S-ar putea să vă placă și

- Bank StatementDocument4 paginiBank StatementKenny Nam50% (2)

- Ruling - CIR V FilinvestDocument1 paginăRuling - CIR V FilinvestryanmeinÎncă nu există evaluări

- Accepted Fees 1200.00 Amount in Words: One Thousand Two Hundred OnlyDocument1 paginăAccepted Fees 1200.00 Amount in Words: One Thousand Two Hundred OnlySunil B. SawantÎncă nu există evaluări

- RTGS FormDocument2 paginiRTGS FormravilotusÎncă nu există evaluări

- CIR Vs Central Luzon Drug Corp.Document9 paginiCIR Vs Central Luzon Drug Corp.Jeff GomezÎncă nu există evaluări

- Tax CasesDocument95 paginiTax CasesCyrus Santos MendozaÎncă nu există evaluări

- CIR vs. CLDCDocument18 paginiCIR vs. CLDCLexa L. DotyalÎncă nu există evaluări

- CIR vs. Central Luzon Drug Corp., G.R. No. 159647, April 15, 2005Document10 paginiCIR vs. Central Luzon Drug Corp., G.R. No. 159647, April 15, 2005BernadetteÎncă nu există evaluări

- Comm vs. Central Luzon 456 SCRA 414Document21 paginiComm vs. Central Luzon 456 SCRA 414Jacinto Jr Jamero100% (1)

- CuevaDocument3 paginiCuevaPhilippe CamposanoÎncă nu există evaluări

- Sbu Tax MT Samaniego Emil (4S)Document5 paginiSbu Tax MT Samaniego Emil (4S)Naked PolitixxxÎncă nu există evaluări

- CIR Vs Central Luzon Drug CorpDocument11 paginiCIR Vs Central Luzon Drug CorpGrace DelinÎncă nu există evaluări

- Tax Assessments Burden of ProofDocument3 paginiTax Assessments Burden of ProofblessaraynesÎncă nu există evaluări

- Remedies Procedure Lecture 3Document11 paginiRemedies Procedure Lecture 3Susannie AcainÎncă nu există evaluări

- Commissioner of Internal Revenue vs. Mirant Pagbilao CorporationDocument23 paginiCommissioner of Internal Revenue vs. Mirant Pagbilao CorporationToni LorescaÎncă nu există evaluări

- Fort Bonifacio Development Corporation vs. Commissioner of Internal RevenueDocument28 paginiFort Bonifacio Development Corporation vs. Commissioner of Internal RevenueAriel AbisÎncă nu există evaluări

- Commissioner of Internal Revenue vs. Central Luzon Drug Corp.Document42 paginiCommissioner of Internal Revenue vs. Central Luzon Drug Corp.Daryll AsuncionÎncă nu există evaluări

- CIR vs. AyalaDocument11 paginiCIR vs. AyalaEvan NervezaÎncă nu există evaluări

- Tax Refunds Setting Matters StraightDocument3 paginiTax Refunds Setting Matters StraightSiobhan RobinÎncă nu există evaluări

- Commissioner of Internal Revenue Vs Central Luzon Drug Corporation 456 SCRA 413Document13 paginiCommissioner of Internal Revenue Vs Central Luzon Drug Corporation 456 SCRA 413Epictitus StoicÎncă nu există evaluări

- CIR vs. Central Luzon Drug Corp., G.R. No. 159647, April 15, 2005Document17 paginiCIR vs. Central Luzon Drug Corp., G.R. No. 159647, April 15, 2005Machida AbrahamÎncă nu există evaluări

- Commissioner of Internal Revenue Vs Central Luzon Drug Corporation GR No 159647Document36 paginiCommissioner of Internal Revenue Vs Central Luzon Drug Corporation GR No 159647Tamara Bianca Chingcuangco Ernacio-TabiosÎncă nu există evaluări

- Tax Remedies - Part IDocument11 paginiTax Remedies - Part IRamon AngelesÎncă nu există evaluări

- 9 CIR V Ayala Securities Corp. (1980)Document7 pagini9 CIR V Ayala Securities Corp. (1980)KristineSherikaChyÎncă nu există evaluări

- CIR Vs Ayala Securities CorpDocument7 paginiCIR Vs Ayala Securities Corplen_dy010487Încă nu există evaluări

- Tax Vat Week4Document73 paginiTax Vat Week4Neil FrangilimanÎncă nu există evaluări

- Adv. Mallya Oscar, F.k.... Tax LawDocument7 paginiAdv. Mallya Oscar, F.k.... Tax LawOscar MallyaÎncă nu există evaluări

- CIR Vs Central LuzonDocument12 paginiCIR Vs Central LuzonSahara RiveraÎncă nu există evaluări

- Fort Bonifacio Devt Corp V CIRDocument3 paginiFort Bonifacio Devt Corp V CIRBettina Rayos del SolÎncă nu există evaluări

- PARAS, DENNIS JAY A. (Cases 80 - 84)Document5 paginiPARAS, DENNIS JAY A. (Cases 80 - 84)Dennis Jay ParasÎncă nu există evaluări

- Falsity of False Tax ReturnsDocument6 paginiFalsity of False Tax ReturnsShaike Harvin DaquioagÎncă nu există evaluări

- Deduction From The Gross Income or Gross Sale of The Establishment Concerned. A Tax Credit Is Used by ADocument12 paginiDeduction From The Gross Income or Gross Sale of The Establishment Concerned. A Tax Credit Is Used by AAnonymous D0IyLfirVÎncă nu există evaluări

- G.R. No. 159647Document13 paginiG.R. No. 159647Eunice KanapiÎncă nu există evaluări

- Philippine Guaranty Co Vs CIRDocument4 paginiPhilippine Guaranty Co Vs CIRJarvin David ResusÎncă nu există evaluări

- Coca-Cola Bottlers v. Cir DigestDocument4 paginiCoca-Cola Bottlers v. Cir DigestkathrynmaydevezaÎncă nu există evaluări

- Tax Rev Notes RemediesDocument179 paginiTax Rev Notes RemediesJake MacTavishÎncă nu există evaluări

- Filipinas Synthetic Fiber Corporation V CADocument2 paginiFilipinas Synthetic Fiber Corporation V CACedrick TanÎncă nu există evaluări

- LG-Electronics-vs.-CIR-digestDocument21 paginiLG-Electronics-vs.-CIR-digestDarrel John SombilonÎncă nu există evaluări

- Third Division: Republic of Philippines Court of Tax Appeals QuezonDocument8 paginiThird Division: Republic of Philippines Court of Tax Appeals Quezonنيسريو جينوÎncă nu există evaluări

- Tax 2Document79 paginiTax 2Karen Mae ServanÎncă nu există evaluări

- 2018 Bar Tax Updates (Tax Ii)Document174 pagini2018 Bar Tax Updates (Tax Ii)Jeffrey Dela PazÎncă nu există evaluări

- 5 Philippine Guaranty Co Vs CIR, GGR L-22074, Sept 6, 1965Document5 pagini5 Philippine Guaranty Co Vs CIR, GGR L-22074, Sept 6, 1965Seok Gyeong KangÎncă nu există evaluări

- 20.CIR Vs Central Luzon DrugDocument12 pagini20.CIR Vs Central Luzon DrugClyde KitongÎncă nu există evaluări

- ASSESSMENT OF INTERNAL REVENUE TAXES 2024 InitialDocument31 paginiASSESSMENT OF INTERNAL REVENUE TAXES 2024 InitialRey Jay BICARÎncă nu există evaluări

- Tax CasesDocument43 paginiTax CasesArlando G. ArlandoÎncă nu există evaluări

- Cir Vs SeagateDocument5 paginiCir Vs SeagateRenz Amon0% (1)

- GR No 159647 PDFDocument12 paginiGR No 159647 PDFShameee shameeeÎncă nu există evaluări

- Taxation Law CasesDocument28 paginiTaxation Law CasesLou Corina LacambraÎncă nu există evaluări

- Case No. 49 G.R. No. L-13325 April 20, 1961 Santiago Gancayco, Petitioner, vs. The Collector of INTERNAL REVENUE, RespondentDocument5 paginiCase No. 49 G.R. No. L-13325 April 20, 1961 Santiago Gancayco, Petitioner, vs. The Collector of INTERNAL REVENUE, RespondentLeeÎncă nu există evaluări

- For RecitDocument27 paginiFor RecitAlyk CalionÎncă nu există evaluări

- ING Bank N.V. vs. CIR, 763 SCRA 359 (2015)Document2 paginiING Bank N.V. vs. CIR, 763 SCRA 359 (2015)Anonymous MikI28PkJc100% (2)

- People vs. Sandiganbayan, 467 SCRA 137, August 16, 2005Document28 paginiPeople vs. Sandiganbayan, 467 SCRA 137, August 16, 2005j0d3100% (1)

- Rizal Commercial Banking Corporation V CIR (September 7 2011)Document63 paginiRizal Commercial Banking Corporation V CIR (September 7 2011)ybunÎncă nu există evaluări

- Retroactive Application If The Revocation, Modification or Reversal Will Be Prejudicial To The Taxpayers, Except in The Following CasesDocument4 paginiRetroactive Application If The Revocation, Modification or Reversal Will Be Prejudicial To The Taxpayers, Except in The Following CasesIrish AnnÎncă nu există evaluări

- CIR V PDIDocument2 paginiCIR V PDIRachel LeachonÎncă nu există evaluări

- CIR vs. Procter and GambleDocument3 paginiCIR vs. Procter and GambleRobÎncă nu există evaluări

- Part G 2a - CIR Vs PascorDocument3 paginiPart G 2a - CIR Vs PascorCyruz TuppalÎncă nu există evaluări

- Commissioner of Internal Revenue vs. Benguet Corporation 463 SCRA 28, July 08, 2005Document9 paginiCommissioner of Internal Revenue vs. Benguet Corporation 463 SCRA 28, July 08, 2005Francise Mae Montilla MordenoÎncă nu există evaluări

- Commissioner of Internal Revenue vs. Court of Appeals 301 SCRA 152Document43 paginiCommissioner of Internal Revenue vs. Court of Appeals 301 SCRA 152fritz frances danielleÎncă nu există evaluări

- CIR vs. Algue, Inc. GRN L-28896 February 17, 1988 J. CruzDocument2 paginiCIR vs. Algue, Inc. GRN L-28896 February 17, 1988 J. CruzChelle OngÎncă nu există evaluări

- GST Interest Liability U/Sec - 50 of CGST Act 2017Document6 paginiGST Interest Liability U/Sec - 50 of CGST Act 2017Saurabh JunejaÎncă nu există evaluări

- Facts:: PILMICO-MAURI FOODS CORP. v. CIR,, GR No. 175651, 2016-09-14Document9 paginiFacts:: PILMICO-MAURI FOODS CORP. v. CIR,, GR No. 175651, 2016-09-14Andrew M. AcederaÎncă nu există evaluări

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeDe la Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeEvaluare: 1 din 5 stele1/5 (1)

- 001 Us V. Univis Lens Co. (Villavicencio)Document49 pagini001 Us V. Univis Lens Co. (Villavicencio)Telle MarieÎncă nu există evaluări

- Q: Corp A & Corp B Both Foreign Corporations Not Doing Business in The Philippines, Filed A Complaint ForDocument1 paginăQ: Corp A & Corp B Both Foreign Corporations Not Doing Business in The Philippines, Filed A Complaint ForTelle MarieÎncă nu există evaluări

- 095 Tanay Recreation v. FaustoDocument1 pagină095 Tanay Recreation v. FaustoTelle MarieÎncă nu există evaluări

- 25.2 MR of TOLENTINO V Secretary of FinanceDocument2 pagini25.2 MR of TOLENTINO V Secretary of FinanceTelle MarieÎncă nu există evaluări

- 001 West Coast Life Insurance Co. vs. Hurd (See)Document51 pagini001 West Coast Life Insurance Co. vs. Hurd (See)Telle MarieÎncă nu există evaluări

- PATENT NOTES UpdatedDocument10 paginiPATENT NOTES UpdatedTelle MarieÎncă nu există evaluări

- Labor Law Review Guide Labor 1Document4 paginiLabor Law Review Guide Labor 1Telle MarieÎncă nu există evaluări

- 33 Northwest Air V Sps. HeshanDocument3 pagini33 Northwest Air V Sps. HeshanTelle MarieÎncă nu există evaluări

- Concept of Agrarian Reform (Complete)Document8 paginiConcept of Agrarian Reform (Complete)Telle MarieÎncă nu există evaluări

- 004 RAYOS China Banking Corp V CADocument3 pagini004 RAYOS China Banking Corp V CATelle MarieÎncă nu există evaluări

- Splash Corporation Background: Early BeginningsDocument9 paginiSplash Corporation Background: Early BeginningsTelle MarieÎncă nu există evaluări

- Excise, DST Syllabi 17-18 Train LawDocument19 paginiExcise, DST Syllabi 17-18 Train LawTelle MarieÎncă nu există evaluări

- Batch 1 AdminDocument42 paginiBatch 1 AdminTelle MarieÎncă nu există evaluări

- DBP Pool of Accredited Insurance Companies v. Radio Mindanao Network, IncDocument1 paginăDBP Pool of Accredited Insurance Companies v. Radio Mindanao Network, IncTelle MarieÎncă nu există evaluări

- Occidental Mindoro National College v. MacaraegDocument1 paginăOccidental Mindoro National College v. MacaraegTelle MarieÎncă nu există evaluări

- 013 Short v. U.S.A. (United States v. Iran) (Cristelle)Document2 pagini013 Short v. U.S.A. (United States v. Iran) (Cristelle)Telle MarieÎncă nu există evaluări

- 34 Emilio V Rapal (SUNGCAD)Document2 pagini34 Emilio V Rapal (SUNGCAD)Telle MarieÎncă nu există evaluări

- 013 TOLENTINO DISINI V SANDIGANBAYANDocument3 pagini013 TOLENTINO DISINI V SANDIGANBAYANTelle MarieÎncă nu există evaluări

- 004 Colegio de San Juan de Letran v. Assoc.Document3 pagini004 Colegio de San Juan de Letran v. Assoc.Telle MarieÎncă nu există evaluări

- Zalamea v. de GuzmanDocument3 paginiZalamea v. de GuzmanTelle MarieÎncă nu există evaluări

- Shangrila V. CA ProceduralDocument2 paginiShangrila V. CA ProceduralTelle MarieÎncă nu există evaluări

- 012 Lacson-Magallanes Co., Inc. v. Pano (OLAZO) (DEEMED READ)Document3 pagini012 Lacson-Magallanes Co., Inc. v. Pano (OLAZO) (DEEMED READ)Telle MarieÎncă nu există evaluări

- 001 Joseph Vs - BautistacxDocument2 pagini001 Joseph Vs - BautistacxTelle MarieÎncă nu există evaluări

- (Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountDocument1 pagină(Original For Recipient) : Sl. No Description Unit Price Discount Qty Net Amount Tax Rate Tax Type Tax Amount Total AmountPriya MadanaÎncă nu există evaluări

- REQUERIMIENTODocument110 paginiREQUERIMIENTOJulian Leonardo Mahecha SuescunÎncă nu există evaluări

- Definition of TaxDocument3 paginiDefinition of TaxAbdullah Al Asem0% (1)

- Returning Student Registration Letter 2014 29112013Document3 paginiReturning Student Registration Letter 2014 29112013Joshua IrwinÎncă nu există evaluări

- TBBP2300008 01Document3 paginiTBBP2300008 01กัปตัน นเรศ สิงห์สอาดÎncă nu există evaluări

- TAX05-02 Individual Income TaxDocument7 paginiTAX05-02 Individual Income TaxJeth ConchaÎncă nu există evaluări

- Test Series - Set 5 - Ay 20-21Document16 paginiTest Series - Set 5 - Ay 20-21Urusi TeklaÎncă nu există evaluări

- Belize Customs Declaration - FormDocument1 paginăBelize Customs Declaration - FormMrs RichardsÎncă nu există evaluări

- Part I: Multiple - Choise Questions Choose The Only One Right Answer For Each QuestionDocument7 paginiPart I: Multiple - Choise Questions Choose The Only One Right Answer For Each QuestionHa TranÎncă nu există evaluări

- Take Home Quiz On Taxation Law Prepared By: Prof. AGN Concepts To StudyDocument3 paginiTake Home Quiz On Taxation Law Prepared By: Prof. AGN Concepts To StudyJImlan Sahipa IsmaelÎncă nu există evaluări

- Panasonic Communications Imaging Corp. v. CIRDocument3 paginiPanasonic Communications Imaging Corp. v. CIRAbigayle RecioÎncă nu există evaluări

- View Duplicate Invoice - AppleDocument3 paginiView Duplicate Invoice - AppleEduardo Gamez0% (1)

- Qualified Terminable Interest Property Qtip TrustDocument5 paginiQualified Terminable Interest Property Qtip Trustapi-246909910Încă nu există evaluări

- Sworn Application For Tax Clearance - Non-IndDocument2 paginiSworn Application For Tax Clearance - Non-IndArchie Lazaro0% (1)

- APL - Excise and Service Tax - Final - 03-17Document22 paginiAPL - Excise and Service Tax - Final - 03-17ananda_joshi5178Încă nu există evaluări

- StrataxDocument40 paginiStrataxAsh PadillaÎncă nu există evaluări

- TAX-402 (Other Percentage Taxes - Part 2)Document6 paginiTAX-402 (Other Percentage Taxes - Part 2)VKVCPlaysÎncă nu există evaluări

- 596 Idbi StatementDocument11 pagini596 Idbi Statementsri harshaÎncă nu există evaluări

- DeductionsDocument10 paginiDeductionsceline marasiganÎncă nu există evaluări

- Complete Articles of Incorporation ExampleDocument2 paginiComplete Articles of Incorporation ExampleNidhi SharmaÎncă nu există evaluări

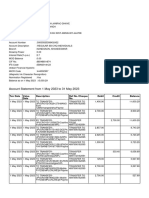

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 paginiAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027Încă nu există evaluări

- SODA Report For R70Document378 paginiSODA Report For R70Reji ThomasÎncă nu există evaluări

- Boat Airdopes 141 PDFDocument1 paginăBoat Airdopes 141 PDFSantosh SharmaÎncă nu există evaluări

- Self-Test 1Document8 paginiSelf-Test 1Dymphna Ann CalumpianoÎncă nu există evaluări

- Report TransactionsretyrDocument5 paginiReport TransactionsretyrPitirut Anca DanielaÎncă nu există evaluări

- OD327981941808242100Document1 paginăOD327981941808242100HATHEEKATHUL AROOSIYAÎncă nu există evaluări