S-ar putea să vă placă și

- Feb 2020 Statement PDFDocument2 paginiFeb 2020 Statement PDFSandeep KumarÎncă nu există evaluări

- DSInnovate Fintech Report 2021Document76 paginiDSInnovate Fintech Report 2021Emil Fahmi YakhyaÎncă nu există evaluări

- Dobuy Whitepaper PDFDocument17 paginiDobuy Whitepaper PDFOsantucoÎncă nu există evaluări

- 2021 Mckinsey Global Payments ReportDocument40 pagini2021 Mckinsey Global Payments ReportChandulalÎncă nu există evaluări

- HHLL Trading StrategyDocument15 paginiHHLL Trading Strategyachiro0707100% (2)

- Puschmann2017 FintechDocument8 paginiPuschmann2017 FintecharushichananaÎncă nu există evaluări

- We Are InvestocryptDocument9 paginiWe Are InvestocryptAnonymous SdWPyjÎncă nu există evaluări

- Swift RTP PDFDocument15 paginiSwift RTP PDFmais dawasÎncă nu există evaluări

- Innovation in Payments Opportunities and Challenges For EMDEsDocument55 paginiInnovation in Payments Opportunities and Challenges For EMDEsluisÎncă nu există evaluări

- Fintech in Asean 2021Document49 paginiFintech in Asean 2021dl1983Încă nu există evaluări

- Impact of Financial Technology On Payment and Lending in AsiaDocument19 paginiImpact of Financial Technology On Payment and Lending in AsiaADBI EventsÎncă nu există evaluări

- Uob - Fintech in AseanDocument49 paginiUob - Fintech in AseanTrader CatÎncă nu există evaluări

- ACI Prime Time For Real-Time Report PDFDocument47 paginiACI Prime Time For Real-Time Report PDFAnand ArgÎncă nu există evaluări

- Better Than Cash Alliance China Report April 2017Document72 paginiBetter Than Cash Alliance China Report April 2017CrowdfundInsider100% (1)

- E Naira Digital Currency and Financial Performance of Listed Deposit Money Banks in NigeriaDocument8 paginiE Naira Digital Currency and Financial Performance of Listed Deposit Money Banks in NigeriaEditor IJTSRDÎncă nu există evaluări

- F 3251 SuerfDocument9 paginiF 3251 SuerfMai ngoc thangÎncă nu există evaluări

- The Future of Payment in AfricaDocument17 paginiThe Future of Payment in AfricaNegera AbetuÎncă nu există evaluări

- The Future of PaymentsDocument40 paginiThe Future of Paymentsanon_903741391Încă nu există evaluări

- Digital Transformation Across European Banking GroupsDocument12 paginiDigital Transformation Across European Banking GroupsVladimir TofoskiÎncă nu există evaluări

- Tink - The Future of Payments Is OpenDocument46 paginiTink - The Future of Payments Is OpenDavid HelmanÎncă nu există evaluări

- F 3251 SuerfDocument9 paginiF 3251 SuerfMai ngoc thangÎncă nu există evaluări

- Digital Payment TransofmaionDocument19 paginiDigital Payment TransofmaiontreflatfaceÎncă nu există evaluări

- The Fintech Edge: First Edition: Peer - To-Peer LendingDocument32 paginiThe Fintech Edge: First Edition: Peer - To-Peer LendingMaria HanyÎncă nu există evaluări

- FinTech MasterClassDocument30 paginiFinTech MasterClassannasserÎncă nu există evaluări

- Galitt SBS Request To Pay White Paper - VF 1Document37 paginiGalitt SBS Request To Pay White Paper - VF 1Erinda MalajÎncă nu există evaluări

- The Future of PaymentsDocument75 paginiThe Future of Paymentssuraj GGÎncă nu există evaluări

- Aiaze Mitha-Amarante Consulting - MFS Intitiatives From Around The World, Myths and RealityDocument22 paginiAiaze Mitha-Amarante Consulting - MFS Intitiatives From Around The World, Myths and RealityPercyÎncă nu există evaluări

- Digital Banks: A Proposal For Licensing & Regulatory Regime For IndiaDocument70 paginiDigital Banks: A Proposal For Licensing & Regulatory Regime For IndiaKashish GamreÎncă nu există evaluări

- AI-powered Digital PaymentsDocument5 paginiAI-powered Digital PaymentsNeha LodheÎncă nu există evaluări

- Interoperability and Government To People and People To Government E0a5e18de9Document22 paginiInteroperability and Government To People and People To Government E0a5e18de9belisaÎncă nu există evaluări

- Payments InnovationDocument4 paginiPayments InnovationEditor IJTSRDÎncă nu există evaluări

- The Effect of Cashless Banking On Ethiopian EconomyDocument11 paginiThe Effect of Cashless Banking On Ethiopian EconomyAnonymous kbmKQLe0JÎncă nu există evaluări

- The 2022 Mckinsey Global Payments ReportDocument53 paginiThe 2022 Mckinsey Global Payments ReportIrene SkorlifeÎncă nu există evaluări

- A Retail CBDC - Economic Considerations in The Singapore ContextDocument55 paginiA Retail CBDC - Economic Considerations in The Singapore ContextmananDgreatÎncă nu există evaluări

- CL1 - CBDCs - An Opportunity For The Monetary System PDFDocument31 paginiCL1 - CBDCs - An Opportunity For The Monetary System PDFKELLY GUADALUPE RAMIREZ DE LA CRUZÎncă nu există evaluări

- Payment Methods Report 2017Document101 paginiPayment Methods Report 2017Stefan StefÎncă nu există evaluări

- The State of Digital Payments in The Philippines-Feb20 PDFDocument96 paginiThe State of Digital Payments in The Philippines-Feb20 PDFKeane100% (1)

- Velmie PDFDocument22 paginiVelmie PDFmerahuldjoshiÎncă nu există evaluări

- Retail Banking MarketforceDocument60 paginiRetail Banking MarketforceYougal MalikÎncă nu există evaluări

- Digital Currencies - Bank For International SettlementsDocument17 paginiDigital Currencies - Bank For International SettlementsAtish KissoonÎncă nu există evaluări

- Ida Wolden Bache: Central Bank Digital Currency and Real-Time PaymentsDocument6 paginiIda Wolden Bache: Central Bank Digital Currency and Real-Time PaymentsForkLogÎncă nu există evaluări

- Nchain CBDC PlaybookDocument40 paginiNchain CBDC PlaybookLinh Nguyễn Hoàng TúÎncă nu există evaluări

- NPCI Magazine - TXN NXT Vol 2 - CollateralDocument76 paginiNPCI Magazine - TXN NXT Vol 2 - CollateraldupeshÎncă nu există evaluări

- RakutenDocument20 paginiRakutenIgna BÎncă nu există evaluări

- Content Dam Deloitte Ce Documents Financial-Services Ce-Digital-Banking-Maturity-2020Document37 paginiContent Dam Deloitte Ce Documents Financial-Services Ce-Digital-Banking-Maturity-2020Nikhil RajÎncă nu există evaluări

- Joining The Next Generation of Digital Banks in AsiaDocument12 paginiJoining The Next Generation of Digital Banks in AsiaChi PhamÎncă nu există evaluări

- دور التكنولوجيا المالية في عصر ما بعد كوفيدDocument31 paginiدور التكنولوجيا المالية في عصر ما بعد كوفيدsm3977263Încă nu există evaluări

- Digital Innovation, Data Revolution and Central Bank Digital CurrencyDocument21 paginiDigital Innovation, Data Revolution and Central Bank Digital CurrencyBrigette DomingoÎncă nu există evaluări

- 16af303e Neobank Quarterly Report q4 PDFDocument15 pagini16af303e Neobank Quarterly Report q4 PDFM Ikhsan N FÎncă nu există evaluări

- Omni Fintech Digital Payments and Banking A Digital RevolutionDocument11 paginiOmni Fintech Digital Payments and Banking A Digital RevolutionvicgreerÎncă nu există evaluări

- EDDY SATRIYA-WANTIKNAS TransformationFINALDocument37 paginiEDDY SATRIYA-WANTIKNAS TransformationFINALPermana BakrieÎncă nu există evaluări

- Beyond Mobile Payments: Exploring The Evolution and Future of FintechDocument6 paginiBeyond Mobile Payments: Exploring The Evolution and Future of FintechInternational Journal of Innovative Science and Research TechnologyÎncă nu există evaluări

- Digitalization in Banking SectorDocument7 paginiDigitalization in Banking SectorEditor IJTSRDÎncă nu există evaluări

- Fintech Wave in IndiaDocument7 paginiFintech Wave in IndiaT ForsythÎncă nu există evaluări

- Digital Transformation in India - S Banking SectorDocument4 paginiDigital Transformation in India - S Banking SectorT ForsythÎncă nu există evaluări

- Payment Revolution: Preparing For Participation : R. GandhiDocument4 paginiPayment Revolution: Preparing For Participation : R. GandhihvenkiÎncă nu există evaluări

- Fintech and Transformation in Financial Services: Seminar Report OnDocument25 paginiFintech and Transformation in Financial Services: Seminar Report Onrobert juniorÎncă nu există evaluări

- MantapsDocument11 paginiMantapssuarta kasmiranÎncă nu există evaluări

- Effect of Financial Innovation On The Performance of Deposit Money Banks in NigeriaDocument11 paginiEffect of Financial Innovation On The Performance of Deposit Money Banks in NigeriaEditor IJTSRDÎncă nu există evaluări

- Session 7-1: Fintech and Financial Literacy in Viet Nam by Peter J. MorganDocument30 paginiSession 7-1: Fintech and Financial Literacy in Viet Nam by Peter J. MorganADBI Events100% (1)

- 518pm31.zahoor Ahmad ShahDocument8 pagini518pm31.zahoor Ahmad ShahPrajwal KottawarÎncă nu există evaluări

- The Block Research - A Global Look at CBDC - Aug 2020Document92 paginiThe Block Research - A Global Look at CBDC - Aug 2020Eugenio Navarro MÎncă nu există evaluări

- Ey The Winds of Change India Fintech Report 2021Document76 paginiEy The Winds of Change India Fintech Report 2021ShwetaÎncă nu există evaluări

- CIMB Clicks 27Document1 paginăCIMB Clicks 27achiro0707Încă nu există evaluări

- Git InstallationDocument10 paginiGit Installationachiro0707Încă nu există evaluări

- SOFTEC ASIA 2022 FlyerDocument4 paginiSOFTEC ASIA 2022 Flyerachiro0707Încă nu există evaluări

- Istqb Virtual Foundation Level Performance Testing Course Outline v1 00Document5 paginiIstqb Virtual Foundation Level Performance Testing Course Outline v1 00achiro0707Încă nu există evaluări

- Sunway FSSC SDN BHD: Supplier Banking Details Form For Online TransferDocument1 paginăSunway FSSC SDN BHD: Supplier Banking Details Form For Online Transferachiro0707Încă nu există evaluări

- Crypto and Law FinalDocument19 paginiCrypto and Law Finalharshvardhan dinghÎncă nu există evaluări

- Electronic Payment SystemsDocument21 paginiElectronic Payment Systemsyaswanth manchikalapudiÎncă nu există evaluări

- Jio Fibre RecieptDocument3 paginiJio Fibre RecieptMuhammad Aqeel DarÎncă nu există evaluări

- Can A Debit Card From A Different Bank Be Used at Another BankDocument5 paginiCan A Debit Card From A Different Bank Be Used at Another BankHabtamu AssefaÎncă nu există evaluări

- DCU LoanDocument2 paginiDCU Loansubhadip1390Încă nu există evaluări

- Ethics Education Package Order FormDocument1 paginăEthics Education Package Order Formlinm@kilvington.vic.edu.auÎncă nu există evaluări

- Marriage ResumeDocument2 paginiMarriage ResumeSk SharmaÎncă nu există evaluări

- Can You Send Money From Algeria To Florida - GoogDocument1 paginăCan You Send Money From Algeria To Florida - GoogJessica Hendricks GroovesÎncă nu există evaluări

- Ehrentraud & Garcia (2020) - Managing The Winds of Change - Policy Responses To FintechDocument8 paginiEhrentraud & Garcia (2020) - Managing The Winds of Change - Policy Responses To FintechJeffersonÎncă nu există evaluări

- Yahoo Mail - Booking Confirmation On IRCTC, Train - 02717, 18-Feb-2021, CC, VSKP - RJYDocument2 paginiYahoo Mail - Booking Confirmation On IRCTC, Train - 02717, 18-Feb-2021, CC, VSKP - RJYPhani KumarÎncă nu există evaluări

- DOJ Powerpoint Presentation On Hotwatch Surveillance Orders of Credit Card TransactionsDocument10 paginiDOJ Powerpoint Presentation On Hotwatch Surveillance Orders of Credit Card Transactionscsoghoian100% (1)

- Invoice WFWEF 671707Document1 paginăInvoice WFWEF 671707Brian MpafeÎncă nu există evaluări

- Geran BSN - Digitalized SystemDocument290 paginiGeran BSN - Digitalized SystemSyahira AzmiÎncă nu există evaluări

- Cyber CashDocument13 paginiCyber CashDivya PorwalÎncă nu există evaluări

- Pocket Rocket PayTmDocument16 paginiPocket Rocket PayTmNikhil Negi100% (1)

- MSBsDocument538 paginiMSBsEvangeline VillegasÎncă nu există evaluări

- Standar mt103Document82 paginiStandar mt103Nestor Julio Arias Moná100% (1)

- Magazine ContentDocument5 paginiMagazine ContentGail PerezÎncă nu există evaluări

- F FDYpk RZGK MMVX 4 WDocument4 paginiF FDYpk RZGK MMVX 4 WRaghu Varma PorankiÎncă nu există evaluări

- E Business ModelsDocument46 paginiE Business Modelsskumar4787Încă nu există evaluări

- Account StatementDocument12 paginiAccount StatementRadhi PatelÎncă nu există evaluări

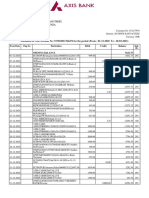

- Axis Bank Latest StatementDocument4 paginiAxis Bank Latest StatementPrashant KumarÎncă nu există evaluări

- LLR Subscription Form 2018Document1 paginăLLR Subscription Form 2018jagshish100% (1)

- Colombia PSE Case Study Long ENG Jan 2015Document46 paginiColombia PSE Case Study Long ENG Jan 2015SaurabhRoyÎncă nu există evaluări

- Statement of AccountDocument5 paginiStatement of Accountmutaia pandian100% (1)

- Schedule of Charges - MTB Credit Cards - Effective From 1st Jul 2023Document4 paginiSchedule of Charges - MTB Credit Cards - Effective From 1st Jul 2023Dhononjoy PaulÎncă nu există evaluări

- Acct Statement - XX7579 - 03112023Document19 paginiAcct Statement - XX7579 - 03112023Ashish Singh bhandari100% (1)