S-ar putea să vă placă și

- Do Banks Provision For Bad Loans in Good Times? Empirical Evidence and Policy ImplicationsDocument34 paginiDo Banks Provision For Bad Loans in Good Times? Empirical Evidence and Policy ImplicationsabhinavatripathiÎncă nu există evaluări

- BASELDocument8 paginiBASELrohit_kumraÎncă nu există evaluări

- Capital Regulation and Banks' Financial Decisions: Haibin ZhuDocument47 paginiCapital Regulation and Banks' Financial Decisions: Haibin ZhuprernagadiaÎncă nu există evaluări

- The Non-Performing LoansDocument34 paginiThe Non-Performing Loanshannory100% (1)

- Adrian Et Al - 2013Document56 paginiAdrian Et Al - 2013Gülşah SütçüÎncă nu există evaluări

- The Long-Term Economic Impact of Higher Capital LevelsDocument9 paginiThe Long-Term Economic Impact of Higher Capital LevelsRonald MirallesÎncă nu există evaluări

- Ecb wp2181 enDocument27 paginiEcb wp2181 enaldhibahÎncă nu există evaluări

- Why Do Banks Securitize Assets?: Alfredo Martín-Oliver (Banco de España) Jesús Saurina (Banco de España)Document33 paginiWhy Do Banks Securitize Assets?: Alfredo Martín-Oliver (Banco de España) Jesús Saurina (Banco de España)Sorah YoriÎncă nu există evaluări

- Basel - 1,2,3Document40 paginiBasel - 1,2,3Golam RamijÎncă nu există evaluări

- The Non-Performing Loans: Some Bank-Level EvidencesDocument34 paginiThe Non-Performing Loans: Some Bank-Level EvidencesJORKOS1Încă nu există evaluări

- PaperJBF ExpectedSignsDocument23 paginiPaperJBF ExpectedSignsPhạm Hà AnÎncă nu există evaluări

- Liquidity Assessment and The Use of Liquidity Ratio As Defined in The Basel III Accords To Identify Bank DistressDocument36 paginiLiquidity Assessment and The Use of Liquidity Ratio As Defined in The Basel III Accords To Identify Bank DistressmikeokayÎncă nu există evaluări

- Reserves, Liquidity and Money: An Assessment of Balance Sheet PoliciesDocument54 paginiReserves, Liquidity and Money: An Assessment of Balance Sheet PoliciesGeralyn MiralÎncă nu există evaluări

- Resolving Too Big To FailDocument28 paginiResolving Too Big To Failsakins9429Încă nu există evaluări

- Adrian-Colla-Shin - Which Financial Frictions (Parsing The Evidence From The Financial Crisis of 2007-9)Document54 paginiAdrian-Colla-Shin - Which Financial Frictions (Parsing The Evidence From The Financial Crisis of 2007-9)Chi-Wa CWÎncă nu există evaluări

- Afa2018 1908Document33 paginiAfa2018 1908tamÎncă nu există evaluări

- Bologna 2018 Banks Maturity TransformationDocument36 paginiBologna 2018 Banks Maturity TransformationRashid AnwarÎncă nu există evaluări

- Policy Brief AssessmentDocument5 paginiPolicy Brief AssessmentAnish PadalkarÎncă nu există evaluări

- Accenture The New Importance of Risk Weighted Assets Across Europe PDFDocument24 paginiAccenture The New Importance of Risk Weighted Assets Across Europe PDFvinaygupta18Încă nu există evaluări

- 1# Managing Bank Liquidity Risk How Deposit-Loan Synergies Vary With Market ConditionsDocument35 pagini1# Managing Bank Liquidity Risk How Deposit-Loan Synergies Vary With Market ConditionsYING DINGÎncă nu există evaluări

- Bank Asset Structure, Real-Estate Lending, and Risk-Taking: Matej Bla Sko, Joseph F. Sinkey JRDocument29 paginiBank Asset Structure, Real-Estate Lending, and Risk-Taking: Matej Bla Sko, Joseph F. Sinkey JRCiornei OanaÎncă nu există evaluări

- Journal of Economics and Business: Caroline RouletDocument21 paginiJournal of Economics and Business: Caroline RouletNahyunjungÎncă nu există evaluări

- Can Be Use Ful SmeDocument30 paginiCan Be Use Ful SmemayurhoreÎncă nu există evaluări

- Dividend Policy and Capital Retention: A Systemic "First Response"Document16 paginiDividend Policy and Capital Retention: A Systemic "First Response"Phượng ViÎncă nu există evaluări

- Capital Regulation Challenges (1) - Banking LawsDocument6 paginiCapital Regulation Challenges (1) - Banking Lawshemstone mgendyÎncă nu există evaluări

- Journalof: Banking & FinanceDocument21 paginiJournalof: Banking & FinanceEvelin BudiartiÎncă nu există evaluări

- How Has Bank Supervision Performed and How Might It Be Improved?Document47 paginiHow Has Bank Supervision Performed and How Might It Be Improved?Peter RadkovÎncă nu există evaluări

- Monetary Policy and The Risk-Taking Channel: CompleterDocument11 paginiMonetary Policy and The Risk-Taking Channel: CompleterMaría GómezÎncă nu există evaluări

- NPL Accounting BOEDocument80 paginiNPL Accounting BOETom, Dick and HarryÎncă nu există evaluări

- Godlewski Are Bank Loans Still Special Especially During A CrisisDocument33 paginiGodlewski Are Bank Loans Still Special Especially During A CrisisPhương Anh TrầnÎncă nu există evaluări

- Journal of Macroeconomics: Sebastiaan Pool, Leo de Haan, Jan P.A.M. JacobsDocument13 paginiJournal of Macroeconomics: Sebastiaan Pool, Leo de Haan, Jan P.A.M. JacobsabhinavatripathiÎncă nu există evaluări

- Journal of Accounting and Economics: Paul J. Beck, Ganapathi S. NarayanamoorthyDocument24 paginiJournal of Accounting and Economics: Paul J. Beck, Ganapathi S. NarayanamoorthyabhinavatripathiÎncă nu există evaluări

- Impact of QE - BoEDocument11 paginiImpact of QE - BoENikolay KolarovÎncă nu există evaluări

- Discussion Paper Series: Optimal Bank CapitalDocument57 paginiDiscussion Paper Series: Optimal Bank CapitalOleg BotnaruÎncă nu există evaluări

- Evidence On The Response of Us Banks To Changes in Capital RequirementsDocument32 paginiEvidence On The Response of Us Banks To Changes in Capital RequirementskanonchowdhuryÎncă nu există evaluări

- Low Rates and Bank Stability: The Risk of A Tipping PointDocument4 paginiLow Rates and Bank Stability: The Risk of A Tipping Pointbob.winarskiÎncă nu există evaluări

- Finance and Economics Discussion SeriesDocument38 paginiFinance and Economics Discussion SeriesChong PengÎncă nu există evaluări

- 012 New Loan Provisioning Standards and Procyclicality, Borio 2018Document6 pagini012 New Loan Provisioning Standards and Procyclicality, Borio 2018Juan José LopezÎncă nu există evaluări

- Evidence of How Banks Respond To Central Bank SupervisionDocument36 paginiEvidence of How Banks Respond To Central Bank SupervisionRichard SaitoÎncă nu există evaluări

- Long Term Bank Lending and The TransferDocument55 paginiLong Term Bank Lending and The TransferFerdee FerdÎncă nu există evaluări

- Spillovers From Systemic Bank DefaultsDocument22 paginiSpillovers From Systemic Bank DefaultsAdolfÎncă nu există evaluări

- Dallas FedDocument4 paginiDallas FedAdminAliÎncă nu există evaluări

- Capital Buffer, Credit Risk and Liquidity Behaviour: Evidence For GCC Banks Saibal GhoshDocument25 paginiCapital Buffer, Credit Risk and Liquidity Behaviour: Evidence For GCC Banks Saibal GhoshMarcos Romero PerezÎncă nu există evaluări

- Active Risk Management and Banking StabilityDocument44 paginiActive Risk Management and Banking Stabilityadib tanjungÎncă nu există evaluări

- An Essay On Bank Regulation and Basel IIDocument15 paginiAn Essay On Bank Regulation and Basel IIBhanumati BhunjunÎncă nu există evaluări

- Research 3Document40 paginiResearch 3ms.AhmedÎncă nu există evaluări

- Shadow Banking System ThesisDocument6 paginiShadow Banking System Thesispak0t0dynyj3100% (2)

- NG, J., & Roychowdhury, S. (2014) .Document46 paginiNG, J., & Roychowdhury, S. (2014) .Vita NataliaÎncă nu există evaluări

- MisunderstandingDocument11 paginiMisunderstandingImranÎncă nu există evaluări

- What Happened: Financial Factors in The Great Recession: Mark Gertler and Simon GilchristDocument28 paginiWhat Happened: Financial Factors in The Great Recession: Mark Gertler and Simon GilchristplxnospamÎncă nu există evaluări

- Monetary Policy TransmissionDocument8 paginiMonetary Policy TransmissionPeter WailesÎncă nu există evaluări

- Cross-Country Determinants of Bank Income Smoothing by Managing Loan-Loss ProvisionsDocument12 paginiCross-Country Determinants of Bank Income Smoothing by Managing Loan-Loss ProvisionsabhinavatripathiÎncă nu există evaluări

- Abiad The QualityDocument13 paginiAbiad The QualityFauzan AzimaÎncă nu există evaluări

- Financial Distortions in China: A General Equilibrium ApproachDocument31 paginiFinancial Distortions in China: A General Equilibrium ApproachTBP_Think_TankÎncă nu există evaluări

- Congressional Research Service Capstone Research ReportDocument31 paginiCongressional Research Service Capstone Research ReportFrank AnthonyÎncă nu există evaluări

- Accepted Manuscript: Research in International Business and FinanceDocument34 paginiAccepted Manuscript: Research in International Business and FinanceCorolla SedanÎncă nu există evaluări

- Credit Flows To Businesses During The Great Recession: Conomic OmmentaryDocument6 paginiCredit Flows To Businesses During The Great Recession: Conomic Ommentarykharal785Încă nu există evaluări

- Understanding The Price of New Lending To HouseholdsDocument11 paginiUnderstanding The Price of New Lending To HouseholdshellowodÎncă nu există evaluări

- Ecb wp2589 2fda18e5ca enDocument53 paginiEcb wp2589 2fda18e5ca enDemian MacedoÎncă nu există evaluări

- EIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataDe la EverandEIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataÎncă nu există evaluări

- Beta Anomaly An Ex-Ante Tail RiskDocument104 paginiBeta Anomaly An Ex-Ante Tail RiskDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Claudia Jones Nuclear TestingDocument25 paginiClaudia Jones Nuclear TestingDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Why The Euro Will Rival The Dollar PDFDocument25 paginiWhy The Euro Will Rival The Dollar PDFDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Continuity Change State of Process of Task ofDocument1 paginăContinuity Change State of Process of Task ofDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Conference Group For Central European History of The American Historical AssociationDocument9 paginiConference Group For Central European History of The American Historical AssociationDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Theophilus Capital Against: Fisk Labor1Document9 paginiTheophilus Capital Against: Fisk Labor1Daniel Lee Eisenberg Jacobs100% (1)

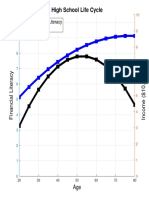

- High School Life Cycle: Financial Literacy IncomeDocument1 paginăHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Individualization of Robo-AdviceDocument8 paginiIndividualization of Robo-AdviceDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Karl Kautsky Republic and Social Democra PDFDocument4 paginiKarl Kautsky Republic and Social Democra PDFDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Borel Sets PDFDocument181 paginiBorel Sets PDFDaniel Lee Eisenberg Jacobs100% (1)

- Cover FERCDocument1 paginăCover FERCDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- 1st International: Djacobs November 2020Document5 pagini1st International: Djacobs November 2020Daniel Lee Eisenberg JacobsÎncă nu există evaluări

- Gpebook PDFDocument332 paginiGpebook PDFDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- The Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDocument8 paginiThe Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Necessary and Sufficient Conditions For Dynamic OptimizationDocument18 paginiNecessary and Sufficient Conditions For Dynamic OptimizationDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Teach-In: Government of The People, by The People, For The PeopleDocument24 paginiTeach-In: Government of The People, by The People, For The PeopleDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Simple BeamerDocument25 paginiSimple BeamerDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Corporate Finance 2 SyllabusDocument11 paginiCorporate Finance 2 SyllabusMai NguyenÎncă nu există evaluări

- Mckinsey On Payments: October 2015 Volume 8, Number 22Document8 paginiMckinsey On Payments: October 2015 Volume 8, Number 22santosh hariharanÎncă nu există evaluări

- 5 BFU 07406 Assessment of Credit ApplicationsDocument109 pagini5 BFU 07406 Assessment of Credit ApplicationsDeogratias MsigalaÎncă nu există evaluări

- What Is Modaraba: I) General DefinitionDocument6 paginiWhat Is Modaraba: I) General Definitionahsan saeedÎncă nu există evaluări

- Internship Report of Muminul Hoque Fahim PDFDocument58 paginiInternship Report of Muminul Hoque Fahim PDFMahmudul HasanÎncă nu există evaluări

- Research Project AssignmentDocument27 paginiResearch Project AssignmentSam CleonÎncă nu există evaluări

- Mod3 - MBO-6 Credit Delivery and Legal Aspects With NumericalsDocument21 paginiMod3 - MBO-6 Credit Delivery and Legal Aspects With NumericalsakashvagadiyaÎncă nu există evaluări

- RBI Directions On Foreign Banks and Acquisition and Amalgamation of BanksDocument8 paginiRBI Directions On Foreign Banks and Acquisition and Amalgamation of Banksvijayadarshini vÎncă nu există evaluări

- Internal Marketing Journal PDFDocument26 paginiInternal Marketing Journal PDFIndiani Putri Datik100% (1)

- 5332740317Document301 pagini5332740317sharkl123Încă nu există evaluări

- CTBC Form & Consent FormDocument2 paginiCTBC Form & Consent FormJhon Micheal AlicandoÎncă nu există evaluări

- ProposalDocument10 paginiProposalSagar KarkiÎncă nu există evaluări

- Reagen PapersDocument118 paginiReagen PapersFilip DanielÎncă nu există evaluări

- Post Office Saving Bank Account Project-01Document13 paginiPost Office Saving Bank Account Project-01vivek jadhavÎncă nu există evaluări

- Cheviot ColtdDocument41 paginiCheviot ColtdSubscriptionÎncă nu există evaluări

- 12 Chapter 9 - Risk Management in Banks NBFCsDocument4 pagini12 Chapter 9 - Risk Management in Banks NBFCsgarima_kukreja_dceÎncă nu există evaluări

- JM Financial Home - CRISIL - CleanedDocument8 paginiJM Financial Home - CRISIL - CleanedSrinivasÎncă nu există evaluări

- Statement 115377 Oct-2022Document8 paginiStatement 115377 Oct-2022Mary MacLellanÎncă nu există evaluări

- Money and CreditDocument14 paginiMoney and CreditRajau RajputanaÎncă nu există evaluări

- Federal Deposit Insurance Corporation, Etc. v. Leonard Caporale, Etc., 931 F.2d 1, 1st Cir. (1991)Document4 paginiFederal Deposit Insurance Corporation, Etc. v. Leonard Caporale, Etc., 931 F.2d 1, 1st Cir. (1991)Scribd Government DocsÎncă nu există evaluări

- Health Insurance Industry in India: Prospects and ChallengesDocument13 paginiHealth Insurance Industry in India: Prospects and ChallengesGaurav NarangÎncă nu există evaluări

- Capital Market - : Difference Between Primary and Secondary MarketDocument7 paginiCapital Market - : Difference Between Primary and Secondary MarketJanellaÎncă nu există evaluări

- 15-IFRS 15 - SummaryDocument6 pagini15-IFRS 15 - SummaryhusseinÎncă nu există evaluări

- Banc One Case Study PDF FreeDocument10 paginiBanc One Case Study PDF FreeFathima KamalÎncă nu există evaluări

- RBI - NPA CircularDocument96 paginiRBI - NPA CircularArundev SusarlaÎncă nu există evaluări

- Administrative HoldDocument2 paginiAdministrative Holdunoguru93% (15)

- StoneDocument21 paginiStoneandre.torresÎncă nu există evaluări

- Josoft Technologies Pvt. Limited: Application Form (For Individual)Document1 paginăJosoft Technologies Pvt. Limited: Application Form (For Individual)tharunÎncă nu există evaluări

- BFM RecollectedDocument8 paginiBFM RecollectedGURPREET KAURÎncă nu există evaluări

- Aud ProbDocument9 paginiAud ProbKulet AkoÎncă nu există evaluări