S-ar putea să vă placă și

- Ed A 02.00 I 01Document39 paginiEd A 02.00 I 01Enrique BlancoÎncă nu există evaluări

- No Painless Solution To Greece's Debt Crisis: Vanessa Rossi and Rodrigo Delgado AguileraDocument23 paginiNo Painless Solution To Greece's Debt Crisis: Vanessa Rossi and Rodrigo Delgado AguileragunduuuuÎncă nu există evaluări

- Boiler-Water ChemistryDocument94 paginiBoiler-Water ChemistryPRAG100% (2)

- Solution Manual For International Macroeconomics 4th Edition Robert C FeenstraDocument5 paginiSolution Manual For International Macroeconomics 4th Edition Robert C FeenstraVicky Lopez100% (30)

- Asset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceDe la EverandAsset Rotation: The Demise of Modern Portfolio Theory and the Birth of an Investment RenaissanceÎncă nu există evaluări

- Baccolini, Raffaela - CH 8 Finding Utopia in Dystopia Feminism, Memory, Nostalgia and HopeDocument16 paginiBaccolini, Raffaela - CH 8 Finding Utopia in Dystopia Feminism, Memory, Nostalgia and HopeMelissa de SáÎncă nu există evaluări

- Understanding The School Curriculum Close Encounter With The School Curriculum SPARK Your InterestDocument12 paginiUnderstanding The School Curriculum Close Encounter With The School Curriculum SPARK Your InterestJoshua Lander Soquita CadayonaÎncă nu există evaluări

- Chapter 2 Governance and ManagementDocument32 paginiChapter 2 Governance and Managementlmmh100% (2)

- Basel Accords and Framework CombineDocument30 paginiBasel Accords and Framework Combinelmmh100% (1)

- Calcium Carbonate Lab ReportDocument2 paginiCalcium Carbonate Lab ReportAlexander Weber0% (1)

- Organic Agriculture Gr12 - Module2.final For StudentDocument20 paginiOrganic Agriculture Gr12 - Module2.final For Studentapril jean cahoyÎncă nu există evaluări

- All The Money in The World September 20, 2018 PDFDocument48 paginiAll The Money in The World September 20, 2018 PDFSittidath PrasertrungruangÎncă nu există evaluări

- "Billionares": and They Were Not Happy About ItDocument36 pagini"Billionares": and They Were Not Happy About Itkhanriyaz23941560Încă nu există evaluări

- Understanding Market Channels and Alternatives For Commercial Catfish Farmers (PDFDrive)Document95 paginiUnderstanding Market Channels and Alternatives For Commercial Catfish Farmers (PDFDrive)AmiibahÎncă nu există evaluări

- BC WatershedDocument15 paginiBC Watershedshihan ZhangÎncă nu există evaluări

- Peerea MoldovaDocument30 paginiPeerea MoldovaKristina SchmidtÎncă nu există evaluări

- The Economy and Its Effect On Higher Education: William F. Jarvis, Managing Director, Commonfund InstituteDocument43 paginiThe Economy and Its Effect On Higher Education: William F. Jarvis, Managing Director, Commonfund InstitutepulavarthiÎncă nu există evaluări

- Macroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulDocument21 paginiMacroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulMaria KulawikÎncă nu există evaluări

- Morning News Notes: 2010-05-17Document2 paginiMorning News Notes: 2010-05-17glerner133926Încă nu există evaluări

- EES Presentation Koch PDFDocument67 paginiEES Presentation Koch PDFVaibhav GhildiyalÎncă nu există evaluări

- NJ HPI RatioDocument1 paginăNJ HPI Ratiokettle1Încă nu există evaluări

- Oklahoma Budget Trends and Outlook (Rev. Jan 13, 2010)Document39 paginiOklahoma Budget Trends and Outlook (Rev. Jan 13, 2010)dblattokÎncă nu există evaluări

- Overseas Recr Practises Wcms - 100010Document20 paginiOverseas Recr Practises Wcms - 100010Joseph AugustineÎncă nu există evaluări

- The Future of Securitization: 5 Annual Credit Risk ConferenceDocument13 paginiThe Future of Securitization: 5 Annual Credit Risk Conferenceanon-121346Încă nu există evaluări

- Oklahoma Budget Overview: Trends and Outlook (May 12, 2010)Document44 paginiOklahoma Budget Overview: Trends and Outlook (May 12, 2010)dblattokÎncă nu există evaluări

- Macroeconomics I: Open EconomyDocument26 paginiMacroeconomics I: Open EconomyAlèxia SalvadorÎncă nu există evaluări

- Asia StrategyDocument21 paginiAsia StrategySouvia RahimahÎncă nu există evaluări

- NJ - Ca - FL Income PriceDocument1 paginăNJ - Ca - FL Income Pricekettle1Încă nu există evaluări

- Energy: Figure 3.1: Power ShortageDocument18 paginiEnergy: Figure 3.1: Power ShortageSyed Muhammad Ahsan RizviÎncă nu există evaluări

- 2014 Photochemical Assessment Monitoring Station (PAMS) SummaryDocument6 pagini2014 Photochemical Assessment Monitoring Station (PAMS) Summaryھنس مکيÎncă nu există evaluări

- Impact of Foreign Exchange Reserves On Nigerian Stock MarketDocument8 paginiImpact of Foreign Exchange Reserves On Nigerian Stock MarketAaronÎncă nu există evaluări

- RX Drug Spending Tables Accompanying Policy BriefDocument1 paginăRX Drug Spending Tables Accompanying Policy BriefSandy CohenÎncă nu există evaluări

- Murder Rate of Death Penalty States Compared To Non Death Penalty States Death Penalty Information CenterDocument3 paginiMurder Rate of Death Penalty States Compared To Non Death Penalty States Death Penalty Information CenterRalph Moses PadillaÎncă nu există evaluări

- Monev Kab. Tapin THN 2018Document24 paginiMonev Kab. Tapin THN 2018Nawra naziraÎncă nu există evaluări

- The Cuban Economy:: Current Performance and Future Trends: Focus On External TradeDocument9 paginiThe Cuban Economy:: Current Performance and Future Trends: Focus On External Tradevikramgodara94898Încă nu există evaluări

- Operations & Supply Chain Management (Unit 3)Document31 paginiOperations & Supply Chain Management (Unit 3)Kiril IlievÎncă nu există evaluări

- Globalización Económica y Cadenas Globales de Valor Estadistica de Dinamarca-2013Document27 paginiGlobalización Económica y Cadenas Globales de Valor Estadistica de Dinamarca-2013raul jonathan palomino ocampoÎncă nu există evaluări

- Net Monthly TIC Flows: Kettle1 Research Kettle1 ResearchDocument7 paginiNet Monthly TIC Flows: Kettle1 Research Kettle1 Researchkettle1Încă nu există evaluări

- Can We Get Rid of Palm OilDocument3 paginiCan We Get Rid of Palm OiljaboerboyÎncă nu există evaluări

- The Economic Foundations of Imperialism: Guglielmo Carchedi and Michael Roberts HM London November 2019Document28 paginiThe Economic Foundations of Imperialism: Guglielmo Carchedi and Michael Roberts HM London November 2019MrWaratahsÎncă nu există evaluări

- Fama DB Prize Market Efficiency October 2005Document15 paginiFama DB Prize Market Efficiency October 2005Nathan AwÎncă nu există evaluări

- An Empirical Study in Albania of Foreign Direct Investments and Economic Growth RelationshipDocument10 paginiAn Empirical Study in Albania of Foreign Direct Investments and Economic Growth RelationshipVidya YuniantiÎncă nu există evaluări

- Inflation Unemployment Line GraphDocument2 paginiInflation Unemployment Line GraphLady Arianne CandelarioÎncă nu există evaluări

- 2017 Annual Housing Market Survey WebinarDocument62 pagini2017 Annual Housing Market Survey WebinarC.A.R. Research & EconomicsÎncă nu există evaluări

- The Tail Chaser The Land of The Setting SunDocument77 paginiThe Tail Chaser The Land of The Setting SunDanell BronkhorstÎncă nu există evaluări

- Hugh Donovan, Eight-Year Review of The Full Depth Reclamation Process in The City of EdmontonDocument40 paginiHugh Donovan, Eight-Year Review of The Full Depth Reclamation Process in The City of Edmontoneye2iÎncă nu există evaluări

- Chairmans CornerDocument3 paginiChairmans Cornerjstamp02Încă nu există evaluări

- Dividend DecisionsDocument36 paginiDividend DecisionsMohammed ZakriyaÎncă nu există evaluări

- 5 consumodeenergiaUSA PDFDocument41 pagini5 consumodeenergiaUSA PDFAlex Huaraca YuyaliÎncă nu există evaluări

- Ch01 - IntroductionDocument41 paginiCh01 - IntroductionNhuÎncă nu există evaluări

- GRAPHDocument1 paginăGRAPHShanelle MacajilosÎncă nu există evaluări

- GRAPHDocument1 paginăGRAPHShanelle MacajilosÎncă nu există evaluări

- Trainiing BeckhoffDocument45 paginiTrainiing BeckhoffĐại TrầnÎncă nu există evaluări

- Entry and Exit in The Public Charity Sector in TheDocument29 paginiEntry and Exit in The Public Charity Sector in TheBhavesh TrivediÎncă nu există evaluări

- Ecopetrol-CCI Asphalt Market Update - Feb162022Document26 paginiEcopetrol-CCI Asphalt Market Update - Feb162022Fabián Quesada UribeÎncă nu există evaluări

- Trade Integration in Latin America and The Caribbean: Hype, Hope, and RealityDocument10 paginiTrade Integration in Latin America and The Caribbean: Hype, Hope, and Realitysteve britoÎncă nu există evaluări

- Mariana Mazzucato Beyond Markert FailureDocument36 paginiMariana Mazzucato Beyond Markert FailureFrancisco Gallo MÎncă nu există evaluări

- Pedoman Dan Checklist Monitoring Switch 190815Document114 paginiPedoman Dan Checklist Monitoring Switch 190815uptpkm jeruklegiduaÎncă nu există evaluări

- The Plateau in Cinema Attendances and Drop in Video Sales in The UK The Role of Digital Leisure Substitutes 2006 10 10Document25 paginiThe Plateau in Cinema Attendances and Drop in Video Sales in The UK The Role of Digital Leisure Substitutes 2006 10 10Eliza L. KormazopoulosÎncă nu există evaluări

- Fall Chinook Summary 1977 - To - 2015Document1 paginăFall Chinook Summary 1977 - To - 2015Mark SherwoodÎncă nu există evaluări

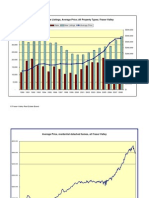

- Fraser Valley Real Estate Stats January '09Document12 paginiFraser Valley Real Estate Stats January '09HudsonHomeTeamÎncă nu există evaluări

- Assignment 1 - AirlineDocument16 paginiAssignment 1 - AirlineArthur GodderisÎncă nu există evaluări

- Public Safety Forum Woodrow 01.23.20Document32 paginiPublic Safety Forum Woodrow 01.23.20Quinton ChandlerÎncă nu există evaluări

- CF Export 29 04 2023Document9 paginiCF Export 29 04 2023Shubham KumarÎncă nu există evaluări

- Market Environment - Inflation Comments1Document8 paginiMarket Environment - Inflation Comments1zabalamgÎncă nu există evaluări

- Presentation GeothermalDocument5 paginiPresentation GeothermalYudexÎncă nu există evaluări

- ICICI Prudential Bharat Consumption Fund Series 2 INVESTOR PPT FinalDocument21 paginiICICI Prudential Bharat Consumption Fund Series 2 INVESTOR PPT FinalvistascanÎncă nu există evaluări

- Property Boom and Banking Bust: The Role of Commercial Lending in the Bankruptcy of BanksDe la EverandProperty Boom and Banking Bust: The Role of Commercial Lending in the Bankruptcy of BanksÎncă nu există evaluări

- Risk Management in Banking Cover and ContentDocument2 paginiRisk Management in Banking Cover and ContentlmmhÎncă nu există evaluări

- 14 Principles of ManagementDocument5 pagini14 Principles of ManagementlmmhÎncă nu există evaluări

- Chapter-17 Bank Management - Lending To Business Firms and Pricing Business LoansDocument41 paginiChapter-17 Bank Management - Lending To Business Firms and Pricing Business Loanslmmh50% (2)

- 1416490317Document2 pagini1416490317Anonymous sRkitXÎncă nu există evaluări

- We Don't Need No MBADocument9 paginiWe Don't Need No MBAsharad_khandelwal_2Încă nu există evaluări

- Fruit LeathersDocument4 paginiFruit LeathersAmmon FelixÎncă nu există evaluări

- Public Utility Accounting Manual 2018Document115 paginiPublic Utility Accounting Manual 2018effieladureÎncă nu există evaluări

- Ps 202PET Manual enDocument7 paginiPs 202PET Manual enStiv KisÎncă nu există evaluări

- Brochure For New HiresDocument11 paginiBrochure For New HiresroseÎncă nu există evaluări

- Friday Night Mishaps, Listening Plus TasksDocument3 paginiFriday Night Mishaps, Listening Plus TasksCristina Stoian100% (1)

- Vocab Money HeistDocument62 paginiVocab Money HeistCivil EngineeringÎncă nu există evaluări

- Trabajos de InglésDocument6 paginiTrabajos de Inglésliztmmm35Încă nu există evaluări

- Towards (De-) Financialisation: The Role of The State: Ewa KarwowskiDocument27 paginiTowards (De-) Financialisation: The Role of The State: Ewa KarwowskieconstudentÎncă nu există evaluări

- C Programming Bit Bank U-1, U-2Document17 paginiC Programming Bit Bank U-1, U-2HariahÎncă nu există evaluări

- Arendi v. GoogleDocument16 paginiArendi v. GooglePriorSmartÎncă nu există evaluări

- Masters Thesis Oral Reading For Masters in Education ST Xavier ED386687Document238 paginiMasters Thesis Oral Reading For Masters in Education ST Xavier ED386687Bruce SpielbauerÎncă nu există evaluări

- Alamat NG BatangasDocument2 paginiAlamat NG BatangasGiennon Arth LimÎncă nu există evaluări

- Dela Cruz vs. Atty. DimaanoDocument8 paginiDela Cruz vs. Atty. DimaanoMarga CastilloÎncă nu există evaluări

- Missions ETC 2020 SchemesOfWarDocument10 paginiMissions ETC 2020 SchemesOfWarDanieleBisignanoÎncă nu există evaluări

- Ring Spinning Machine LR 6/S Specification and Question AnswerDocument15 paginiRing Spinning Machine LR 6/S Specification and Question AnswerPramod Sonbarse100% (3)

- 2.peace Treaties With Defeated PowersDocument13 pagini2.peace Treaties With Defeated PowersTENDAI MAVHIZAÎncă nu există evaluări

- Formalities in Land LawDocument4 paginiFormalities in Land LawCalum Parfitt100% (1)

- Axe in Pakistan PDFDocument22 paginiAxe in Pakistan PDFAdarsh BansalÎncă nu există evaluări

- Tiny House 2020: Less House, More HomeDocument11 paginiTiny House 2020: Less House, More HomeVanshika SpeedyÎncă nu există evaluări

- DS ClozapineDocument3 paginiDS ClozapineMiggsÎncă nu există evaluări

- Coles Stategic AssessmentDocument10 paginiColes Stategic AssessmentRichardÎncă nu există evaluări

- Volume 1Document17 paginiVolume 1Anant RamÎncă nu există evaluări