S-ar putea să vă placă și

- Consumer Protection in India: Some Reflections on History and ConceptsDocument40 paginiConsumer Protection in India: Some Reflections on History and ConceptsPatel JatinÎncă nu există evaluări

- Provisions in IPC Against Selling and Manufacturing of Counterfeit Products - Brands & Fakes - Part 92Document7 paginiProvisions in IPC Against Selling and Manufacturing of Counterfeit Products - Brands & Fakes - Part 92manoj-kr-dorai-9476Încă nu există evaluări

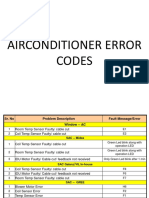

- Ac Error Codes & Trouble ShootingDocument14 paginiAc Error Codes & Trouble ShootingPrantik Padhy60% (5)

- Top 10 Sugar Companies in India - Learning CenterDocument4 paginiTop 10 Sugar Companies in India - Learning Centermanoj-kr-dorai-9476Încă nu există evaluări

- Belting FormulasDocument1 paginăBelting Formulasmanoj-kr-dorai-9476Încă nu există evaluări

- RTI - District Bokaro, Government of JharkhandDocument11 paginiRTI - District Bokaro, Government of Jharkhandmanoj-kr-dorai-9476Încă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Guide Book FPO SchemesDocument60 paginiGuide Book FPO Schemessatyanweshi truthseekerÎncă nu există evaluări

- Deposit OperationsDocument17 paginiDeposit OperationsArmela HasmucaÎncă nu există evaluări

- Study On Impact of Banking Technology On Indian EconomyDocument11 paginiStudy On Impact of Banking Technology On Indian EconomyArpita ChoudharyÎncă nu există evaluări

- Report MSC ProjectDocument6 paginiReport MSC ProjectLola SamÎncă nu există evaluări

- CASHDocument28 paginiCASHJereme PascuaÎncă nu există evaluări

- UntitledDocument121 paginiUntitlednikhilÎncă nu există evaluări

- Reaching The Last Mile: Presented By: NPCI OfficialsDocument17 paginiReaching The Last Mile: Presented By: NPCI OfficialsMithunÎncă nu există evaluări

- RBL Credit CardDocument1 paginăRBL Credit CardDipra DasÎncă nu există evaluări

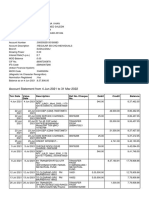

- Account Statement From 4 Jun 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument3 paginiAccount Statement From 4 Jun 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSaleem KhanÎncă nu există evaluări

- Do Terra AugustDocument1 paginăDo Terra AugustRoxana Costache MarinescuÎncă nu există evaluări

- Guidelines For Filling PAN Change Request Application - Reprint of PAN CardDocument3 paginiGuidelines For Filling PAN Change Request Application - Reprint of PAN CardMoumita BanikÎncă nu există evaluări

- Chapter 5 NewDocument44 paginiChapter 5 NewMuhammad Khairul Rafiq Bin Md RafieeÎncă nu există evaluări

- FMI - History of Citibank NA UppedDocument3 paginiFMI - History of Citibank NA UppedSidrat TalukderÎncă nu există evaluări

- Sutton Bank Cardholder Agreement v1.4Document21 paginiSutton Bank Cardholder Agreement v1.4Gina VictoriaÎncă nu există evaluări

- Wa0025Document8 paginiWa0025SachinZambareÎncă nu există evaluări

- Platinum Shopgain SupercardDocument15 paginiPlatinum Shopgain SupercardBas LathaÎncă nu există evaluări

- Rural Financial Institutions: The Case Study of ACLEDA BankDocument15 paginiRural Financial Institutions: The Case Study of ACLEDA BankSophie LamÎncă nu există evaluări

- Economic Injury Disaster Loan UpdateDocument2 paginiEconomic Injury Disaster Loan UpdateJian GabatÎncă nu există evaluări

- RBI keeps repo rate unchanged and other banking newsDocument51 paginiRBI keeps repo rate unchanged and other banking newsunikxocizmÎncă nu există evaluări

- CRM Practices at Icici BankDocument11 paginiCRM Practices at Icici BankJesse Dunn33% (3)

- Moneylending Interest Rates & Types of Friendly LoansDocument3 paginiMoneylending Interest Rates & Types of Friendly LoansKajendra BalanÎncă nu există evaluări

- 4 Genius Mind Notice - Final (I)Document5 pagini4 Genius Mind Notice - Final (I)tanmaya_purohitÎncă nu există evaluări

- Total Units 22: Federal Cooperative College Kaduna P.M.B 2425 KadunaDocument1 paginăTotal Units 22: Federal Cooperative College Kaduna P.M.B 2425 KadunaTope AyeniÎncă nu există evaluări

- CE GSE Meeting - Cash Position and Cash Forecast ReportsDocument12 paginiCE GSE Meeting - Cash Position and Cash Forecast ReportsELOUSOUANIÎncă nu există evaluări

- Andrew Seger Motion For Leave To Amend Complaint Exhibit BDocument85 paginiAndrew Seger Motion For Leave To Amend Complaint Exhibit Bamber stegall100% (1)

- Fee Structure Sentinel Kabitaka 2022Document2 paginiFee Structure Sentinel Kabitaka 2022TaongaÎncă nu există evaluări

- Bangladesh BankDocument5 paginiBangladesh BankSubatomic ParticleÎncă nu există evaluări

- Ann Hoffman Owner of Hoffman Industries Is Negotiating With TheDocument2 paginiAnn Hoffman Owner of Hoffman Industries Is Negotiating With TheAmit PandeyÎncă nu există evaluări

- Laws on banking and finance intermediariesDocument4 paginiLaws on banking and finance intermediariesMary.Rose RosalesÎncă nu există evaluări

- JD v3.1 Tirunelveli Loan Agency 2022 23Document65 paginiJD v3.1 Tirunelveli Loan Agency 2022 23RajaGopalÎncă nu există evaluări