S-ar putea să vă placă și

- Excise Taxes NotesDocument26 paginiExcise Taxes NotesKaren Cael100% (1)

- What Is Percentage TaxDocument4 paginiWhat Is Percentage Taxmy miÎncă nu există evaluări

- Double TaxationDocument4 paginiDouble TaxationLou Nonoi TanÎncă nu există evaluări

- Excise TaxDocument15 paginiExcise TaxQedew ErÎncă nu există evaluări

- Ord No.65 s.2007 Anti SmokingDocument12 paginiOrd No.65 s.2007 Anti SmokingJovelan V. EscañoÎncă nu există evaluări

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 paginiTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesÎncă nu există evaluări

- The Concept of Taxation and Estate TaxDocument6 paginiThe Concept of Taxation and Estate TaxKara MiaÎncă nu există evaluări

- Taxation (Income Tax) - Pp41-60Document37 paginiTaxation (Income Tax) - Pp41-60Iya PadernaÎncă nu există evaluări

- CEDAWDocument5 paginiCEDAWShyGal_MsaÎncă nu există evaluări

- Tax2 DigestsDocument11 paginiTax2 DigestsErwin Roxas100% (1)

- Opt and Excise TaxDocument20 paginiOpt and Excise TaxDana Marie FamorÎncă nu există evaluări

- Villanueva Vs City of IloiloDocument7 paginiVillanueva Vs City of IloilocharmssatellÎncă nu există evaluări

- Tax 2 Reviewer: A. Transfer TaxesDocument11 paginiTax 2 Reviewer: A. Transfer TaxesIsay YasonÎncă nu există evaluări

- VAT TableDocument1 paginăVAT TableAnonymous PlK2KakJpÎncă nu există evaluări

- Business Tax Reviewer IDocument5 paginiBusiness Tax Reviewer IMariefel Irish Jimenez KhuÎncă nu există evaluări

- Secretary Vs Lazatin: FactsDocument6 paginiSecretary Vs Lazatin: FactsArah Mae BonillaÎncă nu există evaluări

- UP Succession 2Document109 paginiUP Succession 2Drean TubislloÎncă nu există evaluări

- Evangelista Vs CollectorDocument3 paginiEvangelista Vs CollectorOne TwoÎncă nu există evaluări

- Consolidated Dairy Products CoDocument2 paginiConsolidated Dairy Products CoRaymond AlhambraÎncă nu există evaluări

- Subject To Vat (Nccidactee) : (Contribution Per Member P15,000 - VAT, Electric Cooperatives - VAT)Document13 paginiSubject To Vat (Nccidactee) : (Contribution Per Member P15,000 - VAT, Electric Cooperatives - VAT)Michael AquinoÎncă nu există evaluări

- Donors and VatDocument179 paginiDonors and VatGlino ClaudioÎncă nu există evaluări

- Agra - SSS Law - 102017Document34 paginiAgra - SSS Law - 102017Andrea DeloviarÎncă nu există evaluări

- Restrictions On Capacity To ActDocument1 paginăRestrictions On Capacity To Actdmad_shayneÎncă nu există evaluări

- Chapter 3.1 - VAT Exempt Sales PDFDocument10 paginiChapter 3.1 - VAT Exempt Sales PDFJade Berlyn AgcaoiliÎncă nu există evaluări

- Atlas Mining Vs CirDocument2 paginiAtlas Mining Vs CirmenforeverÎncă nu există evaluări

- 4 - CIR v. Pineda, 21 SCRA 105Document4 pagini4 - CIR v. Pineda, 21 SCRA 105Lemuel Montes Jr.Încă nu există evaluări

- TORTS - 1 IntroductionDocument5 paginiTORTS - 1 IntroductionAnnabelle C. VecinalÎncă nu există evaluări

- Sison vs. Ancheta, 130 SCRA 654 (1984)Document4 paginiSison vs. Ancheta, 130 SCRA 654 (1984)Christiaan CastilloÎncă nu există evaluări

- TAX 1016 Lesson ONE PDFDocument7 paginiTAX 1016 Lesson ONE PDFMonica MonicaÎncă nu există evaluări

- TX10 Other Percentage TaxDocument16 paginiTX10 Other Percentage TaxAnna AldaveÎncă nu există evaluări

- Income Tax On Estates and Trusts: A. Taxability of EstatesDocument4 paginiIncome Tax On Estates and Trusts: A. Taxability of EstatesKevin OnaroÎncă nu există evaluări

- No 14 - The Late Lino Gutierrez V Collector of Internal RevenueDocument2 paginiNo 14 - The Late Lino Gutierrez V Collector of Internal RevenueA Paula Cruz FranciscoÎncă nu există evaluări

- CIR v. Fisher ADocument30 paginiCIR v. Fisher ACE SherÎncă nu există evaluări

- Petron vs. Pililla, G.R. No. 90776, June 3, 1991Document8 paginiPetron vs. Pililla, G.R. No. 90776, June 3, 1991Machida AbrahamÎncă nu există evaluări

- Other Percentage TaxesDocument34 paginiOther Percentage TaxesRose Diane CabiscuelasÎncă nu există evaluări

- CIR Vs Toshiba Information EquipmentDocument1 paginăCIR Vs Toshiba Information EquipmentKayee KatÎncă nu există evaluări

- Attorney - S Fees - 2020Document40 paginiAttorney - S Fees - 2020Ivan ConradÎncă nu există evaluări

- Alfredo Baroy vs. The PhilippinesDocument2 paginiAlfredo Baroy vs. The PhilippinesSheena Yunzal Garidan-GrazaÎncă nu există evaluări

- Tax Syllabus (Spit) 2015Document16 paginiTax Syllabus (Spit) 2015Clarissa de VeraÎncă nu există evaluări

- Basic Concept and Nature of Transfer TaxesDocument21 paginiBasic Concept and Nature of Transfer TaxesKarl BasaÎncă nu există evaluări

- Digested CasesDocument36 paginiDigested CasesJepoy Nisperos ReyesÎncă nu există evaluări

- Eg. Class Notes, Research Papers, Presentations: My Heart Went OpsDocument2 paginiEg. Class Notes, Research Papers, Presentations: My Heart Went OpsEnzoGarciaÎncă nu există evaluări

- Tax Cases - Batch 1Document42 paginiTax Cases - Batch 1Shaira Mae CuevillasÎncă nu există evaluări

- Taxation Reviewer: Taxation in Act and Inherent Provide Money To Pay)Document5 paginiTaxation Reviewer: Taxation in Act and Inherent Provide Money To Pay)Maria Elena AquinoÎncă nu există evaluări

- Taxation Law Bar Questions 06-14Document49 paginiTaxation Law Bar Questions 06-14CarmeloÎncă nu există evaluări

- TAXATION 1 TSN - 3rd Exam PDFDocument33 paginiTAXATION 1 TSN - 3rd Exam PDFPearl Angeli Quisido CanadaÎncă nu există evaluări

- Criminal Justice System by Manuel G. CoDocument17 paginiCriminal Justice System by Manuel G. CoSecret Student0% (1)

- Obillos vs. CIRDocument1 paginăObillos vs. CIRElleÎncă nu există evaluări

- VDA. DE ESCONDE v. CADocument2 paginiVDA. DE ESCONDE v. CAKingÎncă nu există evaluări

- Pepsi Vs ButuanDocument3 paginiPepsi Vs Butuanlovekimsohyun89Încă nu există evaluări

- 4 - G.R. No. 117982 - CIR V CADocument4 pagini4 - G.R. No. 117982 - CIR V CARenz Francis LimÎncă nu există evaluări

- Conflicts of LawDocument2 paginiConflicts of LawNadalap NnayramÎncă nu există evaluări

- G.R. No. L-21570 - Limpan Investment Corp. v. Commissioner of Internal RevenueDocument3 paginiG.R. No. L-21570 - Limpan Investment Corp. v. Commissioner of Internal RevenueMegan AglauaÎncă nu există evaluări

- 008 Francia v. IACDocument2 pagini008 Francia v. IACLoren Bea TulalianÎncă nu există evaluări

- Lecture 4: International Litigation: Adopting Luke Nottage and Vivienne Bath in Some PartsDocument29 paginiLecture 4: International Litigation: Adopting Luke Nottage and Vivienne Bath in Some PartsClarissa NombresÎncă nu există evaluări

- 18 Misamis Lumber Corp. vs. Capital Ins. & Surety Co., Inc. 17 SCRA 228, May 20, 1966Document5 pagini18 Misamis Lumber Corp. vs. Capital Ins. & Surety Co., Inc. 17 SCRA 228, May 20, 1966joyeduardoÎncă nu există evaluări

- Tax 1 ReviewerDocument16 paginiTax 1 ReviewerverkieÎncă nu există evaluări

- Taxation Law - NIRC Vs TRAINDocument3 paginiTaxation Law - NIRC Vs TRAINGemma F. Tiama100% (2)

- TRAIN LAW Comparative AnalysisDocument2 paginiTRAIN LAW Comparative AnalysisElaine100% (3)

- Landlord Tax Planning StrategiesDe la EverandLandlord Tax Planning StrategiesÎncă nu există evaluări

- SOGIEDocument40 paginiSOGIEDon Villanueva Liongson88% (8)

- 1 - BalingitDocument6 pagini1 - BalingitHannah Beatriz CabralÎncă nu există evaluări

- Agenda: 128 Regular Session 13 June 2022, 9:00AMDocument2 paginiAgenda: 128 Regular Session 13 June 2022, 9:00AMHannah Beatriz CabralÎncă nu există evaluări

- Be It Ordained by The Municipality of Lemery, Batangas ThatDocument3 paginiBe It Ordained by The Municipality of Lemery, Batangas ThatHannah Beatriz CabralÎncă nu există evaluări

- L/epublit of Tfit"jbilippines Manila: CourtDocument7 paginiL/epublit of Tfit"jbilippines Manila: CourtAnonymous KgPX1oCfrÎncă nu există evaluări

- Ph020en PDFDocument30 paginiPh020en PDFHannah Beatriz CabralÎncă nu există evaluări

- 2015 Bar Q - MERCANTILE LAWDocument16 pagini2015 Bar Q - MERCANTILE LAWLimVianesseÎncă nu există evaluări

- Sponsorship/Solicitation MonitoringDocument9 paginiSponsorship/Solicitation MonitoringHannah Beatriz CabralÎncă nu există evaluări

- Living and Non Living Things 1Document27 paginiLiving and Non Living Things 1Hannah Beatriz CabralÎncă nu există evaluări

- Development Bank of The Phils., V. Commission On Audit, 373 SCRA 356 (2002)Document33 paginiDevelopment Bank of The Phils., V. Commission On Audit, 373 SCRA 356 (2002)Hannah Beatriz CabralÎncă nu există evaluări

- Remedies Nirc / National Local Real Property LevyDocument6 paginiRemedies Nirc / National Local Real Property LevyHannah Beatriz CabralÎncă nu există evaluări

- Legal Writing Lesson 9 Law Office MemoDocument18 paginiLegal Writing Lesson 9 Law Office MemoHannah Beatriz CabralÎncă nu există evaluări

- Remedies of TaxpayerDocument2 paginiRemedies of TaxpayerHannah Beatriz CabralÎncă nu există evaluări

- Homeroom ModuleDocument4 paginiHomeroom ModuleHannah Beatriz CabralÎncă nu există evaluări

- FULL STP Script Pub1.4 FINAL REV AUG 2016Document28 paginiFULL STP Script Pub1.4 FINAL REV AUG 2016Hannah Beatriz CabralÎncă nu există evaluări

- Govt vs. El HogarDocument73 paginiGovt vs. El HogarHannah Beatriz CabralÎncă nu există evaluări

- Final STP DeckDocument30 paginiFinal STP DeckHannah Beatriz CabralÎncă nu există evaluări

- BLSPM3354H Partb 2021-22Document3 paginiBLSPM3354H Partb 2021-22kumar reddyÎncă nu există evaluări

- Garcia Arby Jay D. Ba 223-Income Taxation Midterm ExaminationDocument4 paginiGarcia Arby Jay D. Ba 223-Income Taxation Midterm ExaminationfssdsddsfdsfsdÎncă nu există evaluări

- Mobitex Network: Billed To: Shipped ToDocument1 paginăMobitex Network: Billed To: Shipped ToVijay SharmaÎncă nu există evaluări

- FTF 2023-01-06 1673061063263 105443Document3 paginiFTF 2023-01-06 1673061063263 105443brandon boggini100% (2)

- Cfas - Pas 12Document2 paginiCfas - Pas 12Gio BurburanÎncă nu există evaluări

- CACTUS MAY 2023 CIC02774 PayslipDocument1 paginăCACTUS MAY 2023 CIC02774 Payslipuraza.octavoÎncă nu există evaluări

- Form 15GDocument2 paginiForm 15GSrinivasa RaghavanÎncă nu există evaluări

- Invoice 686962787Document1 paginăInvoice 686962787Zayn MemanÎncă nu există evaluări

- Aaykar Bhawan, Ist Floor, Kawdiar Po, Thiruvananthapuram, Kerala, 695003 Email: TVM - DCIT.IT@INCOMETAX - GOV.IN, Office Phone:04712566715Document1 paginăAaykar Bhawan, Ist Floor, Kawdiar Po, Thiruvananthapuram, Kerala, 695003 Email: TVM - DCIT.IT@INCOMETAX - GOV.IN, Office Phone:04712566715vijuÎncă nu există evaluări

- Date Details (R) AMOUNT (Excl. Vat) (R) Vat (R) AMOUNT (Incl. Vat)Document2 paginiDate Details (R) AMOUNT (Excl. Vat) (R) Vat (R) AMOUNT (Incl. Vat)NinaÎncă nu există evaluări

- Disclaimer - : This Spreadsheet Is FreeDocument218 paginiDisclaimer - : This Spreadsheet Is FreePaul BischoffÎncă nu există evaluări

- WC157 158Document5 paginiWC157 158JayBalaÎncă nu există evaluări

- 27 Dheeraj Kumar Mandoriya PDFDocument1 pagină27 Dheeraj Kumar Mandoriya PDFyusuf pathanÎncă nu există evaluări

- Corporate Income TaxationDocument3 paginiCorporate Income TaxationKezÎncă nu există evaluări

- FI515 Homework Week 1Document3 paginiFI515 Homework Week 1leizalmÎncă nu există evaluări

- GSTR3B 29aaifa3562d1zl 022020Document3 paginiGSTR3B 29aaifa3562d1zl 022020HEMANTH kumarÎncă nu există evaluări

- Transfer by Trustees To Beneficiary: Form No. 4Document1 paginăTransfer by Trustees To Beneficiary: Form No. 4Sudeep SharmaÎncă nu există evaluări

- Income Tax Fundamentals 2015 33rd Edition Whittenburg Solutions ManualDocument26 paginiIncome Tax Fundamentals 2015 33rd Edition Whittenburg Solutions Manualdianbandelethek6xo100% (23)

- 4 5B Taxation of Individuals Graduated RatesDocument9 pagini4 5B Taxation of Individuals Graduated RatesArgie DeguzmanÎncă nu există evaluări

- EmployeeDocument2 paginiEmployeeMikko MolonÎncă nu există evaluări

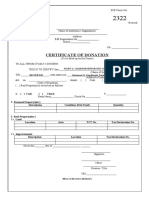

- BIR Form 2322 Cert of Don - FG Calderon High SchoolDocument3 paginiBIR Form 2322 Cert of Don - FG Calderon High SchoolEdmund G. VillarealÎncă nu există evaluări

- Electronic Filing Instructions For Your 2019 Federal Tax ReturnDocument6 paginiElectronic Filing Instructions For Your 2019 Federal Tax ReturnSindy Cruz100% (1)

- Tally SOP-3 Solution (Final Without Errors)Document3 paginiTally SOP-3 Solution (Final Without Errors)Diya -plays hereÎncă nu există evaluări

- Income Taxation 2021 Rex Banggawan Answers Multiple Choice-Theory: General ConceptsDocument6 paginiIncome Taxation 2021 Rex Banggawan Answers Multiple Choice-Theory: General ConceptsJustine UngabÎncă nu există evaluări

- CCA Tax Shield FormulaDocument1 paginăCCA Tax Shield Formulaeconlady100% (1)

- Cost of Debt: MeaningsDocument21 paginiCost of Debt: MeaningsDevyansh GuptaÎncă nu există evaluări

- RV ICE S: Krishna Sales & ServicesDocument1 paginăRV ICE S: Krishna Sales & ServicesSaikatÎncă nu există evaluări

- Paseo Realty & Dev. Corp. vs. CA, CTA, and CIR Case DigestDocument2 paginiPaseo Realty & Dev. Corp. vs. CA, CTA, and CIR Case DigestReniel Eda100% (2)

- Solved Broward Corp Owns 1 500 Shares of Silver Fox Corporation Common PDFDocument1 paginăSolved Broward Corp Owns 1 500 Shares of Silver Fox Corporation Common PDFAnbu jaromiaÎncă nu există evaluări