S-ar putea să vă placă și

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Definition of The 'Going Concern' Concept: AccountingDocument4 paginiDefinition of The 'Going Concern' Concept: Accountingmhrscribd014Încă nu există evaluări

- Capital Expenditure: AccountancyDocument3 paginiCapital Expenditure: Accountancymhrscribd014100% (1)

- Compound Interest: The Mathematical Constant eDocument33 paginiCompound Interest: The Mathematical Constant emhrscribd014Încă nu există evaluări

- Balance SheetDocument7 paginiBalance Sheetmhrscribd014Încă nu există evaluări

- Accrual: AccountancyDocument8 paginiAccrual: Accountancymhrscribd014Încă nu există evaluări

- Yarn Count & Yarn ModificationDocument52 paginiYarn Count & Yarn Modificationmhrscribd014Încă nu există evaluări

- Presentation ShrinkageDocument27 paginiPresentation Shrinkagemhrscribd014Încă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

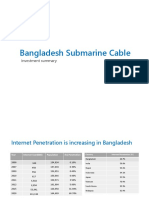

- Bangladesh Submarine Cable (Investment Summary)Document21 paginiBangladesh Submarine Cable (Investment Summary)hossainboxÎncă nu există evaluări

- Harley Davidson Strategic Management Changed NewDocument33 paginiHarley Davidson Strategic Management Changed NewDevina GuptaÎncă nu există evaluări

- 2010 OCBC Cycle Singapore To Follow Route of YOG Road Race, 15 Oct 2009, Business TimesDocument1 pagină2010 OCBC Cycle Singapore To Follow Route of YOG Road Race, 15 Oct 2009, Business TimesdbmcysÎncă nu există evaluări

- HO HUP Analysis K.ani 2Document10 paginiHO HUP Analysis K.ani 2Ummi AniÎncă nu există evaluări

- 01 Chapter 1Document26 pagini01 Chapter 1Ñagáşaï BøïnâÎncă nu există evaluări

- Financial Accounting and Accounting StandardDocument18 paginiFinancial Accounting and Accounting StandardZahidnsuÎncă nu există evaluări

- Larry Pesavento Fibonacci Ratios With Pattern Recognition Traders PDFDocument184 paginiLarry Pesavento Fibonacci Ratios With Pattern Recognition Traders PDFassas100% (2)

- Cost of Capital - The Effect To The Firm Value and Profitability Empirical Evidences in Case of Personal Goods (Textile) Sector of KSE 100 IndexDocument7 paginiCost of Capital - The Effect To The Firm Value and Profitability Empirical Evidences in Case of Personal Goods (Textile) Sector of KSE 100 IndexKanganFatimaÎncă nu există evaluări

- Dissertation On ULIPDocument30 paginiDissertation On ULIPRakesh RajputÎncă nu există evaluări

- C FlorioDocument18 paginiC FlorioDewi DarmastutiÎncă nu există evaluări

- BP Report NewDocument22 paginiBP Report NewKatie WilliamsÎncă nu există evaluări

- Cash Flow of Southwest AirlinesDocument4 paginiCash Flow of Southwest AirlinessumitÎncă nu există evaluări

- Mar-15 Mar-16 Mar-17 Mar-18 Mar-19 Trailing Best Case Worst CaseDocument9 paginiMar-15 Mar-16 Mar-17 Mar-18 Mar-19 Trailing Best Case Worst CaseYASH KOTHARIÎncă nu există evaluări

- Investment in Equity Securities 2Document2 paginiInvestment in Equity Securities 2miss independentÎncă nu există evaluări

- Chardan UniverseDocument5 paginiChardan UniverseAnonymous 6tuR1hzÎncă nu există evaluări

- Secretarial PracticeDocument5 paginiSecretarial PracticeAMIN BUHARI ABDUL KHADER100% (1)

- IFRS13 Fair Value MeasurementDocument79 paginiIFRS13 Fair Value MeasurementAnep ZainuldinÎncă nu există evaluări

- RIL RightsDocument16 paginiRIL Rightsprajakt_pieÎncă nu există evaluări

- Akancha Agarwal - Prof. S. TagareDocument44 paginiAkancha Agarwal - Prof. S. TagareGunadeep ReddyÎncă nu există evaluări

- Total Form 20-FDocument424 paginiTotal Form 20-FedgarmerchanÎncă nu există evaluări

- Ebs FMS IDocument16 paginiEbs FMS IRoshni VargheseÎncă nu există evaluări

- Investor PresDocument24 paginiInvestor PresHungreo411Încă nu există evaluări

- Seminar Report McomDocument17 paginiSeminar Report Mcommansingh_smaranikaÎncă nu există evaluări

- Stock Index FuturesDocument4 paginiStock Index FutureswannaflynowÎncă nu există evaluări

- Bustos vs. Millians Shoe, Inc.Document4 paginiBustos vs. Millians Shoe, Inc.Francis Coronel Jr.100% (1)

- Rating of Indian Commercial Banks: A DEA Approach: Asish Saha, T.S. RavisankarDocument17 paginiRating of Indian Commercial Banks: A DEA Approach: Asish Saha, T.S. RavisankarSaurabh SuryavanshiÎncă nu există evaluări

- Project IRR Equity IRRDocument35 paginiProject IRR Equity IRRsandeepniftianÎncă nu există evaluări

- Credit Risk Analysis - Janani PrakashDocument46 paginiCredit Risk Analysis - Janani PrakashJanani Prakash87% (15)

- ReportDocument3 paginiReportnancysinglaÎncă nu există evaluări

- Betting Against BetaDocument25 paginiBetting Against BetamÎncă nu există evaluări