S-ar putea să vă placă și

- MASDocument46 paginiMASKyll Marcos0% (1)

- HO9 - Decentralized and Segment Reporting, Quantitative Techniques, and Standard Costing PDFDocument7 paginiHO9 - Decentralized and Segment Reporting, Quantitative Techniques, and Standard Costing PDFPATRICIA PEREZÎncă nu există evaluări

- 1.3 Responsibility Accounting Problems AnswersDocument5 pagini1.3 Responsibility Accounting Problems AnswersAsnarizah PakinsonÎncă nu există evaluări

- Management Accounting Information For Activity and Process DecisionsDocument30 paginiManagement Accounting Information For Activity and Process DecisionsCarmelie CumigadÎncă nu există evaluări

- Unit variable costs change proportionally to activityDocument2 paginiUnit variable costs change proportionally to activityJasmin Artates Aquino100% (1)

- ToaDocument5 paginiToaGelyn CruzÎncă nu există evaluări

- 4 Responsibility and Transfer Pricing Part 1Document10 pagini4 Responsibility and Transfer Pricing Part 1Riz CanoyÎncă nu există evaluări

- Vertical Analysis To Financial StatementsDocument8 paginiVertical Analysis To Financial StatementsumeshÎncă nu există evaluări

- Quiz 1 ConsulDocument4 paginiQuiz 1 ConsulJenelyn Pontiveros40% (5)

- Responsibility Accounting and Reporting: Multiple ChoiceDocument23 paginiResponsibility Accounting and Reporting: Multiple ChoiceARISÎncă nu există evaluări

- Chap 010Document147 paginiChap 010Khang HuynhÎncă nu există evaluări

- FarDocument5 paginiFarMaria Fatima AlambraÎncă nu există evaluări

- Angelo - Chapter 10 Operating LeaseDocument8 paginiAngelo - Chapter 10 Operating LeaseAngelo Andro Suan100% (1)

- Code of Ethics for AccountantsDocument9 paginiCode of Ethics for AccountantsJesfer Van DioayanÎncă nu există evaluări

- Bsa 2202 SCM PrelimDocument17 paginiBsa 2202 SCM PrelimKezia SantosidadÎncă nu există evaluări

- ACFrOgC2r9bE9HvuYvxYtUf46A7BnwrhdqbDelEEwU ZdG-lkedjoc9wabHHL2kMRBzhHg1gW W7Document21 paginiACFrOgC2r9bE9HvuYvxYtUf46A7BnwrhdqbDelEEwU ZdG-lkedjoc9wabHHL2kMRBzhHg1gW W7Elizalen MacarilayÎncă nu există evaluări

- c2 2Document3 paginic2 2Kath LeynesÎncă nu există evaluări

- ABC and Standard CostingDocument16 paginiABC and Standard CostingCarlo QuinlogÎncă nu există evaluări

- AIR - CorporateDocument5 paginiAIR - CorporateRaz JisrylÎncă nu există evaluări

- Chapter 7 ProblemsDocument4 paginiChapter 7 ProblemsZyraÎncă nu există evaluări

- Strategic Costing and Management SystemsDocument21 paginiStrategic Costing and Management Systemsambrosia96Încă nu există evaluări

- Management Advisory Services Solution to ProblemDocument13 paginiManagement Advisory Services Solution to ProblemMIKKOÎncă nu există evaluări

- October 2010 Business Law & Taxation Final Pre-BoardDocument11 paginiOctober 2010 Business Law & Taxation Final Pre-BoardPatrick ArazoÎncă nu există evaluări

- Hansen Aise Im Ch16Document55 paginiHansen Aise Im Ch16Daniel NababanÎncă nu există evaluări

- TB Chapter12Document33 paginiTB Chapter12CGÎncă nu există evaluări

- Quiz Number One Without AnswerDocument8 paginiQuiz Number One Without AnswerKpop updates 24/7Încă nu există evaluări

- La Consolacion College Manila Managerial Accounting 1 QuizDocument5 paginiLa Consolacion College Manila Managerial Accounting 1 QuizDeniece RonquilloÎncă nu există evaluări

- Math 006B - Module 4 HypothesisDocument4 paginiMath 006B - Module 4 Hypothesisaey de guzmanÎncă nu există evaluări

- Cost-Volume-Profit Analysis: 2,000 Units and $100,000 of RevenuesDocument14 paginiCost-Volume-Profit Analysis: 2,000 Units and $100,000 of RevenuesMa. Alexandra Teddy BuenÎncă nu există evaluări

- Chap 8 Responsibility AccountingDocument51 paginiChap 8 Responsibility AccountingXel Joe BahianÎncă nu există evaluări

- ReceivablesDocument17 paginiReceivablesJaspreet GillÎncă nu există evaluări

- PAS 11: Long-term construction contractsDocument5 paginiPAS 11: Long-term construction contractsLester John Mendi0% (1)

- 01 x01 Basic ConceptsDocument10 pagini01 x01 Basic ConceptsXandae MempinÎncă nu există evaluări

- Answer2 TaDocument13 paginiAnswer2 TaJohn BryanÎncă nu există evaluări

- Long-Term Construction Contracts and FranchisingDocument16 paginiLong-Term Construction Contracts and FranchisingAlexis SosingÎncă nu există evaluări

- Tactical DecisionDocument2 paginiTactical DecisionLovely Del MundoÎncă nu există evaluări

- Fischer - Pship LiquiDocument7 paginiFischer - Pship LiquiShawn Michael DoluntapÎncă nu există evaluări

- Chapter10.Standard Costing Operational Performance Measures and The Balanced Scorecard PDFDocument36 paginiChapter10.Standard Costing Operational Performance Measures and The Balanced Scorecard PDFJudy Anne SalucopÎncă nu există evaluări

- Responsibility Acctg Transfer Pricing GP Analysis 1Document21 paginiResponsibility Acctg Transfer Pricing GP Analysis 1John Bryan100% (1)

- MA PresentationDocument6 paginiMA PresentationbarbaroÎncă nu există evaluări

- Acquisition of Stocks Date of AcquisitionDocument9 paginiAcquisition of Stocks Date of Acquisitiondom baldemorÎncă nu există evaluări

- D15Document12 paginiD15neo14Încă nu există evaluări

- CF Quiz AprilDocument5 paginiCF Quiz Aprilsumeet9surana9744100% (1)

- Installment Sales & Long-Term ConsDocument6 paginiInstallment Sales & Long-Term ConsSirr JeyÎncă nu există evaluări

- Coma Quiz 6 KeyDocument20 paginiComa Quiz 6 KeyMD TARIQUE NOORÎncă nu există evaluări

- Study Guide 3030Document14 paginiStudy Guide 3030arsenal2687100% (1)

- UST AMV ACC 4 QUIZ 1 INVESTMENT EQUITY SECURITIESDocument9 paginiUST AMV ACC 4 QUIZ 1 INVESTMENT EQUITY SECURITIESMildred Angela DingalÎncă nu există evaluări

- Handouts ConsolidationIntercompany Sale of Plant AssetsDocument3 paginiHandouts ConsolidationIntercompany Sale of Plant AssetsCPAÎncă nu există evaluări

- Toa Basic ConceptsDocument44 paginiToa Basic ConceptsKristine WaliÎncă nu există evaluări

- 2011 NATIONAL CPA MOCK BOARD EXAMINATION PRACTICAL ACCOUNTING 2Document6 pagini2011 NATIONAL CPA MOCK BOARD EXAMINATION PRACTICAL ACCOUNTING 2Mary Queen Ramos-UmoquitÎncă nu există evaluări

- Seatwork - Advacc1Document2 paginiSeatwork - Advacc1David DavidÎncă nu există evaluări

- Chapter 19Document9 paginiChapter 19Marc Siblag IIIÎncă nu există evaluări

- TB ch07Document27 paginiTB ch07carolevangelist4657Încă nu există evaluări

- Responsibility Accounting and Transfer Pricing ExplainedDocument14 paginiResponsibility Accounting and Transfer Pricing ExplainedRamm Raven CastilloÎncă nu există evaluări

- Chapter On CVP 2015 - Acc 2Document16 paginiChapter On CVP 2015 - Acc 2nur aqilah ridzuanÎncă nu există evaluări

- AbuegDocument10 paginiAbuegswit_kamoteÎncă nu există evaluări

- 04 x04 Cost-Volume-Profit RelationshipsDocument11 pagini04 x04 Cost-Volume-Profit RelationshipscassandraÎncă nu există evaluări

- 07 X07 A Responsibility Accounting and TP Decentralization and Performance EvaluationDocument11 pagini07 X07 A Responsibility Accounting and TP Decentralization and Performance EvaluationNora Pasa100% (1)

- Responsibility Accounting, Decentralization, and Goal CongruenceDocument10 paginiResponsibility Accounting, Decentralization, and Goal CongruencemonneÎncă nu există evaluări

- 07 X07 A ResponsibilityDocument10 pagini07 X07 A ResponsibilityJune Koo100% (1)

- Donors Tax Theory ExplainedDocument5 paginiDonors Tax Theory ExplainedJoey Acierda BumagatÎncă nu există evaluări

- Estate Tax Problems Quizzer 1104Document10 paginiEstate Tax Problems Quizzer 1104Fate Serrano100% (1)

- Republic Act No. 9520: "Philippine Cooperative Code of 2008"Document9 paginiRepublic Act No. 9520: "Philippine Cooperative Code of 2008"abcdefgÎncă nu există evaluări

- MasDocument27 paginiMaskevinlim186Încă nu există evaluări

- 13 Consolidated Financial StatementDocument5 pagini13 Consolidated Financial StatementabcdefgÎncă nu există evaluări

- AaaaaaaaaaaaaaDocument1 paginăAaaaaaaaaaaaaaabcdefgÎncă nu există evaluări

- AP-5907 CashDocument12 paginiAP-5907 CashAiko E. LaraÎncă nu există evaluări

- Ifric21 PDFDocument8 paginiIfric21 PDFJorreyGarciaOplasÎncă nu există evaluări

- 01 Glossary of Terms December 2002Document20 pagini01 Glossary of Terms December 2002Tracy KayeÎncă nu există evaluări

- CPALE Syllabi 2018 PDFDocument32 paginiCPALE Syllabi 2018 PDFLorraine TomasÎncă nu există evaluări

- PSA 120 Framework of Philippine Standards on AuditingDocument9 paginiPSA 120 Framework of Philippine Standards on AuditingMichael Vincent Buan SuicoÎncă nu există evaluări

- AIS AssDocument2 paginiAIS AssabcdefgÎncă nu există evaluări

- 09 Standard CostingDocument5 pagini09 Standard CostingabcdefgÎncă nu există evaluări

- AaaaaaaaaaaaaaDocument1 paginăAaaaaaaaaaaaaaabcdefgÎncă nu există evaluări

- REGULATORY FRAMEWORK MCQDocument17 paginiREGULATORY FRAMEWORK MCQabcdefgÎncă nu există evaluări

- Due Process StepsDocument12 paginiDue Process StepsabcdefgÎncă nu există evaluări

- P1 Day4 RMDocument15 paginiP1 Day4 RMSharmaine Sur100% (1)

- Prelim Good GovDocument1 paginăPrelim Good GovabcdefgÎncă nu există evaluări

- P1 HSHSJSKDJHSHDocument8 paginiP1 HSHSJSKDJHSHabcdefg0% (1)

- P1 Day1 RMDocument4 paginiP1 Day1 RMabcdefg100% (2)

- Criminal Code September-2014 (Draft)Document27 paginiCriminal Code September-2014 (Draft)Charles MJÎncă nu există evaluări

- 11 Home Office and BranchDocument3 pagini11 Home Office and BranchabcdefgÎncă nu există evaluări

- P1 Day3 RMDocument6 paginiP1 Day3 RMabcdefg0% (2)

- Untitled DocumentDocument1 paginăUntitled DocumentabcdefgÎncă nu există evaluări

- Account Classification and Presentation PDFDocument8 paginiAccount Classification and Presentation PDFKimberly Etulle CellonaÎncă nu există evaluări

- Description Complied MissingDocument2 paginiDescription Complied MissingabcdefgÎncă nu există evaluări

- Smart Goals Worksheet Final 4 Step Process PDFF PDFDocument1 paginăSmart Goals Worksheet Final 4 Step Process PDFF PDFabcdefgÎncă nu există evaluări

- Aud ProbDocument1 paginăAud ProbabcdefgÎncă nu există evaluări

- Deontology Axiology: Citation NeededDocument1 paginăDeontology Axiology: Citation NeededabcdefgÎncă nu există evaluări

- Managment Accountant ACCOW, OpenT, KPP WBDocument6 paginiManagment Accountant ACCOW, OpenT, KPP WBFarahAin FainÎncă nu există evaluări

- Panera BreadDocument23 paginiPanera BreadtomÎncă nu există evaluări

- Final Thesis Daniel Tsegaye Accounting and FinanceDocument48 paginiFinal Thesis Daniel Tsegaye Accounting and FinanceBee TadeleÎncă nu există evaluări

- Cost Accounting For Decision-MakingDocument56 paginiCost Accounting For Decision-MakingRita ChingÎncă nu există evaluări

- Financial Projection: Total Goods Available For SalesDocument7 paginiFinancial Projection: Total Goods Available For SalesClau MagahisÎncă nu există evaluări

- Answer Tutorial 3 Partnership Part 2Document3 paginiAnswer Tutorial 3 Partnership Part 2athirah jamaludin100% (1)

- CFAS Computations PDFDocument40 paginiCFAS Computations PDFJay-B Angelo75% (4)

- تمارين +الحل اداريةDocument14 paginiتمارين +الحل اداريةaec216320136Încă nu există evaluări

- Comman Size Analysis of Income StatementDocument11 paginiComman Size Analysis of Income Statement4 7Încă nu există evaluări

- Shs Abm Gr12 Fabm2 q1 m2 Statement-Of-comprehensive-IncomeDocument14 paginiShs Abm Gr12 Fabm2 q1 m2 Statement-Of-comprehensive-IncomeKye RauleÎncă nu există evaluări

- Basic Accounting-RatiosDocument22 paginiBasic Accounting-RatiosSala SahariÎncă nu există evaluări

- Fiancial Analysis of Rolls RoyceDocument8 paginiFiancial Analysis of Rolls RoyceJohn Jerrin BabuÎncă nu există evaluări

- HorngrenIMA14eSM ch07Document57 paginiHorngrenIMA14eSM ch07manunited83100% (3)

- Chapter 3Document24 paginiChapter 3izai vitorÎncă nu există evaluări

- Twelve-Month Cash Flo YEAR 1: Jan-18 Fiscal Year BeginsDocument1 paginăTwelve-Month Cash Flo YEAR 1: Jan-18 Fiscal Year BeginsTun Izlinda Tun BahardinÎncă nu există evaluări

- Financial Statement AnalysisDocument5 paginiFinancial Statement AnalysisVirgil Kit Augustin AbanillaÎncă nu există evaluări

- Cheesy Lumpianatics BusinessDocument27 paginiCheesy Lumpianatics BusinessYvonne ZabayÎncă nu există evaluări

- hw4 (Answers) R2Document6 paginihw4 (Answers) R2Arslan HafeezÎncă nu există evaluări

- A Study On Ratio Analysis at Amar - Raja Battery LTD, PuneDocument68 paginiA Study On Ratio Analysis at Amar - Raja Battery LTD, PuneAMIT K SINGHÎncă nu există evaluări

- Chapter 17 Solutions 7eDocument46 paginiChapter 17 Solutions 7epenelopegerhardÎncă nu există evaluări

- Profitability and Cash Flow Analysis of Lowe's and Home DepotDocument9 paginiProfitability and Cash Flow Analysis of Lowe's and Home DepotSisiChenÎncă nu există evaluări

- Financial Statment TestDocument3 paginiFinancial Statment TestDerick FloresÎncă nu există evaluări

- Final Fall 2012Document14 paginiFinal Fall 2012Miruna CiteaÎncă nu există evaluări

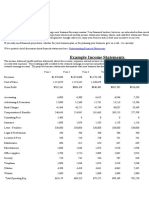

- Example Income Statements: Business Plan Financial ProjectionsDocument3 paginiExample Income Statements: Business Plan Financial ProjectionsSUMANTO SHARANÎncă nu există evaluări

- CH 13Document77 paginiCH 13Mohammed SamyÎncă nu există evaluări

- Chapter 25Document4 paginiChapter 25Xynith Nicole RamosÎncă nu există evaluări

- Financial Accounting Ch04Document57 paginiFinancial Accounting Ch04b2dm2k100% (1)

- Project Finance AssignmentDocument10 paginiProject Finance AssignmentShaketia hallÎncă nu există evaluări

- Midterm Analysis TestDocument33 paginiMidterm Analysis TestDan Andrei BongoÎncă nu există evaluări

- How to File PH Quarterly Income TaxDocument44 paginiHow to File PH Quarterly Income TaxMia Torres100% (1)