S-ar putea să vă placă și

- Junk to Gold: From Salvage to the World’S Largest Online Auto AuctionDe la EverandJunk to Gold: From Salvage to the World’S Largest Online Auto AuctionEvaluare: 5 din 5 stele5/5 (2)

- The Security I Like BestDocument7 paginiThe Security I Like Bestneo269100% (4)

- Cfas Quiz 1 2 3 4Document47 paginiCfas Quiz 1 2 3 4JONATHAN LANCE JOBLEÎncă nu există evaluări

- 2009 Annual LetterDocument5 pagini2009 Annual Letterppate100% (1)

- Lisa Rapuano Finding Your Way Along The Many Paths of ValueDocument29 paginiLisa Rapuano Finding Your Way Along The Many Paths of ValueValueWalk100% (1)

- Ek VLDocument1 paginăEk VLJohn Aldridge ChewÎncă nu există evaluări

- Michael Burry Write Ups From 2000Document27 paginiMichael Burry Write Ups From 2000Patrick LangstromÎncă nu există evaluări

- Bridge With Buffett A Mathematician On Wall StreetDocument3 paginiBridge With Buffett A Mathematician On Wall StreetgjangÎncă nu există evaluări

- Distressed Investment Banking - To the Abyss and Back - Second EditionDe la EverandDistressed Investment Banking - To the Abyss and Back - Second EditionÎncă nu există evaluări

- Risk. Reward. Repeat.: How I Succeeded and How You Can TooDe la EverandRisk. Reward. Repeat.: How I Succeeded and How You Can TooÎncă nu există evaluări

- Grant Article On Henry SingletonDocument4 paginiGrant Article On Henry SingletonYashÎncă nu există evaluări

- Venture Capital 101Document20 paginiVenture Capital 101jhmedvedÎncă nu există evaluări

- Intermediate Accounting 1 Final Grading ExaminationDocument18 paginiIntermediate Accounting 1 Final Grading ExaminationKrissa Mae LongosÎncă nu există evaluări

- Unit 1 WORKING CAPITAL MGTDocument22 paginiUnit 1 WORKING CAPITAL MGTsanthosh prabhu mÎncă nu există evaluări

- Aquamarine Fund PresentationDocument25 paginiAquamarine Fund PresentationVijay MalikÎncă nu există evaluări

- The 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy HimDocument5 paginiThe 400% Man: How A College Dropout at A Tiny Utah Fund Beat Wall Street, and Why Most Managers Are Scared To Copy Himrakeshmoney99Încă nu există evaluări

- Office Hours With Warren Buffett May 2013Document11 paginiOffice Hours With Warren Buffett May 2013jkusnan3341Încă nu există evaluări

- Teledyne and Henry Singleton A CS of A Great Capital AllocatorDocument34 paginiTeledyne and Henry Singleton A CS of A Great Capital Allocatorp_rishi_2000Încă nu există evaluări

- Thomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Document34 paginiThomas Russo: Global Value Investing - Richard Ivey School of Business, 2013Hedge Fund ConversationsÎncă nu există evaluări

- Bob Robotti - Navigating Deep WatersDocument35 paginiBob Robotti - Navigating Deep WatersCanadianValue100% (1)

- Decision-Making For Investors: Theory, Practice, and PitfallsDocument20 paginiDecision-Making For Investors: Theory, Practice, and PitfallsGaurav JainÎncă nu există evaluări

- David Tepper S 2007 Presentation at Carnegie Mellon PDFDocument7 paginiDavid Tepper S 2007 Presentation at Carnegie Mellon PDFPattyPattersonÎncă nu există evaluări

- Max Heine Forbes March 29 1982Document2 paginiMax Heine Forbes March 29 1982jkusnan3341100% (2)

- The Future of Common Stocks Benjamin Graham PDFDocument8 paginiThe Future of Common Stocks Benjamin Graham PDFPrashant AgarwalÎncă nu există evaluări

- Klarman Yield PigDocument2 paginiKlarman Yield Pigalexg6Încă nu există evaluări

- 8th Annual New York: Value Investing CongressDocument46 pagini8th Annual New York: Value Investing CongressVALUEWALK LLCÎncă nu există evaluări

- Arlington Value 2016 Annual Letter PDFDocument6 paginiArlington Value 2016 Annual Letter PDFChrisÎncă nu există evaluări

- Boyar's Intrinsic Value Research Forgotten FourtyDocument49 paginiBoyar's Intrinsic Value Research Forgotten FourtyValueWalk100% (1)

- Graham and Doddsville - Issue 9 - Spring 2010Document33 paginiGraham and Doddsville - Issue 9 - Spring 2010g4nz0Încă nu există evaluări

- Clear Thinking About Share RepurchaseDocument29 paginiClear Thinking About Share RepurchaseVrtpy CiurbanÎncă nu există evaluări

- Arlington Value 2014 Annual Letter PDFDocument8 paginiArlington Value 2014 Annual Letter PDFChrisÎncă nu există evaluări

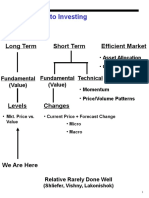

- Approaches To Investing: Long Term Short Term Efficient MarketDocument71 paginiApproaches To Investing: Long Term Short Term Efficient MarketPeter WarmeÎncă nu există evaluări

- Warren Buffett and GEICO Case StudyDocument18 paginiWarren Buffett and GEICO Case StudyReymond Jude PagcoÎncă nu există evaluări

- Templeton ProcessDocument42 paginiTempleton ProcessFrederico DimarzioÎncă nu există evaluări

- Chuck Akre Value Investing Conference Talk - 'An Investor's Odyssey - The Search For Outstanding Investments' PDFDocument10 paginiChuck Akre Value Investing Conference Talk - 'An Investor's Odyssey - The Search For Outstanding Investments' PDFSunil ParikhÎncă nu există evaluări

- Focus InvestorDocument5 paginiFocus Investora65b66inc7288Încă nu există evaluări

- Aquamarine - 2013Document84 paginiAquamarine - 2013sb86Încă nu există evaluări

- ValuationsDocument27 paginiValuationsblabitan100% (1)

- Carl Icahn's Letter To Apple's Tim CookDocument4 paginiCarl Icahn's Letter To Apple's Tim CookCanadianValueÎncă nu există evaluări

- Scott Miller of Greenhaven Road Capital: Long On Zix CorpDocument0 paginiScott Miller of Greenhaven Road Capital: Long On Zix CorpcurrygoatÎncă nu există evaluări

- Allan Mecham Interview PDFDocument6 paginiAllan Mecham Interview PDFRajeev BahugunaÎncă nu există evaluări

- Nick Train The King of Buy and HoldDocument13 paginiNick Train The King of Buy and HoldkessbrokerÎncă nu există evaluări

- Securities in An Insecure World - Benjamin GrahamDocument14 paginiSecurities in An Insecure World - Benjamin Grahamneo269100% (3)

- Graham Doddsville Issue 24Document61 paginiGraham Doddsville Issue 24CanadianValueÎncă nu există evaluări

- Mick McGuire Value Investing Congress Presentation Marcato Capital ManagementDocument70 paginiMick McGuire Value Investing Congress Presentation Marcato Capital Managementmarketfolly.comÎncă nu există evaluări

- 8th Annual New York: Value Investing CongressDocument53 pagini8th Annual New York: Value Investing CongressVALUEWALK LLCÎncă nu există evaluări

- Profit Guru Bill NygrenDocument5 paginiProfit Guru Bill NygrenekramcalÎncă nu există evaluări

- Murray Stahl - Value - Investor - May - 2013 PDFDocument10 paginiMurray Stahl - Value - Investor - May - 2013 PDFkdwcapitalÎncă nu există evaluări

- Hayman Bass 20081017Document3 paginiHayman Bass 20081017dylan555100% (1)

- Austrian Economics & InvestingDocument20 paginiAustrian Economics & InvestingRaj KumarÎncă nu există evaluări

- Sealed Air Case Study - HandoutDocument17 paginiSealed Air Case Study - HandoutJohn Aldridge ChewÎncă nu există evaluări

- BerkshireHandout2012Final 0 PDFDocument4 paginiBerkshireHandout2012Final 0 PDFHermes TristemegistusÎncă nu există evaluări

- SchlossDocument188 paginiSchlossEduardo FreitasÎncă nu există evaluări

- Mick McGuire Value Investing Congress Presentation Marcato Capital ManagementDocument70 paginiMick McGuire Value Investing Congress Presentation Marcato Capital ManagementscottleeyÎncă nu există evaluări

- Finding Value Amoung The Lows The Walter J Schloss ApproachDocument2 paginiFinding Value Amoung The Lows The Walter J Schloss ApproachrlmohlaÎncă nu există evaluări

- H. Kevin Byun's Q4 2013 Denali Investors LetterDocument4 paginiH. Kevin Byun's Q4 2013 Denali Investors LetterValueInvestingGuy100% (1)

- Lou Simpson 5 Investing PrinciplesDocument4 paginiLou Simpson 5 Investing Principlesevolve_usÎncă nu există evaluări

- Book Recommendations From Legendary Investors PDFDocument6 paginiBook Recommendations From Legendary Investors PDFDevendra GhodkeÎncă nu există evaluări

- Buffett On ValuationDocument7 paginiBuffett On ValuationAyush AggarwalÎncă nu există evaluări

- The Art of Vulture Investing: Adventures in Distressed Securities ManagementDe la EverandThe Art of Vulture Investing: Adventures in Distressed Securities ManagementÎncă nu există evaluări

- Tech Stock Valuation: Investor Psychology and Economic AnalysisDe la EverandTech Stock Valuation: Investor Psychology and Economic AnalysisEvaluare: 4 din 5 stele4/5 (1)

- The Value Proposition: Sionna's Common Sense Path to Investment SuccessDe la EverandThe Value Proposition: Sionna's Common Sense Path to Investment SuccessÎncă nu există evaluări

- RC&G Transcript 2018Document28 paginiRC&G Transcript 2018YashÎncă nu există evaluări

- Leon Cooperman Value Investing Congress Henry Singleton PDFDocument37 paginiLeon Cooperman Value Investing Congress Henry Singleton PDFYashÎncă nu există evaluări

- Pricing PowerDocument13 paginiPricing PowerYashÎncă nu există evaluări

- Capitalizing Operating Leases (No Principal Reduction)Document3 paginiCapitalizing Operating Leases (No Principal Reduction)PogotoshÎncă nu există evaluări

- 1979 Letter To Shareholders - Berkshire HathawayDocument9 pagini1979 Letter To Shareholders - Berkshire HathawayYashÎncă nu există evaluări

- 1978 Letter To Shareholders - Berkshire HathawayDocument6 pagini1978 Letter To Shareholders - Berkshire HathawayYashÎncă nu există evaluări

- Buffet 1977Document7 paginiBuffet 1977spogoliÎncă nu există evaluări

- Corporate Law ProjectDocument15 paginiCorporate Law ProjectShaurya AronÎncă nu există evaluări

- AFAR 2305 Not-for-Profit OrganizationsDocument14 paginiAFAR 2305 Not-for-Profit OrganizationsDzulija TalipanÎncă nu există evaluări

- Project On Ratio Analysis and DCF Model of Mazagaon Dock Shipbuilders LimitedDocument6 paginiProject On Ratio Analysis and DCF Model of Mazagaon Dock Shipbuilders LimitedChriselle D'souzaÎncă nu există evaluări

- 12linsteel Book of Account DecemberDocument54 pagini12linsteel Book of Account DecemberCarlos_CriticaÎncă nu există evaluări

- Lucknow Seission Ending Project 2021-22 Name:Aditi Shukla Class:Xith-D Roll No:04 Submitted To: MR - Kush SrivastavaDocument24 paginiLucknow Seission Ending Project 2021-22 Name:Aditi Shukla Class:Xith-D Roll No:04 Submitted To: MR - Kush SrivastavaAdisha's100% (1)

- Kotak securities-PandL 2022-23 RRGDocument5 paginiKotak securities-PandL 2022-23 RRGRg RrgÎncă nu există evaluări

- Answer To MTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial AccountingDocument17 paginiAnswer To MTP - Intermediate - Syllabus 2016 - June2020 - Set1: Paper 5-Financial AccountingMohit SangwanÎncă nu există evaluări

- NISM Series III A Securities Intermediaries Compliance NF Certication ExamDocument222 paginiNISM Series III A Securities Intermediaries Compliance NF Certication ExamNIFM PGDMFÎncă nu există evaluări

- 0.80 Points: AwardDocument21 pagini0.80 Points: AwardhirevÎncă nu există evaluări

- Use The Following Information For The Next Four Cases:: Depreciation Methods Fact PatternDocument6 paginiUse The Following Information For The Next Four Cases:: Depreciation Methods Fact PatternPRESCIOUS JOY CERALDEÎncă nu există evaluări

- Subsequent Acquisition PDFDocument21 paginiSubsequent Acquisition PDFEvangeline WongÎncă nu există evaluări

- Gann CoursesDocument3 paginiGann CoursesKirtan Balkrishna RautÎncă nu există evaluări

- BFM - Mod - DDocument67 paginiBFM - Mod - DAbhishek KumarÎncă nu există evaluări

- Itc Clsa Oct2020Document100 paginiItc Clsa Oct2020ksatishbabuÎncă nu există evaluări

- Format of Entries of Standard Costing-Chap 20Document9 paginiFormat of Entries of Standard Costing-Chap 20Muhammad azeemÎncă nu există evaluări

- Module For AccountingDocument46 paginiModule For AccountingJhefz KhurtzÎncă nu există evaluări

- TATA Motors Final AccountsDocument4 paginiTATA Motors Final AccountsjayanathÎncă nu există evaluări

- New Folder - AUD - AUD-1 OutlineDocument9 paginiNew Folder - AUD - AUD-1 OutlineDaljeet SinghÎncă nu există evaluări

- Cost Accounting Labor Costs AssignmentDocument3 paginiCost Accounting Labor Costs AssignmentGabriel EvannÎncă nu există evaluări

- Questions For Solving Case Study of Anandam MFG CoDocument3 paginiQuestions For Solving Case Study of Anandam MFG CoSubodh Sahastrabuddhe100% (1)

- Corporation Issuance of Shares Illutsrative ProblemDocument15 paginiCorporation Issuance of Shares Illutsrative ProblemHoney MuliÎncă nu există evaluări

- NBFC Thematic On Securitisation - Spark - 25nov19Document35 paginiNBFC Thematic On Securitisation - Spark - 25nov19chetankvoraÎncă nu există evaluări

- Brief Description On The CompanyDocument4 paginiBrief Description On The CompanyDuong Trinh MinhÎncă nu există evaluări

- 11 Ashok Leyland HosurDocument67 pagini11 Ashok Leyland HosurJ N PradeepÎncă nu există evaluări

- Topic 8 - IAS 8 (Eng)Document19 paginiTopic 8 - IAS 8 (Eng)Alisa OrÎncă nu există evaluări