S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- CCL Products India: PrintDocument2 paginiCCL Products India: PrintSaurabh RajÎncă nu există evaluări

- Session 3: The Entrepreneur Tracking His ResourcesDocument36 paginiSession 3: The Entrepreneur Tracking His ResourcesRose Mae TabayoyongÎncă nu există evaluări

- SBR NoteDocument20 paginiSBR NotechuwenÎncă nu există evaluări

- Financial Results, Form A For March 31, 2016 (Result)Document13 paginiFinancial Results, Form A For March 31, 2016 (Result)Shyam SunderÎncă nu există evaluări

- Financial ProjectionDocument55 paginiFinancial ProjectionVinayak SilverlineswapÎncă nu există evaluări

- Corporate Liquidation & Joint Venture2Document5 paginiCorporate Liquidation & Joint Venture2jjjjjjjjjjjjjjjÎncă nu există evaluări

- Introduction To Accounting and Business: Question InformationDocument56 paginiIntroduction To Accounting and Business: Question InformationSivakumar KanchirajuÎncă nu există evaluări

- Property, Plant & Equipment (Fixed Assets) : Reeve Warren DuchacDocument33 paginiProperty, Plant & Equipment (Fixed Assets) : Reeve Warren Duchacyow jing peiÎncă nu există evaluări

- Ssignment RiefDocument6 paginiSsignment RiefShah MuradÎncă nu există evaluări

- Advanced - Yr 2022 Audited AccountsDocument22 paginiAdvanced - Yr 2022 Audited AccountswolekniceÎncă nu există evaluări

- BF BinderDocument7 paginiBF BinderShane VeiraÎncă nu există evaluări

- Company Limited: "We Foster Rich Customer Service"Document7 paginiCompany Limited: "We Foster Rich Customer Service"delrose delgadoÎncă nu există evaluări

- Substantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Document38 paginiSubstantive Test of Intangible Assets, Prepaid Expenses (Autosaved)Mej AgaoÎncă nu există evaluări

- Final Grading Examination Key AnswersDocument22 paginiFinal Grading Examination Key AnswersKimÎncă nu există evaluări

- At Tahur LimitedDocument24 paginiAt Tahur Limitedcristiano ronaldooÎncă nu există evaluări

- JU Penjahit YantiDocument14 paginiJU Penjahit Yantiecjeb100% (2)

- ACT Assignment FullDocument16 paginiACT Assignment Fullsadif sayeed100% (3)

- Accounting RTPDocument40 paginiAccounting RTPMayur KundarÎncă nu există evaluări

- Business Combi and Conso HandoutDocument16 paginiBusiness Combi and Conso HandoutKarlo Jude Acidera100% (2)

- SSR Stock Analysis SpreadsheetDocument33 paginiSSR Stock Analysis Spreadsheetpvenky100% (1)

- Intangible Asset (Pas 38) : Introduction, Scope and DefinitionsDocument20 paginiIntangible Asset (Pas 38) : Introduction, Scope and Definitionskeithy joshuaÎncă nu există evaluări

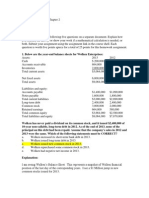

- FIN 534 Homework Chap.2Document3 paginiFIN 534 Homework Chap.2Jenna KiragisÎncă nu există evaluări

- Report On Asian PaintsDocument10 paginiReport On Asian PaintsMukul AgarwalÎncă nu există evaluări

- Accounting Chapter 3 SummaryDocument7 paginiAccounting Chapter 3 SummaryHariÎncă nu există evaluări

- CH 04Document40 paginiCH 04Melanie SamsonaÎncă nu există evaluări

- 111 0404Document36 pagini111 0404api-27548664Încă nu există evaluări

- 3-Statement Model (Complete)Document16 pagini3-Statement Model (Complete)James BondÎncă nu există evaluări

- Pusing Rhezel - UNIT V - Learning Activity 5 - Exercise 5 - Closing Entries - Post Closing Trial Balance - Opening EntryDocument2 paginiPusing Rhezel - UNIT V - Learning Activity 5 - Exercise 5 - Closing Entries - Post Closing Trial Balance - Opening EntryRhezel Baroro Pusing100% (2)

- Accountancy Review Center (ARC) of The Philippines Inc.: Student HandoutsDocument5 paginiAccountancy Review Center (ARC) of The Philippines Inc.: Student HandoutsRÎncă nu există evaluări

- Adjustments of Final AccountsDocument11 paginiAdjustments of Final AccountsUmesh Gaikwad50% (10)