S-ar putea să vă placă și

- The 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsDe la EverandThe 5 Elements of the Highly Effective Debt Collector: How to Become a Top Performing Debt Collector in Less Than 30 Days!!! the Powerful Training System for Developing Efficient, Effective & Top Performing Debt CollectorsEvaluare: 5 din 5 stele5/5 (1)

- Negotiable Law Doctrines (Sundiang)Document25 paginiNegotiable Law Doctrines (Sundiang)KarellMarieLascano100% (2)

- Negotiable Instrument Hand OutsDocument51 paginiNegotiable Instrument Hand OutsHenry Jones UrsalesÎncă nu există evaluări

- Jurisprudence: I. Nature, Forms, KindsDocument13 paginiJurisprudence: I. Nature, Forms, KindsGenevieve Bermudo100% (2)

- Latin Legal Phrases, Terms and Maxims as Applied by the Malaysian CourtsDe la EverandLatin Legal Phrases, Terms and Maxims as Applied by the Malaysian CourtsÎncă nu există evaluări

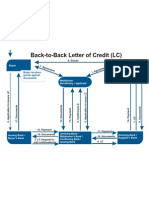

- Back To Back LCDocument1 paginăBack To Back LCJayant Nair0% (1)

- Nego Doctrines RMD BusmenteDocument5 paginiNego Doctrines RMD BusmenteMonicaSumangaÎncă nu există evaluări

- Nego - Y2S1: Midterms Answers - Doctrine of CasesDocument2 paginiNego - Y2S1: Midterms Answers - Doctrine of CasesGabrielle SantosÎncă nu există evaluări

- Nego Notes - Summary of Doctrines - 2kDocument11 paginiNego Notes - Summary of Doctrines - 2kElla MarceloÎncă nu există evaluări

- Nego Notes - Summary of Doctrines - 2kDocument11 paginiNego Notes - Summary of Doctrines - 2kFrnz Qatar-Flip TeradaÎncă nu există evaluări

- Negotiable Law DoctrinesDocument22 paginiNegotiable Law DoctrineswichupinunoÎncă nu există evaluări

- Caltex v. Court of AppealsDocument16 paginiCaltex v. Court of AppealsNoel Cagigas FelongcoÎncă nu există evaluări

- Caltex Vs CA - G.R. No. 97753. August 10, 1992Document12 paginiCaltex Vs CA - G.R. No. 97753. August 10, 1992Ebbe DyÎncă nu există evaluări

- Caltex (Phil) Inc., V. CA (212 Scra 448)Document11 paginiCaltex (Phil) Inc., V. CA (212 Scra 448)Eric Villa100% (1)

- Nego Cases AssignDocument108 paginiNego Cases AssignCzarianne GollaÎncă nu există evaluări

- Second Division: Negotiable Instruments Law Act No. 2031 Negotiable Instruments LawDocument106 paginiSecond Division: Negotiable Instruments Law Act No. 2031 Negotiable Instruments LawCzarianne GollaÎncă nu există evaluări

- CALTEX (PHILIPPINES), INC., Petitioner, vs. COURT OF Appeals and Security Bank and Trust CompanyDocument22 paginiCALTEX (PHILIPPINES), INC., Petitioner, vs. COURT OF Appeals and Security Bank and Trust CompanyChristiaan CastilloÎncă nu există evaluări

- Caltex Philippines Inc. v. CADocument14 paginiCaltex Philippines Inc. v. CARein NantesÎncă nu există evaluări

- 7 Caltex Philippines Inc. v. Court of AppealsDocument15 pagini7 Caltex Philippines Inc. v. Court of AppealsJulius R. TeeÎncă nu există evaluări

- Negotiable Instruments Law SodDocument20 paginiNegotiable Instruments Law SodEmmanuel Emigdio DumlaoÎncă nu există evaluări

- Negotiable Instruments - AnnotatedDocument54 paginiNegotiable Instruments - AnnotatedArchie GuevarraÎncă nu există evaluări

- Nego DigestsDocument26 paginiNego DigestsTeacherEliÎncă nu există evaluări

- GDFDFGDFDocument8 paginiGDFDFGDFgem baeÎncă nu există evaluări

- Warriors' Notes: Mercantile LAWDocument33 paginiWarriors' Notes: Mercantile LAWJing Goal Merit67% (3)

- Held:: Trader's Royal v. CADocument7 paginiHeld:: Trader's Royal v. CAAngela ParadoÎncă nu există evaluări

- Case 2Document40 paginiCase 2Howard DinumlaÎncă nu există evaluări

- Nego Cases ReviewerDocument7 paginiNego Cases ReviewerWinnie Anne Cuerdo100% (1)

- I. Corporation CodeDocument23 paginiI. Corporation CodeCharlie MagneÎncă nu există evaluări

- Red Notes: Mercantile LawDocument36 paginiRed Notes: Mercantile Lawjojitus100% (2)

- Layese - Negotiable InstrumentsDocument13 paginiLayese - Negotiable InstrumentsAndrei Jose V. LayeseÎncă nu există evaluări

- Negotiable Instruments Law CasesDocument2 paginiNegotiable Instruments Law CasesMia Abegail ChuaÎncă nu există evaluări

- Act 2031, 03 February 1911 Sec. 60, New Central Bank Act, R.A. 7653 Art. 1249, CCDocument57 paginiAct 2031, 03 February 1911 Sec. 60, New Central Bank Act, R.A. 7653 Art. 1249, CCrdÎncă nu există evaluări

- Caltex VsDocument2 paginiCaltex Vsmore2xÎncă nu există evaluări

- Nego - Midterms - Case DoctrinesDocument25 paginiNego - Midterms - Case DoctrinesSage LingatongÎncă nu există evaluări

- Midterms Case Doctrines NegoDocument6 paginiMidterms Case Doctrines NegoAlex Viray LucinarioÎncă nu există evaluări

- Nego LawDocument17 paginiNego LawErika RedÎncă nu există evaluări

- Pointers in Negotiable Instruments LawDocument7 paginiPointers in Negotiable Instruments LawMaria Diory RabajanteÎncă nu există evaluări

- Agency, Trust, and Partnership DoctrinesDocument46 paginiAgency, Trust, and Partnership DoctrinesAlvin100% (1)

- Negotiable Instruments Law DoctrinesDocument21 paginiNegotiable Instruments Law DoctrinesMarc Daniel MolinaÎncă nu există evaluări

- Handout No. 3Document4 paginiHandout No. 3Cielo Mae ParungoÎncă nu există evaluări

- Negotiable Instruments Law: ACT NO. 2031Document43 paginiNegotiable Instruments Law: ACT NO. 2031Majorie ArimadoÎncă nu există evaluări

- Concept of Negotiable InstrumentsDocument6 paginiConcept of Negotiable InstrumentsJemmieÎncă nu există evaluări

- Unit Iv PDFDocument12 paginiUnit Iv PDFlena cpaÎncă nu există evaluări

- Negotiable Instruments Law ReviewerDocument8 paginiNegotiable Instruments Law ReviewerKath100% (1)

- Outline Agency - Filled OutDocument9 paginiOutline Agency - Filled OutZahraMinaÎncă nu există evaluări

- Caltex Phil. vs. CADocument3 paginiCaltex Phil. vs. CAKym AlgarmeÎncă nu există evaluări

- Negotiable Instruments LawDocument57 paginiNegotiable Instruments LawKimberly BanuelosÎncă nu există evaluări

- Caltex VS CaDocument18 paginiCaltex VS CaViolet BlueÎncă nu există evaluări

- Philippine Education Co. vs. Soriano: Case DoctrinesDocument5 paginiPhilippine Education Co. vs. Soriano: Case DoctrinesTRXÎncă nu există evaluări

- Pointers & Cases: Negotiable Instruments LawDocument7 paginiPointers & Cases: Negotiable Instruments LawPduys16Încă nu există evaluări

- ("To Bearer") Because Only A DraweeDocument9 pagini("To Bearer") Because Only A DraweeDeanna Noreen HolgadoÎncă nu există evaluări

- NIL Compilation of ReviewersDocument236 paginiNIL Compilation of ReviewerstowanÎncă nu există evaluări

- CIV Case DigestDocument86 paginiCIV Case DigestvalkyriorÎncă nu există evaluări

- Violago vs. Ba FinanceDocument29 paginiViolago vs. Ba FinanceChristine MontefalconÎncă nu există evaluări

- A Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsDe la EverandA Simple Guide for Drafting of Conveyances in India : Forms of Conveyances and Instruments executed in the Indian sub-continent along with Notes and TipsÎncă nu există evaluări

- Bigger Problems: Major Concepts for Understanding Transactions under Islamic lawDe la EverandBigger Problems: Major Concepts for Understanding Transactions under Islamic lawÎncă nu există evaluări

- Introduction to Negotiable Instruments: As per Indian LawsDe la EverandIntroduction to Negotiable Instruments: As per Indian LawsEvaluare: 5 din 5 stele5/5 (1)

- Life, Accident and Health Insurance in the United StatesDe la EverandLife, Accident and Health Insurance in the United StatesEvaluare: 5 din 5 stele5/5 (1)

- Suspension Order Effects:: Provided, That Any Final and Executory Judgment Arising From Such Appeal Shall BeDocument3 paginiSuspension Order Effects:: Provided, That Any Final and Executory Judgment Arising From Such Appeal Shall BeEnteng KabisoteÎncă nu există evaluări

- Moms RemarksDocument1 paginăMoms RemarksEnteng KabisoteÎncă nu există evaluări

- CrimPro CasesDocument12 paginiCrimPro CasesEnteng KabisoteÎncă nu există evaluări

- Chapter 1 - General PrinciplesDocument64 paginiChapter 1 - General PrinciplesEnteng KabisoteÎncă nu există evaluări

- Tax Notes (Dizon Book)Document3 paginiTax Notes (Dizon Book)Enteng KabisoteÎncă nu există evaluări

- Persons Cases2Document12 paginiPersons Cases2Enteng KabisoteÎncă nu există evaluări

- Legarda VS CaDocument8 paginiLegarda VS CaPatatas SayoteÎncă nu există evaluări

- Briones vs. CammayoDocument1 paginăBriones vs. CammayoChicoRodrigoBantayog100% (1)

- Similarities and Differences Between Special WritsDocument3 paginiSimilarities and Differences Between Special WritsJuliet Czarina Furia EinsteinÎncă nu există evaluări

- Torts (Scope of Quasi Delict)Document7 paginiTorts (Scope of Quasi Delict)JunRobotboiÎncă nu există evaluări

- Right To Travel - Statutes, Codes & Regulations Are Not LawDocument11 paginiRight To Travel - Statutes, Codes & Regulations Are Not Lawfree100% (2)

- Petitioner Vs Vs Respondent William F. Peralta, Solicitor General Tañada, City Fiscal MabanagDocument48 paginiPetitioner Vs Vs Respondent William F. Peralta, Solicitor General Tañada, City Fiscal MabanagKirby MalibiranÎncă nu există evaluări

- In Re: Cunanan, Et Al.: DioknoDocument1 paginăIn Re: Cunanan, Et Al.: Dioknojaana albanoÎncă nu există evaluări

- 498 (A) Direction by Supreme CourtDocument21 pagini498 (A) Direction by Supreme CourtDeepanshi RajputÎncă nu există evaluări

- Intellectual Property LawDocument3 paginiIntellectual Property LawRmLyn MclnaoÎncă nu există evaluări

- What Are The Different Examinations Administered by The National Police Commission?Document6 paginiWhat Are The Different Examinations Administered by The National Police Commission?Paolo VariasÎncă nu există evaluări

- United States v. James L. Griggs, United States of America v. Curtis G. Bridges, 713 F.2d 672, 11th Cir. (1983)Document4 paginiUnited States v. James L. Griggs, United States of America v. Curtis G. Bridges, 713 F.2d 672, 11th Cir. (1983)Scribd Government DocsÎncă nu există evaluări

- Agcaoili Versus MolinaDocument9 paginiAgcaoili Versus MolinaAnskee TejamÎncă nu există evaluări

- Transfer of Property: BasicsDocument14 paginiTransfer of Property: BasicsTania MajumderÎncă nu există evaluări

- Tagolino V HRET Case DigestDocument4 paginiTagolino V HRET Case DigestJose Ignatius D. PerezÎncă nu există evaluări

- Ruling Kintu Samuel Another V Registrar of Companies OthersDocument10 paginiRuling Kintu Samuel Another V Registrar of Companies Othersbogere robertÎncă nu există evaluări

- Legal Language and Writing: How To Draft A PleadingDocument8 paginiLegal Language and Writing: How To Draft A PleadingPratham SaxenaÎncă nu există evaluări

- Technology Properties v. MicrodiaDocument8 paginiTechnology Properties v. MicrodiaPriorSmartÎncă nu există evaluări

- Lewisville PD050509Document5 paginiLewisville PD050509The Dallas Morning NewsÎncă nu există evaluări

- Delhi University, Llb. Entrance TEST, 2019Document14 paginiDelhi University, Llb. Entrance TEST, 2019Ram Mohan VattikondaÎncă nu există evaluări

- ConfirmationDocument5 paginiConfirmationMuni ReddyÎncă nu există evaluări

- Maxwell Letter MotionDocument6 paginiMaxwell Letter MotionLaw&CrimeÎncă nu există evaluări

- Ateneo de Manila University School of Law: 1 Semester, AY 2022-2023Document19 paginiAteneo de Manila University School of Law: 1 Semester, AY 2022-2023janÎncă nu există evaluări

- Elvira Q. Tamondong: Teacher 3Document34 paginiElvira Q. Tamondong: Teacher 3Margie RodriguezÎncă nu există evaluări

- Casco Philippine Chemical Co vs. GimenezDocument2 paginiCasco Philippine Chemical Co vs. GimenezAnton MercadoÎncă nu există evaluări

- Ramirez V GmurDocument3 paginiRamirez V GmurSamantha BugayÎncă nu există evaluări

- People vs. RubioDocument6 paginiPeople vs. RubioRh MalonÎncă nu există evaluări

- In Defense of The Juvenile Justice and Welfare Act of 2006Document35 paginiIn Defense of The Juvenile Justice and Welfare Act of 2006TimÎncă nu există evaluări

- FINAL JUDGMENT 2020 No 243 Civ Wolda Salamma Gardner V The Department of Public Prosecutions Et Al With CitationDocument15 paginiFINAL JUDGMENT 2020 No 243 Civ Wolda Salamma Gardner V The Department of Public Prosecutions Et Al With CitationAnonymous UpWci5Încă nu există evaluări

- Filipinas Investment 9Document3 paginiFilipinas Investment 9Bibi JumpolÎncă nu există evaluări