S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Interview Van TharpDocument7 paginiInterview Van TharpcoachbiznesuÎncă nu există evaluări

- Stock Investing Advice: An Interview With Dr. Van K. TharpDocument9 paginiStock Investing Advice: An Interview With Dr. Van K. TharpcoachbiznesuÎncă nu există evaluări

- Fifteen Rules and Five Steps For Successful Investing and Trading - The Tao of WealthDocument4 paginiFifteen Rules and Five Steps For Successful Investing and Trading - The Tao of WealthcoachbiznesuÎncă nu există evaluări

- Interview With Van Tharp - StockTickr BlogDocument11 paginiInterview With Van Tharp - StockTickr BlogcoachbiznesuÎncă nu există evaluări

- Interview Trading Psychology Expert Van Tharp PDFDocument9 paginiInterview Trading Psychology Expert Van Tharp PDFcoachbiznesuÎncă nu există evaluări

- Interview Van K. Tharp PDFDocument13 paginiInterview Van K. Tharp PDFcoachbiznesuÎncă nu există evaluări

- Interview Van Tharp Institute PDFDocument14 paginiInterview Van Tharp Institute PDFcoachbiznesuÎncă nu există evaluări

- The 9 Best Ketogenic Diet Ingredients - YouTubeDocument7 paginiThe 9 Best Ketogenic Diet Ingredients - YouTubecoachbiznesuÎncă nu există evaluări

- How To Make The Package in Python - Data Driven Investor - MediumDocument13 paginiHow To Make The Package in Python - Data Driven Investor - MediumcoachbiznesuÎncă nu există evaluări

- Balance On Power BopDocument5 paginiBalance On Power BopAnam TawhidÎncă nu există evaluări

- Zero Carb Cheat SheetDocument1 paginăZero Carb Cheat SheetcoachbiznesuÎncă nu există evaluări

- Metabolic Health 1Document7 paginiMetabolic Health 1coachbiznesuÎncă nu există evaluări

- The Power Pause - Regain Your Balance and Manifest Your IntentionsDocument10 paginiThe Power Pause - Regain Your Balance and Manifest Your IntentionscoachbiznesuÎncă nu există evaluări

- This Buddhist Technique Will Help You Fall Asleep in 2 Minutes - The AscentDocument7 paginiThis Buddhist Technique Will Help You Fall Asleep in 2 Minutes - The AscentcoachbiznesuÎncă nu există evaluări

- Turning Back The Clock On Aging Cells - The New York TimesDocument4 paginiTurning Back The Clock On Aging Cells - The New York TimescoachbiznesuÎncă nu există evaluări

- How Is Reiki Different To Access Bars? - Kerry Garner VenterDocument7 paginiHow Is Reiki Different To Access Bars? - Kerry Garner VentercoachbiznesuÎncă nu există evaluări

- The Clearing Statement - Access Clearing ToolsDocument3 paginiThe Clearing Statement - Access Clearing Toolscoachbiznesu100% (1)

- Python Packages: How To Create and Import Them?Document3 paginiPython Packages: How To Create and Import Them?coachbiznesuÎncă nu există evaluări

- Frequently Asked Questions About The Bars - Access BlogDocument20 paginiFrequently Asked Questions About The Bars - Access BlogcoachbiznesuÎncă nu există evaluări

- Bulk - How To Schedule Tweets To Save Time and Engage Your AudienceDocument16 paginiBulk - How To Schedule Tweets To Save Time and Engage Your AudiencecoachbiznesuÎncă nu există evaluări

- How To Publish Your First Python Package - It's Not That HardDocument11 paginiHow To Publish Your First Python Package - It's Not That HardcoachbiznesuÎncă nu există evaluări

- How Do I Download Data To Excel? (StockCharts Support)Document1 paginăHow Do I Download Data To Excel? (StockCharts Support)coachbiznesuÎncă nu există evaluări

- Bulk Import, Schedule and Manage Tweets With ManageFlitter's Bulk Import FeatureDocument4 paginiBulk Import, Schedule and Manage Tweets With ManageFlitter's Bulk Import FeaturecoachbiznesuÎncă nu există evaluări

- Zzeating For Gains - Part IIDocument10 paginiZzeating For Gains - Part IIcoachbiznesuÎncă nu există evaluări

- Zzhow I Hacked My Food & Lost 20kgs in 60daysDocument14 paginiZzhow I Hacked My Food & Lost 20kgs in 60dayscoachbiznesu75% (4)

- Build Python Packages Without Publishing - Towards Data ScienceDocument6 paginiBuild Python Packages Without Publishing - Towards Data SciencecoachbiznesuÎncă nu există evaluări

- Building A Python Package in Minutes - Analytics Vidhya - MediumDocument23 paginiBuilding A Python Package in Minutes - Analytics Vidhya - MediumcoachbiznesuÎncă nu există evaluări

- Denmark'S Ic Companys: Staying Sharply Focused On Strategy ExecutionDocument6 paginiDenmark'S Ic Companys: Staying Sharply Focused On Strategy ExecutioncoachbiznesuÎncă nu există evaluări

- Breakthrough Results With: The 4 Disciplines of ExecutionDocument2 paginiBreakthrough Results With: The 4 Disciplines of ExecutioncoachbiznesuÎncă nu există evaluări

- zz-7 Things I Wish Someone Had Told Me About Fitness and Weight Loss A Long Time AgoDocument12 paginizz-7 Things I Wish Someone Had Told Me About Fitness and Weight Loss A Long Time AgocoachbiznesuÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Sales Kit Backup 1Document28 paginiSales Kit Backup 1api-26863276Încă nu există evaluări

- Rusame33492Document1 paginăRusame33492jinalpatel004Încă nu există evaluări

- Econ - An Afternoon With Jim Rogers - 2009!02!04 Maybank-IB ETDocument3 paginiEcon - An Afternoon With Jim Rogers - 2009!02!04 Maybank-IB ETwonderwÎncă nu există evaluări

- Chap 005 StudentsDocument24 paginiChap 005 StudentsAlex BenyayevÎncă nu există evaluări

- Do&Dnt Interview Q & A-3Document14 paginiDo&Dnt Interview Q & A-3Praveen KNÎncă nu există evaluări

- Solutions To Concept Questions 8Document6 paginiSolutions To Concept Questions 8anaisne25Încă nu există evaluări

- Mathematics March 2007 KanDocument8 paginiMathematics March 2007 KanPrasad C MÎncă nu există evaluări

- Exchange Rate Policy and Modelling in IndiaDocument117 paginiExchange Rate Policy and Modelling in IndiaArjun SriHariÎncă nu există evaluări

- DornbuschDocument13 paginiDornbuschdivyajain2888Încă nu există evaluări

- Chapter 4Document7 paginiChapter 4Đặng Thị Ngọc UyênÎncă nu există evaluări

- DSE Enterprise Acceleration ProgramDocument1 paginăDSE Enterprise Acceleration ProgramAnonymous FnM14a0Încă nu există evaluări

- Developpments in OTC MarketsDocument80 paginiDeveloppments in OTC MarketsRexTradeÎncă nu există evaluări

- BMA5318 YWY 1213 Sem2 (A)Document3 paginiBMA5318 YWY 1213 Sem2 (A)Sumedha Shocisuto Das JpsÎncă nu există evaluări

- 2018 06 25 - Bloomberg - Businessweek USA PDFDocument80 pagini2018 06 25 - Bloomberg - Businessweek USA PDFPaco FernandezÎncă nu există evaluări

- The Simplified Futures and Options Trading StrategyDocument93 paginiThe Simplified Futures and Options Trading StrategyNaitik80% (5)

- Credit Card Setup Questionnaire: As Assigned by CC VendorDocument6 paginiCredit Card Setup Questionnaire: As Assigned by CC VendorMoon MunÎncă nu există evaluări

- Indonesia Strategy Stronger Growth and Stability PhaseDocument26 paginiIndonesia Strategy Stronger Growth and Stability PhaseNurcahya PriyonugrohoÎncă nu există evaluări

- A Study On Commodity MarketDocument68 paginiA Study On Commodity Marketbabajan_480% (5)

- Lecture 4-Hedging With FuturesDocument36 paginiLecture 4-Hedging With FuturesNIAZ ALI KHANÎncă nu există evaluări

- AlphaIndicator BONI 20181106Document11 paginiAlphaIndicator BONI 20181106Daniel WigginsÎncă nu există evaluări

- Financial IQ PDFDocument32 paginiFinancial IQ PDFgerald91% (11)

- Written Business Plan Round Scoring Criteria PDFDocument2 paginiWritten Business Plan Round Scoring Criteria PDFRestu AnnisaÎncă nu există evaluări

- Ttel.: Resa of Accountancy 735-98O7 & 734-3989Document1 paginăTtel.: Resa of Accountancy 735-98O7 & 734-3989KyohyunÎncă nu există evaluări

- Dhaka Bank ( - ) MTO - 29.09.2017Document6 paginiDhaka Bank ( - ) MTO - 29.09.2017sahadatÎncă nu există evaluări

- 5 PDFDocument36 pagini5 PDFKevin Che100% (1)

- The Cost of Capital For Swan MotorsDocument2 paginiThe Cost of Capital For Swan Motorsanhnguyen2501Încă nu există evaluări

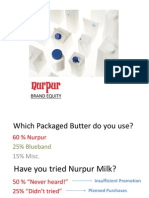

- Nurpur Brand EquityDocument19 paginiNurpur Brand EquityBilal100% (2)

- Technical Analysis For The Mathematical MindDocument1 paginăTechnical Analysis For The Mathematical MindF WilliamsÎncă nu există evaluări

- Lecture 1 PDFDocument43 paginiLecture 1 PDFOmarIsmailÎncă nu există evaluări

- 96th AIBB TMFI SolvedDocument26 pagini96th AIBB TMFI SolvedShamima AkterÎncă nu există evaluări