S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Value Added Tax (VAT) Number Registration / ApplicationDocument4 paginiValue Added Tax (VAT) Number Registration / ApplicationLedger Domains LLCÎncă nu există evaluări

- ,6ffiffi: The Municipat Council, BargarhDocument1 pagină,6ffiffi: The Municipat Council, BargarhGyana SahooÎncă nu există evaluări

- 7212 2022 CertificateDocument1 pagină7212 2022 CertificateGyana SahooÎncă nu există evaluări

- Ritu Department EXAMDocument1 paginăRitu Department EXAMGyana SahooÎncă nu există evaluări

- Letter TCS Emun HWDocument1 paginăLetter TCS Emun HWGyana SahooÎncă nu există evaluări

- Digital Photograph VIDEODocument4 paginiDigital Photograph VIDEOGyana SahooÎncă nu există evaluări

- Adobe Scan Nov 16, 2022Document1 paginăAdobe Scan Nov 16, 2022Gyana SahooÎncă nu există evaluări

- Pic Meeting Mom 5Document7 paginiPic Meeting Mom 5Gyana SahooÎncă nu există evaluări

- Downloads 15122015114324AMDocument4 paginiDownloads 15122015114324AMGyana SahooÎncă nu există evaluări

- TalcherDocument4 paginiTalcherGyana SahooÎncă nu există evaluări

- Labjam PDFDocument10 paginiLabjam PDFGyana SahooÎncă nu există evaluări

- Demo Ulb Municipality, Demoulb: Certificate of Holding TaxDocument1 paginăDemo Ulb Municipality, Demoulb: Certificate of Holding TaxGyana SahooÎncă nu există evaluări

- Unit 13 Digital Divide: StructureDocument14 paginiUnit 13 Digital Divide: StructureGyana SahooÎncă nu există evaluări

- Attendance May RabindraDocument1 paginăAttendance May RabindraGyana SahooÎncă nu există evaluări

- Effects of RF Interference: Aki HekkalaDocument18 paginiEffects of RF Interference: Aki HekkalaGyana SahooÎncă nu există evaluări

- Crimes and Torts Committed On A Computer Network and Realting To Electronic MailDocument15 paginiCrimes and Torts Committed On A Computer Network and Realting To Electronic MailGyana SahooÎncă nu există evaluări

- High Accuracy GPS and Antijam Protection Using A P (Y) Code Digital Beamsteering ReceiverDocument10 paginiHigh Accuracy GPS and Antijam Protection Using A P (Y) Code Digital Beamsteering ReceiverGyana SahooÎncă nu există evaluări

- 9909005Document6 pagini9909005Gyana SahooÎncă nu există evaluări

- Unit 3 Networking Concepts: StructureDocument12 paginiUnit 3 Networking Concepts: StructureGyana SahooÎncă nu există evaluări

- Linux Reference CardDocument3 paginiLinux Reference Cardvinoth_kumarss4961Încă nu există evaluări

- Unix Commands Cheat Sheet PDFDocument1 paginăUnix Commands Cheat Sheet PDFRosemond FabienÎncă nu există evaluări

- Introduction To Computer WrongsDocument12 paginiIntroduction To Computer WrongsGyana SahooÎncă nu există evaluări

- Promotions of Global CommonsDocument11 paginiPromotions of Global CommonsGyana SahooÎncă nu există evaluări

- International Treaties, Conventions and Protocols Concerning CyberspaceDocument13 paginiInternational Treaties, Conventions and Protocols Concerning CyberspaceGyana SahooÎncă nu există evaluări

- Linux Bash Shell Cheat SheetDocument7 paginiLinux Bash Shell Cheat SheetArdit MeziniÎncă nu există evaluări

- Unit 15 Open Source Movement: StructureDocument9 paginiUnit 15 Open Source Movement: StructureGyana SahooÎncă nu există evaluări

- Promotions of Global CommonsDocument11 paginiPromotions of Global CommonsGyana SahooÎncă nu există evaluări

- Prabhupad Mohapatra - WiproDocument6 paginiPrabhupad Mohapatra - WiproGyana SahooÎncă nu există evaluări

- Escalation MatrixDocument2 paginiEscalation MatrixGyana SahooÎncă nu există evaluări

- License Spiv 16090327 AusDocument3 paginiLicense Spiv 16090327 AusGyana SahooÎncă nu există evaluări

- Reward Current Account Statement: Nabeel AhmedDocument1 paginăReward Current Account Statement: Nabeel AhmedAlex Beldiman100% (1)

- Capital GainsDocument22 paginiCapital Gainssachinkumar3009Încă nu există evaluări

- Danny SyDocument2 paginiDanny SyJael AmorÎncă nu există evaluări

- AssignmentDocument5 paginiAssignmentSuyash PrakashÎncă nu există evaluări

- Tax Invoice: Page 1 of 2Document2 paginiTax Invoice: Page 1 of 2HamzaÎncă nu există evaluări

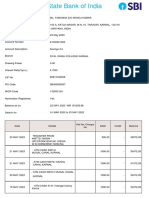

- State Bank of India PDFDocument1 paginăState Bank of India PDFSUDHANSHU KUMARÎncă nu există evaluări

- Training Registration FormDocument6 paginiTraining Registration FormRoka KaramÎncă nu există evaluări

- Cashier Data Flow DiagramDocument7 paginiCashier Data Flow DiagramashenÎncă nu există evaluări

- Wa0000.Document1 paginăWa0000.nikhil buddaÎncă nu există evaluări

- Booking Confirmation On IRCTC, Train: 12311, 16-Jul-2022, 2A, BWN - KKDEDocument1 paginăBooking Confirmation On IRCTC, Train: 12311, 16-Jul-2022, 2A, BWN - KKDEAtul GoyalÎncă nu există evaluări

- Unlock Instant Payment Use Cases With The Fednow ServiceDocument2 paginiUnlock Instant Payment Use Cases With The Fednow ServiceLaLa BanksÎncă nu există evaluări

- Cash & GB MCQ NEW ESKATON FDocument18 paginiCash & GB MCQ NEW ESKATON FJubaida Alam Juthy57% (7)

- Income Tax Calculator Fy 2021 22 v2Document11 paginiIncome Tax Calculator Fy 2021 22 v2yuvirocksÎncă nu există evaluări

- H&R Block Income Tax School: CatalogDocument17 paginiH&R Block Income Tax School: CatalogclaokerÎncă nu există evaluări

- Rajasthan Housing Board, Circle - Iii, JaipurDocument1 paginăRajasthan Housing Board, Circle - Iii, JaipuranilÎncă nu există evaluări

- 2.1 Income Tax - General PrinciplesDocument9 pagini2.1 Income Tax - General PrinciplesMarco RvsÎncă nu există evaluări

- Book 2Document1 paginăBook 2Kim MonteronaÎncă nu există evaluări

- Profits Tax IIIDocument159 paginiProfits Tax IIISin Yee FUNGÎncă nu există evaluări

- EXAMPLE 12.1 (Current Tax Liability)Document8 paginiEXAMPLE 12.1 (Current Tax Liability)KaiWenNgÎncă nu există evaluări

- Buslaw3 VATDocument58 paginiBuslaw3 VATVan TisbeÎncă nu există evaluări

- 142 CIR v. CitytrustDocument3 pagini142 CIR v. CitytrustclarkorjaloÎncă nu există evaluări

- Web Generated Bill: Feeder: Islamia Park Sub Division: Islamia Park Division: Civil LineDocument1 paginăWeb Generated Bill: Feeder: Islamia Park Sub Division: Islamia Park Division: Civil LineAkhtar AliÎncă nu există evaluări

- Seec F'orm 20Document23 paginiSeec F'orm 20The Valley IndyÎncă nu există evaluări

- Tamanna Sbi SDocument4 paginiTamanna Sbi SSajan SharmaÎncă nu există evaluări

- Residential Status and Incidence of Tax - Study MaterialDocument6 paginiResidential Status and Incidence of Tax - Study MaterialEmeline SoroÎncă nu există evaluări

- 21072023, 010608 PDFDocument2 pagini21072023, 010608 PDFCatalina-Elena100% (1)

- Final Tax ReviewerDocument35 paginiFinal Tax Revieweryza100% (1)

- CIR vs. LA FLOR DEla ISABELA, 2019Document3 paginiCIR vs. LA FLOR DEla ISABELA, 2019Fenina Reyes0% (1)

- Pakistan Custom Department MCQs For Appraising - Valuation Officer in BoR PDFDocument5 paginiPakistan Custom Department MCQs For Appraising - Valuation Officer in BoR PDFAamir ArainÎncă nu există evaluări