreign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ADocument3 paginiForeign Exchange Risk: Foreign Exchange Risk (Also Known As Exchange Rate Risk or Currency Risk) Is ASonali RawatÎncă nu există evaluări

- Chapter 9 Derivatives: Futures, Options, and Swaps: Multiple Choice QuestionsDocument34 paginiChapter 9 Derivatives: Futures, Options, and Swaps: Multiple Choice QuestionsKartikÎncă nu există evaluări

- DebaucheryDocument2 paginiDebaucheryDebolina DeyÎncă nu există evaluări

- Be Industrilization 2Document20 paginiBe Industrilization 2JAY SolankiÎncă nu există evaluări

- Chartered Wealth ManagerDocument4 paginiChartered Wealth ManagerKeith Parker100% (1)

- Dow Theory Letter 100708Document6 paginiDow Theory Letter 100708Richard Banks100% (1)

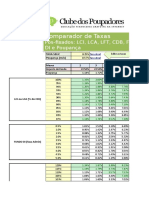

- CP Comparador de Taxas LCI LCA LFT CDB Poupanca FundosDIDocument5 paginiCP Comparador de Taxas LCI LCA LFT CDB Poupanca FundosDIeduardolavratiÎncă nu există evaluări

- Syailendra Fixed Income FundDocument1 paginăSyailendra Fixed Income FundJan KristantoÎncă nu există evaluări

- Andrew Lockwood: Trading Cheat SheetDocument18 paginiAndrew Lockwood: Trading Cheat SheetSifisoÎncă nu există evaluări

- BFS PracticeDocument61 paginiBFS PracticeBhagawath KishoreÎncă nu există evaluări