S-ar putea să vă placă și

- The PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingDocument98 paginiThe PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingJhopel Casagnap EmanÎncă nu există evaluări

- Overview Obnbn PPSASDocument44 paginiOverview Obnbn PPSASJenofDulwn0% (1)

- Registry of Allotments and Notice of Transfer of Allocation: Appendix 31Document1 paginăRegistry of Allotments and Notice of Transfer of Allocation: Appendix 31Tesa GDÎncă nu există evaluări

- GaDocument39 paginiGaRomeo Baldevia100% (1)

- 01-BacarraIN2020 Audit ReportDocument91 pagini01-BacarraIN2020 Audit ReportRichard MendezÎncă nu există evaluări

- 20% Devt FundDocument18 pagini20% Devt Fundvangie100% (1)

- Antipolo Rizal Budget 2022Document59 paginiAntipolo Rizal Budget 2022Kakam PwetÎncă nu există evaluări

- Independent: Auditor'S ReportDocument3 paginiIndependent: Auditor'S ReportRene Huyo-aÎncă nu există evaluări

- The City of CAUAYAN, IsABELA Investment Incentive CodeDocument18 paginiThe City of CAUAYAN, IsABELA Investment Incentive CodeDon Vincent Bautista BustoÎncă nu există evaluări

- PPSAS 1 & PPSAS 33-Presentation of FS and First Time Adoption of Accrual - For AGIADocument72 paginiPPSAS 1 & PPSAS 33-Presentation of FS and First Time Adoption of Accrual - For AGIALyka Mae Palarca Irang100% (1)

- Manual On Financial Management of Barangays MODULE 2Document29 paginiManual On Financial Management of Barangays MODULE 2vicsÎncă nu există evaluări

- SAOR 2015 Additional AOM DO ZDNDocument9 paginiSAOR 2015 Additional AOM DO ZDNrussel1435Încă nu există evaluări

- Goldilocks LetterDocument1 paginăGoldilocks LetterPhilippe CamposanoÎncă nu există evaluări

- AOM No. 2022-001 (20-22) - Audit of Accounts and Transactions Brgy. Salinas, BambangDocument24 paginiAOM No. 2022-001 (20-22) - Audit of Accounts and Transactions Brgy. Salinas, BambangGilbert D. AfallaÎncă nu există evaluări

- Job OrderDocument1 paginăJob OrderMARIFA ROSEROÎncă nu există evaluări

- Sample Finding On Unreleased ChecksDocument1 paginăSample Finding On Unreleased ChecksJan QuÎncă nu există evaluări

- 1-Connecting Plans To The BudgetDocument81 pagini1-Connecting Plans To The BudgetJamy Vab MontesÎncă nu există evaluări

- 3 Kmac AuthorizationDocument40 pagini3 Kmac AuthorizationJamy Vab MontesÎncă nu există evaluări

- Budget Preparation: Republic of The Philippines Department of Budget and ManagementDocument55 paginiBudget Preparation: Republic of The Philippines Department of Budget and ManagementFernando ComedoyÎncă nu există evaluări

- Budget Authorization: Budget Operations Manual For BarangaysDocument72 paginiBudget Authorization: Budget Operations Manual For BarangaysNonielyn Sabornido100% (1)

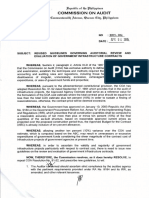

- COA CIRCULAR NO. 2024 006 March 14 2024Document21 paginiCOA CIRCULAR NO. 2024 006 March 14 2024Jen IgnacioÎncă nu există evaluări

- Prescribing The Use of IASPPS & ICS For PPSDocument6 paginiPrescribing The Use of IASPPS & ICS For PPSJulie Khristine Panganiban100% (1)

- Ms. Angeles A. MarallagDocument6 paginiMs. Angeles A. MarallaggilbertÎncă nu există evaluări

- Audit of Confidential Fund of LGUDocument16 paginiAudit of Confidential Fund of LGUBarwin Scott VillordonÎncă nu există evaluări

- Draft AOM On 20% DevelopmentDocument4 paginiDraft AOM On 20% DevelopmentWilliam A. Chakas Jr.Încă nu există evaluări

- A1 - ICQ Agency Level ControlsDocument7 paginiA1 - ICQ Agency Level ControlsReihannah Paguital-MagnoÎncă nu există evaluări

- Annual Audit Report: Republic of The Philippines Commission On Audit Regional Office No. IX Zamboanga CityDocument8 paginiAnnual Audit Report: Republic of The Philippines Commission On Audit Regional Office No. IX Zamboanga CityJuan Luis LusongÎncă nu există evaluări

- AA 4102 1st Hand OutDocument9 paginiAA 4102 1st Hand OutMana XDÎncă nu există evaluări

- COA - Unnumbered - Memo (OJE & JET)Document5 paginiCOA - Unnumbered - Memo (OJE & JET)Kaitou Kuroba100% (1)

- Appendix 30 - Instructions - RANCADocument1 paginăAppendix 30 - Instructions - RANCApdmu regionixÎncă nu există evaluări

- Features of The Government Accounting Manual For National Government AgenciesDocument30 paginiFeatures of The Government Accounting Manual For National Government AgenciesMay Joy ManagdagÎncă nu există evaluări

- Angsamoro: Section 1. Composition MPDCDocument4 paginiAngsamoro: Section 1. Composition MPDCAbdel-ashri HadjinullaÎncă nu există evaluări

- Barangay Accounting System Manual: For Use by City/ Municipal AccountantsDocument104 paginiBarangay Accounting System Manual: For Use by City/ Municipal Accountantsemman neriÎncă nu există evaluări

- Barangay Budget Preparation andDocument13 paginiBarangay Budget Preparation andMimi OlshopeÎncă nu există evaluări

- National Government Sector Cluster NGS-5-Education and Employment Audit Group R16-C, Audit Team No. R16-C-04Document3 paginiNational Government Sector Cluster NGS-5-Education and Employment Audit Group R16-C, Audit Team No. R16-C-04Winnie Ann Daquil Lomosad-MisagalÎncă nu există evaluări

- 1.4 BSKE 2023 - Annexes D E and F SANGGUNIANG KABATAAN Inventory and Turnover of SK PFRDs and Money - October 30 RA No. 11935 - February 27 1Document7 pagini1.4 BSKE 2023 - Annexes D E and F SANGGUNIANG KABATAAN Inventory and Turnover of SK PFRDs and Money - October 30 RA No. 11935 - February 27 1jellyn ayosÎncă nu există evaluări

- MC No 1 s14 Guidelines On Employees On Cti StatusDocument4 paginiMC No 1 s14 Guidelines On Employees On Cti StatuslookalikenilongÎncă nu există evaluări

- Capital BudgetingDocument15 paginiCapital BudgetingJoshua Naragdag ColladoÎncă nu există evaluări

- Proposed Lpu Lagunaemployees CooperativeDocument10 paginiProposed Lpu Lagunaemployees CooperativeMarcus GreyÎncă nu există evaluări

- Semestral Report On Status of Submission of Barangay Financial Transaction DocumentsDocument2 paginiSemestral Report On Status of Submission of Barangay Financial Transaction DocumentsBARANGAY 146Încă nu există evaluări

- Accounting PrinciplesDocument35 paginiAccounting PrinciplesShruti KapoorÎncă nu există evaluări

- Aapsi 2020Document9 paginiAapsi 2020Ragnar LothbrokÎncă nu există evaluări

- Baar LabelDocument61 paginiBaar LabelJerwin Cases TiamsonÎncă nu există evaluări

- ANNEX A LDIP Alignment FormDocument5 paginiANNEX A LDIP Alignment FormMarieta AlejoÎncă nu există evaluări

- ChapterDocument17 paginiChapterQuennie DesullanÎncă nu există evaluări

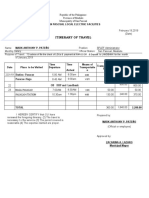

- Iterenary Travel FormDocument3 paginiIterenary Travel Formsplef lguÎncă nu există evaluări

- LGU-NGAS TableofContentsVol1Document6 paginiLGU-NGAS TableofContentsVol1Pee-Jay Inigo UlitaÎncă nu există evaluări

- Coa 2015-014Document2 paginiCoa 2015-014melizze100% (2)

- Shopping and Small Value Procurement Requirements ChecklistDocument1 paginăShopping and Small Value Procurement Requirements ChecklistMark GoducoÎncă nu există evaluări

- Piep Membership Application Form New - 1Document2 paginiPiep Membership Application Form New - 1Goldwin Ruben de CastroÎncă nu există evaluări

- Draft RCSP EO MunicipalDocument5 paginiDraft RCSP EO MunicipalFatimi SantiagoÎncă nu există evaluări

- Chapter8 Fiancial Reporting by James HallDocument43 paginiChapter8 Fiancial Reporting by James Hallkessa thea salvatoreÎncă nu există evaluări

- COA Decision Re: Splitting of ContractsDocument6 paginiCOA Decision Re: Splitting of ContractsNadine DiamanteÎncă nu există evaluări

- Coa C97-002Document4 paginiCoa C97-002Hoven MacasinagÎncă nu există evaluări

- Notes FSUU AccountingDocument18 paginiNotes FSUU AccountingRobert CastilloÎncă nu există evaluări

- Liga AOM CollectionsDocument6 paginiLiga AOM CollectionsJonson PalmaresÎncă nu există evaluări

- FS Presentation PPSASDocument12 paginiFS Presentation PPSASMarlyn Cayetano MercadoÎncă nu există evaluări

- Annex F-ICQ (Cashier) DraftDocument5 paginiAnnex F-ICQ (Cashier) DraftRussel SarachoÎncă nu există evaluări

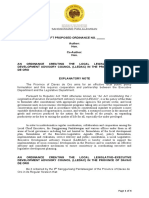

- Legislative-Executive Development Advisory Council (LEDAC) ", It Is The Policy of The StateDocument4 paginiLegislative-Executive Development Advisory Council (LEDAC) ", It Is The Policy of The StateVincient LeeÎncă nu există evaluări

- The PPSAS and The Revised Chart of AccountsDocument98 paginiThe PPSAS and The Revised Chart of AccountsDaniel Salmorin87% (15)

- Bill CertificateDocument3 paginiBill CertificateRohith ReddyÎncă nu există evaluări

- E Money PDFDocument41 paginiE Money PDFCPMMÎncă nu există evaluări

- NaftaDocument18 paginiNaftaShabla MohamedÎncă nu există evaluări

- DX210WDocument13 paginiDX210WScanner Camiones CáceresÎncă nu există evaluări

- FM.04.02.01 Project Demobilization Checklist Rev2Document2 paginiFM.04.02.01 Project Demobilization Checklist Rev2alex100% (3)

- MHO ProposalDocument4 paginiMHO ProposalLGU PadadaÎncă nu există evaluări

- Dak Tronic SDocument25 paginiDak Tronic SBreejum Portulum BrascusÎncă nu există evaluări

- Manufactures Near byDocument28 paginiManufactures Near bykomal LPS0% (1)

- The System of Government Budgeting Bangladesh: Motahar HussainDocument9 paginiThe System of Government Budgeting Bangladesh: Motahar HussainManjare Hassin RaadÎncă nu există evaluări

- Alcor's Impending Npo FailureDocument11 paginiAlcor's Impending Npo FailureadvancedatheistÎncă nu există evaluări

- 11980-Article Text-37874-1-10-20200713Document14 pagini11980-Article Text-37874-1-10-20200713hardiprasetiawanÎncă nu există evaluări

- Posting Journal - 1-5 - 1-5Document5 paginiPosting Journal - 1-5 - 1-5Shagi FastÎncă nu există evaluări

- Independent Power Producer (IPP) Debacle in Indonesia and The PhilippinesDocument19 paginiIndependent Power Producer (IPP) Debacle in Indonesia and The Philippinesmidon64Încă nu există evaluări

- StatementsDocument2 paginiStatementsFIRST FIRSÎncă nu există evaluări

- Metropolitan Transport Corporation Guindy Estate JJ Nagar WestDocument5 paginiMetropolitan Transport Corporation Guindy Estate JJ Nagar WestbiindduuÎncă nu există evaluări

- Circle Rates 2009-2010 in Gurgaon For Flats, Plots, and Agricultural Land - Gurgaon PropertyDocument15 paginiCircle Rates 2009-2010 in Gurgaon For Flats, Plots, and Agricultural Land - Gurgaon Propertyqubrex1100% (2)

- What Is InflationDocument222 paginiWhat Is InflationAhim Raj JoshiÎncă nu există evaluări

- Pembayaran PoltekkesDocument12 paginiPembayaran PoltekkesteffiÎncă nu există evaluări

- Factors Affecting SME'sDocument63 paginiFactors Affecting SME'sMubeen Shaikh50% (2)

- Working Capital Appraisal by Banks For SSI PDFDocument85 paginiWorking Capital Appraisal by Banks For SSI PDFBrijesh MaraviyaÎncă nu există evaluări

- QQy 5 N OKBej DP 2 U 8 MDocument4 paginiQQy 5 N OKBej DP 2 U 8 MAaditi yadavÎncă nu există evaluări

- BNI Mobile Banking: Histori TransaksiDocument1 paginăBNI Mobile Banking: Histori TransaksiWebi SuprayogiÎncă nu există evaluări

- India'S Tourism Industry - Progress and Emerging Issues: Dr. Rupal PatelDocument10 paginiIndia'S Tourism Industry - Progress and Emerging Issues: Dr. Rupal PatelAnonymous cRMw8feac8Încă nu există evaluări

- Where Achievement Begins: Doug ManningDocument29 paginiWhere Achievement Begins: Doug ManningbillÎncă nu există evaluări

- KaleeswariDocument14 paginiKaleeswariRocks KiranÎncă nu există evaluări

- Jay Chou Medley (周杰伦小提琴串烧) Arranged by XJ ViolinDocument2 paginiJay Chou Medley (周杰伦小提琴串烧) Arranged by XJ ViolinAsh Zaiver OdavarÎncă nu există evaluări

- CBN Rule Book Volume 5Document687 paginiCBN Rule Book Volume 5Justus OhakanuÎncă nu există evaluări

- Is Enron OverpricedDocument3 paginiIs Enron Overpricedgarimag2kÎncă nu există evaluări

- Chap014 Solution Manual Financial Institutions Management A Risk Management ApproachDocument19 paginiChap014 Solution Manual Financial Institutions Management A Risk Management ApproachFami FamzÎncă nu există evaluări

- Dhiratara Pradipta Narendra (1506790210)Document4 paginiDhiratara Pradipta Narendra (1506790210)Pradipta NarendraÎncă nu există evaluări