S-ar putea să vă placă și

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- Blockchains: Where We Are and How They Will Change Risk ManagementDocument16 paginiBlockchains: Where We Are and How They Will Change Risk ManagementDudenÎncă nu există evaluări

- Financial MathematicsDocument107 paginiFinancial MathematicsDudenÎncă nu există evaluări

- Exchange Rates and Monetary Policy UncertaintyDocument48 paginiExchange Rates and Monetary Policy UncertaintyDudenÎncă nu există evaluări

- FinTech Journey and The HurdlesDocument22 paginiFinTech Journey and The HurdlesDudenÎncă nu există evaluări

- Behavioural Risk ManagementDocument20 paginiBehavioural Risk ManagementDudenÎncă nu există evaluări

- Cybersecurity Is Your Disclosure Discovery SecureDocument18 paginiCybersecurity Is Your Disclosure Discovery SecureDudenÎncă nu există evaluări

- Post-Energy RiskDocument23 paginiPost-Energy RiskDudenÎncă nu există evaluări

- P SyllabusDocument5 paginiP SyllabusDudenÎncă nu există evaluări

- Accounting For Insurance LiabilitiesDocument18 paginiAccounting For Insurance LiabilitiesDudenÎncă nu există evaluări

- Alternative Approaches To Modelling Non Maturing DepositsDocument23 paginiAlternative Approaches To Modelling Non Maturing DepositsDuden100% (1)

- Bonus Credit Equity FormsDocument1 paginăBonus Credit Equity FormsDudenÎncă nu există evaluări

- Challenges To Implementing CECLDocument20 paginiChallenges To Implementing CECLDudenÎncă nu există evaluări

- Investment & Financial Markets Exam-July 2019: Normal Distribution Calculator Prometric Web SiteDocument12 paginiInvestment & Financial Markets Exam-July 2019: Normal Distribution Calculator Prometric Web SiteDudenÎncă nu există evaluări

- Probability Measures in Financial MathematicsDocument3 paginiProbability Measures in Financial MathematicsDudenÎncă nu există evaluări

- Minority-Led Activist Hedge FundDocument4 paginiMinority-Led Activist Hedge FundDudenÎncă nu există evaluări

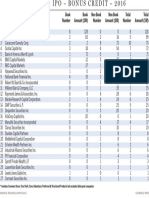

- Bonus Credit Equity IpoDocument1 paginăBonus Credit Equity IpoDudenÎncă nu există evaluări

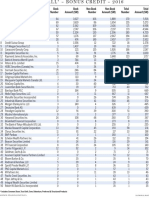

- Bonus Credit Government DebtDocument1 paginăBonus Credit Government DebtDudenÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- 17 People v. TibayanDocument11 pagini17 People v. TibayanStephanie SerapioÎncă nu există evaluări

- List of Students Not Allowed For Final Term Exam Due To Shortage of Attendance BBA 4th Cost Accounting Money Banking Oral CommunicationDocument7 paginiList of Students Not Allowed For Final Term Exam Due To Shortage of Attendance BBA 4th Cost Accounting Money Banking Oral CommunicationAhmad KhawajaÎncă nu există evaluări

- Week 7-8 Financial PlanningDocument16 paginiWeek 7-8 Financial PlanningCeejay0908Încă nu există evaluări

- Fdi Without& With AllianceDocument10 paginiFdi Without& With AlliancemiarahmadinaÎncă nu există evaluări

- Bank (Final)Document25 paginiBank (Final)MishuÎncă nu există evaluări

- Pyidawtha - The New BurmaDocument7 paginiPyidawtha - The New BurmaZarni Maw WinÎncă nu există evaluări

- Case 4 - Curled MetalDocument4 paginiCase 4 - Curled MetalSravya DoppaniÎncă nu există evaluări

- ACC 206 Week 3 Assignment Chapter Four and Five ProblemsDocument5 paginiACC 206 Week 3 Assignment Chapter Four and Five Problemshomeworktab0% (1)

- GEM3 Empirical NotesDocument60 paginiGEM3 Empirical Notesxy053333Încă nu există evaluări

- Content://com - Opera.mini - Native.operafile/?o File:///storage/emulated/0/download/. QBNEW uid1891%20PZRDocument8 paginiContent://com - Opera.mini - Native.operafile/?o File:///storage/emulated/0/download/. QBNEW uid1891%20PZRSanaya SinghÎncă nu există evaluări

- Five Minute InvestingDocument68 paginiFive Minute InvestingRajiv GandhiÎncă nu există evaluări

- Tata Tea WebsiteDocument59 paginiTata Tea WebsiteVikram KoradeÎncă nu există evaluări

- Business Finance AssignmentDocument3 paginiBusiness Finance Assignmentk_Dashy8465Încă nu există evaluări

- Event As The PromotionalDocument84 paginiEvent As The PromotionalMichael MendsÎncă nu există evaluări

- Curret Ratio Acid Test RatioDocument7 paginiCurret Ratio Acid Test RatioNIKHIL MATHEWÎncă nu există evaluări

- Income Tax Procedure PracticeU 12345 RB1Document20 paginiIncome Tax Procedure PracticeU 12345 RB1Chakram SirishaÎncă nu există evaluări

- Cadbury PROJECTDocument14 paginiCadbury PROJECTAnand singhÎncă nu există evaluări

- Finance MCQSDocument30 paginiFinance MCQSShakeelÎncă nu există evaluări

- Acc 550 Week 4 HomeworkDocument7 paginiAcc 550 Week 4 Homeworkjoannapsmith33Încă nu există evaluări

- GE 9 Cell MatrixDocument10 paginiGE 9 Cell MatrixMr. M. Sandeep Kumar0% (1)

- Circular 323-2016Document52 paginiCircular 323-2016Om PrakashÎncă nu există evaluări

- V2 Exam 2 PM PDFDocument30 paginiV2 Exam 2 PM PDFMaharishi VaidyaÎncă nu există evaluări

- Chapter 6 - TestbankDocument14 paginiChapter 6 - TestbankCharles MK ChanÎncă nu există evaluări

- ADV I Chapter 2 2009Document5 paginiADV I Chapter 2 2009temedebereÎncă nu există evaluări

- Equity Research Report - CiplaDocument8 paginiEquity Research Report - CiplaKrishu AgrawalÎncă nu există evaluări

- Lecture 3 Overview of Bond Sectors and InstrumentsDocument98 paginiLecture 3 Overview of Bond Sectors and InstrumentsAsadÎncă nu există evaluări

- Gael Sfeir - CVDocument1 paginăGael Sfeir - CVGaelÎncă nu există evaluări

- Capital Structure of A CompanyDocument83 paginiCapital Structure of A CompanyAnant GargÎncă nu există evaluări

- High Return Investing: Passive Income and Financial FreedomDocument12 paginiHigh Return Investing: Passive Income and Financial Freedomapi-154838839Încă nu există evaluări

- Port Mana - hdfc-22Document55 paginiPort Mana - hdfc-22MOHAMMED KHAYYUMÎncă nu există evaluări