S-ar putea să vă placă și

- Cornell - Case Study LBODocument25 paginiCornell - Case Study LBOCommodity100% (2)

- UNIT 1 GlobalizationDocument78 paginiUNIT 1 GlobalizationJuan Castillo67% (3)

- Homeopathy WorkbookDocument90 paginiHomeopathy Workbookapi-3708784100% (15)

- Reportable: Signature Not VerifiedDocument28 paginiReportable: Signature Not VerifiedSachin DabadeÎncă nu există evaluări

- SC's NRA Judgement On Sec.68: Threadbare Analysis of Subsequent DecisionsDocument5 paginiSC's NRA Judgement On Sec.68: Threadbare Analysis of Subsequent DecisionsArchit ShethÎncă nu există evaluări

- Aditya Birla Telecom LTDDocument6 paginiAditya Birla Telecom LTDdeepakÎncă nu există evaluări

- TS 46 ITAT 2021mum Reliance - Infrastructure - LTDDocument6 paginiTS 46 ITAT 2021mum Reliance - Infrastructure - LTDsanket shindeÎncă nu există evaluări

- 15 04 16 Case2Document26 pagini15 04 16 Case2tamanna.vkacaÎncă nu există evaluări

- Income Tax Officer Vs Ms Fussy Financial ITAT Delhi PDFDocument9 paginiIncome Tax Officer Vs Ms Fussy Financial ITAT Delhi PDFkalravÎncă nu există evaluări

- WTM/AB/WRO/WRO/14741/2021-22: Final Order in The Matter of Cash Cow Broking & Advisory SolutionsDocument20 paginiWTM/AB/WRO/WRO/14741/2021-22: Final Order in The Matter of Cash Cow Broking & Advisory SolutionsAarnav SinghÎncă nu există evaluări

- Manali Investments, Mumbai Vs AssesseeDocument7 paginiManali Investments, Mumbai Vs AssesseeBibhuChhotrayÎncă nu există evaluări

- TML Rights Issue LofDocument445 paginiTML Rights Issue LofPriya SumanÎncă nu există evaluări

- Mumbai Itat Judgement On Share Application Money 2021Document41 paginiMumbai Itat Judgement On Share Application Money 2021CA Amit RajaÎncă nu există evaluări

- Bankers Customer RelationshipDocument9 paginiBankers Customer RelationshipAnmol GoswamiÎncă nu există evaluări

- Tax Department Notice To NDTVDocument32 paginiTax Department Notice To NDTVThe WireÎncă nu există evaluări

- Term Paper of Law PaperDocument18 paginiTerm Paper of Law PaperreyazmbaÎncă nu există evaluări

- ST ST: © The Institute of Chartered Accountants of IndiaDocument19 paginiST ST: © The Institute of Chartered Accountants of IndiaÑïkêţ BäûðhåÎncă nu există evaluări

- Abhay Manohar Sapre and Ms Indu Malhotra, Jj. Special Leave To Appeal (C) Nos. 7913 of 2018 OCTOBER 31, 2018Document4 paginiAbhay Manohar Sapre and Ms Indu Malhotra, Jj. Special Leave To Appeal (C) Nos. 7913 of 2018 OCTOBER 31, 2018Kartik BhargavaÎncă nu există evaluări

- QMF SAIDocument63 paginiQMF SAItanish gehlotÎncă nu există evaluări

- Mr. Lagadapati Ramesh Vs Mrs. Ramanathan Bhuvaneshwari NCLAT DelhiDocument41 paginiMr. Lagadapati Ramesh Vs Mrs. Ramanathan Bhuvaneshwari NCLAT DelhiAyantika MondalÎncă nu există evaluări

- Satyamg 8 090522093818 Phpapp02Document19 paginiSatyamg 8 090522093818 Phpapp02sumedh1287Încă nu există evaluări

- Sec 68 - Case LawsDocument2 paginiSec 68 - Case LawsShreÎncă nu există evaluări

- 4TH PROGRESS REPORT-sachinDocument9 pagini4TH PROGRESS REPORT-sachinRishabh SinghÎncă nu există evaluări

- Page 1 of 29Document29 paginiPage 1 of 29vv222vvÎncă nu există evaluări

- Judgment Sheet in The Lahore High Court, Lahore Judicial DepartmentDocument30 paginiJudgment Sheet in The Lahore High Court, Lahore Judicial DepartmentApp SUgessterÎncă nu există evaluări

- (1986) 53 Tax 122 (S.C.Pak) ) Sh. M. Imail & CODocument9 pagini(1986) 53 Tax 122 (S.C.Pak) ) Sh. M. Imail & COMansoor AhmadÎncă nu există evaluări

- Shares STCG Business IncomeDocument8 paginiShares STCG Business IncomerakeshvaÎncă nu există evaluări

- Mohit Agro Gujarat AmbujaDocument20 paginiMohit Agro Gujarat AmbujaMuskan KhatriÎncă nu există evaluări

- Ncrds Sterling Institute of Management Studies Financial Market & Institution. Topic-Listing of Securities. Submitted To: Prof. Aradhana TiwariDocument27 paginiNcrds Sterling Institute of Management Studies Financial Market & Institution. Topic-Listing of Securities. Submitted To: Prof. Aradhana TiwariIrfan MalangÎncă nu există evaluări

- Hexaware DelistingDocument48 paginiHexaware DelistingNihal YnÎncă nu există evaluări

- Ca Final Advanced ManagementDocument114 paginiCa Final Advanced ManagementMohammed IrfanÎncă nu există evaluări

- Moot Problem ICSI - FinalDocument5 paginiMoot Problem ICSI - FinalBodhisatya DeyÎncă nu există evaluări

- Adjudication Order in Respect of Cepham Organics Ltd.Document6 paginiAdjudication Order in Respect of Cepham Organics Ltd.Shyam SunderÎncă nu există evaluări

- Mayfair 101 Response To Dye and Co Decembre 16, 2020Document72 paginiMayfair 101 Response To Dye and Co Decembre 16, 2020Toby VueÎncă nu există evaluări

- Ca FinalDocument11 paginiCa FinalHadia HÎncă nu există evaluări

- Ashiana HousingDocument252 paginiAshiana Housingsandip_banerjeeÎncă nu există evaluări

- Faq ScoresDocument17 paginiFaq Scoresaabhi_922Încă nu există evaluări

- Interim Order Cum Show Cause Notice in The Matter of Bhabiswajyoti Infrastructure India LimitedDocument16 paginiInterim Order Cum Show Cause Notice in The Matter of Bhabiswajyoti Infrastructure India LimitedShyam SunderÎncă nu există evaluări

- Vaswani Ipo Scam: Case FactsDocument5 paginiVaswani Ipo Scam: Case FactsNawazish KhanÎncă nu există evaluări

- Paper - 2: Auditing Questions: Accounting Treatment of The Above Receipt of Rs. 50 Lacs?Document20 paginiPaper - 2: Auditing Questions: Accounting Treatment of The Above Receipt of Rs. 50 Lacs?tpsbtpsbtpsbÎncă nu există evaluări

- Case: 1: 11-cv-00672 Assigned To: Huvelle, Ellen S. Assign. Date: Description: General CivilDocument16 paginiCase: 1: 11-cv-00672 Assigned To: Huvelle, Ellen S. Assign. Date: Description: General CivilKelvin Lim Wei LiangÎncă nu există evaluări

- Before The National Company Law Tribunal Mumbai Bench: Per: M. K. Shrawat, Member (J)Document11 paginiBefore The National Company Law Tribunal Mumbai Bench: Per: M. K. Shrawat, Member (J)ajsdkhkljhkjÎncă nu există evaluări

- Capital ReductionDocument17 paginiCapital Reductionsridhar reddyÎncă nu există evaluări

- Weekly Test of AccountsDocument6 paginiWeekly Test of AccountsAMIN BUHARI ABDUL KHADER100% (1)

- Chapter # 1 Issuance of SharesDocument16 paginiChapter # 1 Issuance of SharesRooh Ullah KhanÎncă nu există evaluări

- Mut Fin ProspDocument504 paginiMut Fin Prospvivekrajbhilai5850Încă nu există evaluări

- Adjudication Order in Respect of M/s Ambe Hotel & Resorts LimitedDocument8 paginiAdjudication Order in Respect of M/s Ambe Hotel & Resorts LimitedShyam SunderÎncă nu există evaluări

- Kingfisher Capital Clo LTD Vs Commissioner of Income Tax, On 27 March, 2019Document34 paginiKingfisher Capital Clo LTD Vs Commissioner of Income Tax, On 27 March, 2019Adv Ratnesh DubeÎncă nu există evaluări

- 8990 - 2020 Definitive Information Statement (And Annexes)Document349 pagini8990 - 2020 Definitive Information Statement (And Annexes)Jonathan AccountingÎncă nu există evaluări

- ACAPL - Valuation Report - May, 2023Document16 paginiACAPL - Valuation Report - May, 2023Shashi Bhushan PrinceÎncă nu există evaluări

- CA Inter Law Ans Dec 2021Document21 paginiCA Inter Law Ans Dec 2021Punith KumarÎncă nu există evaluări

- Cheviot ColtdDocument41 paginiCheviot ColtdSubscriptionÎncă nu există evaluări

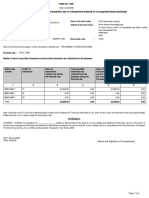

- Form For Evidence of Payment of Securities Transaction Tax On Transactions Entered in A Recognised Stock ExchangeDocument2 paginiForm For Evidence of Payment of Securities Transaction Tax On Transactions Entered in A Recognised Stock ExchangemanishaÎncă nu există evaluări

- 2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioDocument7 pagini2023 153 Taxmann Com 686 Punjab Haryana 01 03 2023 Mahavir Rice Mills Vs CommissioThe Chartered Professional NewsletterÎncă nu există evaluări

- Project Lakshya Letter of Offer January 29 2024 Filing VersionDocument720 paginiProject Lakshya Letter of Offer January 29 2024 Filing VersionJuhi VaryaniÎncă nu există evaluări

- Adjudication Order in Respect of Twenty First Century Capitals Ltd. (Now Known As Spicebulls Investments LTD.)Document6 paginiAdjudication Order in Respect of Twenty First Century Capitals Ltd. (Now Known As Spicebulls Investments LTD.)Shyam SunderÎncă nu există evaluări

- Constructive Dismissal, Significant Loss of WagesDocument48 paginiConstructive Dismissal, Significant Loss of WagesJenson ElectricalÎncă nu există evaluări

- Indian Oil Corporation Limited: Letter of Offer This Document Is Important and Requires Your Immediate AttentionDocument54 paginiIndian Oil Corporation Limited: Letter of Offer This Document Is Important and Requires Your Immediate AttentionJeetSoniÎncă nu există evaluări

- Letter of OfferRDocument48 paginiLetter of OfferRishuv6733Încă nu există evaluări

- (2001) 117 Taxman 522 (Calcutta) / (2000) 241 ITR 494 (Calcutta) / (2000) 158 CTR 361 (Calcutta) (06-09-1999)Document2 pagini(2001) 117 Taxman 522 (Calcutta) / (2000) 241 ITR 494 (Calcutta) / (2000) 158 CTR 361 (Calcutta) (06-09-1999)BuntyÎncă nu există evaluări

- Letter of Offer - 180820201703Document283 paginiLetter of Offer - 180820201703amit jaatÎncă nu există evaluări

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaDe la EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaÎncă nu există evaluări

- The Sarbanes-Oxley Act: costs, benefits and business impactsDe la EverandThe Sarbanes-Oxley Act: costs, benefits and business impactsÎncă nu există evaluări

- Taxguru - In-Section 147 Reason To Believe 20 Case LawsDocument5 paginiTaxguru - In-Section 147 Reason To Believe 20 Case LawsrdaranÎncă nu există evaluări

- Taxguru - In-Understanding of 44AB Tax AuditDocument8 paginiTaxguru - In-Understanding of 44AB Tax AuditrdaranÎncă nu există evaluări

- Sumanth B L PDFDocument137 paginiSumanth B L PDFrdaranÎncă nu există evaluări

- Taxguru - in-Re-Opening Not Allowed For Issue Investigated During Original AssessmentDocument9 paginiTaxguru - in-Re-Opening Not Allowed For Issue Investigated During Original AssessmentrdaranÎncă nu există evaluări

- Classical Homeopathy - Liquid Administration of LM PotenciesDocument1 paginăClassical Homeopathy - Liquid Administration of LM PotenciesrdaranÎncă nu există evaluări

- Excel 51 TipsDocument59 paginiExcel 51 Tipsklodiklodi100% (1)

- Sumanth B L PDFDocument137 paginiSumanth B L PDFrdaranÎncă nu există evaluări

- Laxman Das Khandelwal 143 2 292BBDocument8 paginiLaxman Das Khandelwal 143 2 292BBrdaranÎncă nu există evaluări

- Bach RepertoryDocument107 paginiBach Repertorymystic2012100% (17)

- Ear & Medicines PDFDocument65 paginiEar & Medicines PDFrdaranÎncă nu există evaluări

- Ear & Medicines PDFDocument65 paginiEar & Medicines PDFrdaranÎncă nu există evaluări

- PrathamDocument8 paginiPrathamrdaranÎncă nu există evaluări

- 170 - Borrowed Satisfaction by K NathDocument8 pagini170 - Borrowed Satisfaction by K NathrdaranÎncă nu există evaluări

- Please Answer Each of The Questions CarefullyDocument3 paginiPlease Answer Each of The Questions CarefullyrdaranÎncă nu există evaluări

- Indian and Eastern Newspaper ... Vs Commissioner of Income Tax, New ... On 31 August, 1979Document12 paginiIndian and Eastern Newspaper ... Vs Commissioner of Income Tax, New ... On 31 August, 1979Ankit SijariyaÎncă nu există evaluări

- Ear & MedicinesDocument65 paginiEar & MedicinesrdaranÎncă nu există evaluări

- Case LawDocument6 paginiCase LawrdaranÎncă nu există evaluări

- Acute Bach QuestionnaireDocument5 paginiAcute Bach QuestionnairerdaranÎncă nu există evaluări

- Acute Bach QuestionnaireDocument5 paginiAcute Bach QuestionnairerdaranÎncă nu există evaluări

- Questionnaire 1 4Document4 paginiQuestionnaire 1 4rdaranÎncă nu există evaluări

- IoanaSalajanu CandidateSurveyDocument8 paginiIoanaSalajanu CandidateSurveyInjustice WatchÎncă nu există evaluări

- Assignment by Way of Security DigestsDocument12 paginiAssignment by Way of Security DigestsKyle SubidoÎncă nu există evaluări

- Guide To Original Issue Discount (OID) Instruments: Publication 1212Document17 paginiGuide To Original Issue Discount (OID) Instruments: Publication 1212api-242377800Încă nu există evaluări

- Credit Card Market in IndiaDocument62 paginiCredit Card Market in IndiaDavid BarlaÎncă nu există evaluări

- KabirdassDocument258 paginiKabirdasssumitkishanpuriaÎncă nu există evaluări

- CHP 13 Testbank 2Document15 paginiCHP 13 Testbank 2judyÎncă nu există evaluări

- ADB Public Private Partnership HandbookDocument101 paginiADB Public Private Partnership HandbookGiovanniStirelliÎncă nu există evaluări

- FM CHAPTER 3 THREE. PPT SlidesDocument84 paginiFM CHAPTER 3 THREE. PPT SlidesAlayou TeferaÎncă nu există evaluări

- Postal Auction No 13: The Revenue SocietyDocument20 paginiPostal Auction No 13: The Revenue SocietyKenneth ChandlerÎncă nu există evaluări

- Bai Bitamal Ajil Introduction at UniklDocument14 paginiBai Bitamal Ajil Introduction at UniklLee WongÎncă nu există evaluări

- Art. 1884-1886Document5 paginiArt. 1884-1886Jerald-Edz Tam AbonÎncă nu există evaluări

- Real Estate Investing Purchase AgreementDocument2 paginiReal Estate Investing Purchase Agreementbernel069100% (1)

- I.D. Theft Hits Delphos: Elphos EraldDocument10 paginiI.D. Theft Hits Delphos: Elphos EraldThe Delphos HeraldÎncă nu există evaluări

- 154-155 Voca PDFDocument2 pagini154-155 Voca PDFAnabel Yanina Hilari HuillcaÎncă nu există evaluări

- Eustace Mullins-Secrets of The Federal Reserve 1952Document172 paginiEustace Mullins-Secrets of The Federal Reserve 1952Lucas Muniz Hadade50% (2)

- Difference Between Cheque and Bill of Exchange: MeaningDocument6 paginiDifference Between Cheque and Bill of Exchange: MeaningDeeptangshu KarÎncă nu există evaluări

- Warner Company Statement of Cash FlowsDocument2 paginiWarner Company Statement of Cash FlowsKailash KumarÎncă nu există evaluări

- WIHCON Road To Homeownership EbookDocument9 paginiWIHCON Road To Homeownership EbookAnn VictoriaÎncă nu există evaluări

- Cash Basis Accrual Basis Single Entry Error Correction ASSIGNMENT 1Document3 paginiCash Basis Accrual Basis Single Entry Error Correction ASSIGNMENT 1Christine BÎncă nu există evaluări

- Report On Credit Information Bureau SystemDocument26 paginiReport On Credit Information Bureau Systemshubham97Încă nu există evaluări

- Double Taxation 1Document57 paginiDouble Taxation 1arah baelÎncă nu există evaluări

- Cost of Capital ProblemsDocument5 paginiCost of Capital ProblemsYusairah Benito DomatoÎncă nu există evaluări

- Contract Guarantee and Bond Assignment Contract 2Document8 paginiContract Guarantee and Bond Assignment Contract 2Salman malikÎncă nu există evaluări

- Philippine Legal FormatsDocument38 paginiPhilippine Legal FormatsAnn DyÎncă nu există evaluări

- GST PDFDocument81 paginiGST PDFPankaj JainÎncă nu există evaluări

- Principles of Business Law-Negotiable InstrumentDocument16 paginiPrinciples of Business Law-Negotiable Instrumentjohn wongÎncă nu există evaluări

- The Collapse of Securitization: From Subprimes To Global Credit CrunchDocument14 paginiThe Collapse of Securitization: From Subprimes To Global Credit CrunchFernanda UltremareÎncă nu există evaluări

- IIE DetailsDocument19 paginiIIE Detailssandip_banerjeeÎncă nu există evaluări