S-ar putea să vă placă și

- Solution Manual For Essentials of Accounting For Governmental and Not For Profit Organizations 14th Edition Paul CopleyDocument14 paginiSolution Manual For Essentials of Accounting For Governmental and Not For Profit Organizations 14th Edition Paul CopleyCameronHerreracapt100% (39)

- Case 1 New (Signal Cable Company)Document6 paginiCase 1 New (Signal Cable Company)nicole100% (2)

- HDFC AMC Initiation - 9april2019Document31 paginiHDFC AMC Initiation - 9april2019Sunita ShrivastavaÎncă nu există evaluări

- Essentials of Managerial Finance 14th Edition Besley Solutions ManualDocument35 paginiEssentials of Managerial Finance 14th Edition Besley Solutions Manualbayedaidancerkobn8100% (30)

- Influencer Marketing Proposal 5Document11 paginiInfluencer Marketing Proposal 5Paul0% (1)

- Internal Control of Fixed Assets: A Controller and Auditor's GuideDe la EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideEvaluare: 4 din 5 stele4/5 (1)

- Financial Ratio Analysis-LiquidityDocument30 paginiFinancial Ratio Analysis-LiquidityZybel RosalesÎncă nu există evaluări

- The Use of Technical and Fundamental Analysis Kumar NaveenDocument296 paginiThe Use of Technical and Fundamental Analysis Kumar Naveensmeena100% (1)

- 978-1260004755 1260004759 Managerial EconomicsDocument17 pagini978-1260004755 1260004759 Managerial EconomicsReccebacaÎncă nu există evaluări

- Dwnload Full Financial Management Core Concepts 4th Edition Brooks Solutions Manual PDFDocument35 paginiDwnload Full Financial Management Core Concepts 4th Edition Brooks Solutions Manual PDFbenboydr8pl100% (13)

- FM SemesterDocument19 paginiFM SemesterSanjay VÎncă nu există evaluări

- WorksheetDocument37 paginiWorksheetKim FloresÎncă nu există evaluări

- Financial Leverage and Capital Structure Policy: Conducted by Ranjika Perera & Chanaka KarunasenaDocument53 paginiFinancial Leverage and Capital Structure Policy: Conducted by Ranjika Perera & Chanaka Karunasenacharitha007Încă nu există evaluări

- Fabm 2 - Module 6Document8 paginiFabm 2 - Module 6Kelvin SaplaÎncă nu există evaluări

- Capital Structure Theories ExplainedDocument10 paginiCapital Structure Theories ExplainedBaken D DhungyelÎncă nu există evaluări

- Accounting Principles 10th Edition Weygandt Kimmel Chapter 1 Solutions For Chapter 1 Accounting in ActionDocument44 paginiAccounting Principles 10th Edition Weygandt Kimmel Chapter 1 Solutions For Chapter 1 Accounting in ActionSumit Kumar Dam33% (3)

- Financial Analysis RatiosDocument17 paginiFinancial Analysis RatiosRajesh PatilÎncă nu există evaluări

- M&a Paper ACTG421Document11 paginiM&a Paper ACTG421Alex AdamovÎncă nu există evaluări

- Chapter 16 Tcdn GốcDocument37 paginiChapter 16 Tcdn GốcN KhÎncă nu există evaluări

- Chapters 4 and 5 Capital Structure Decision and Dividends & DividendDocument118 paginiChapters 4 and 5 Capital Structure Decision and Dividends & DividendKalkidan ZerihunÎncă nu există evaluări

- Non Performing Assets of BankDocument7 paginiNon Performing Assets of BankDivyaÎncă nu există evaluări

- FABM1 11 Quarter 4 Week 2 Las 2Document1 paginăFABM1 11 Quarter 4 Week 2 Las 2Janna PleteÎncă nu există evaluări

- Basic Accounting EquationDocument17 paginiBasic Accounting EquationArienaya100% (1)

- Ch-2 Financial Analysis &planningDocument27 paginiCh-2 Financial Analysis &planningMulatu LombamoÎncă nu există evaluări

- OVERVIEW OF FINANCIAL STATEMENT ANALYSIS (Trend, Horizontal..)Document8 paginiOVERVIEW OF FINANCIAL STATEMENT ANALYSIS (Trend, Horizontal..)Trixie Jane MolodÎncă nu există evaluări

- Accounting EquationDocument5 paginiAccounting Equationmbi87Încă nu există evaluări

- Open University Financial Accounting TransactionsDocument4 paginiOpen University Financial Accounting TransactionsKristine Jane Manalastas CullaÎncă nu există evaluări

- Case 1 New Signal Cable CompanyDocument6 paginiCase 1 New Signal Cable Companymilk teaÎncă nu există evaluări

- PowerPoint On Financial RatiosDocument31 paginiPowerPoint On Financial RatiosJimmyÎncă nu există evaluări

- Ratio AnalysisDocument13 paginiRatio AnalysisElizabeth TatadÎncă nu există evaluări

- Summative Quiz 2Document3 paginiSummative Quiz 2Sheena Gallentes LeysonÎncă nu există evaluări

- Basic Accounting Equation ExplainedDocument4 paginiBasic Accounting Equation ExplainedArienayaÎncă nu există evaluări

- Region IX, Zamboanga Peninsula Burgos ST., Molave, Zamboanga Del Sur 7023 Tel No. (062) 2251 507/ School ID No. 303797Document7 paginiRegion IX, Zamboanga Peninsula Burgos ST., Molave, Zamboanga Del Sur 7023 Tel No. (062) 2251 507/ School ID No. 303797Charlyn CastroÎncă nu există evaluări

- Capital StructureDocument31 paginiCapital StructureBagusSuciptoÎncă nu există evaluări

- Financial Management Exam QuestionsDocument4 paginiFinancial Management Exam QuestionsAlena TonyÎncă nu există evaluări

- F7 (FR) Workbook (Mix)Document6 paginiF7 (FR) Workbook (Mix)Aye Myat ThawtarÎncă nu există evaluări

- Chapter 1-4Document20 paginiChapter 1-4BookDownÎncă nu există evaluări

- Handouts 3 - CORPORATE LIQUIDATIONDocument7 paginiHandouts 3 - CORPORATE LIQUIDATIONcecille ramirezÎncă nu există evaluări

- Unit - Iv Cost and Management AccountingDocument12 paginiUnit - Iv Cost and Management AccountingRamakrishna RoshanÎncă nu există evaluări

- Financial Accounting and AnalysisDocument7 paginiFinancial Accounting and AnalysisKush BafnaÎncă nu există evaluări

- Contoh Soal - Test FGDocument1 paginăContoh Soal - Test FGhermanÎncă nu există evaluări

- Accounting Equation and Transactions ExplainedDocument11 paginiAccounting Equation and Transactions ExplainedMasum HossainÎncă nu există evaluări

- Balance SheetDocument20 paginiBalance SheetMarie FeÎncă nu există evaluări

- B326 MTA Fall 2017-2018 MGLDocument7 paginiB326 MTA Fall 2017-2018 MGLmjlÎncă nu există evaluări

- Exercices + Answers (Capital Structure) PDFDocument4 paginiExercices + Answers (Capital Structure) PDFSonal RathhiÎncă nu există evaluări

- Business Combination Valuation Case StudyDocument3 paginiBusiness Combination Valuation Case StudyHuỳnh Minh Gia HàoÎncă nu există evaluări

- ALEJAGA FM Project Week 4Document5 paginiALEJAGA FM Project Week 4Andrea Monique AlejagaÎncă nu există evaluări

- Please Review These Questions Before You Enter For Your Test and Final Examination Thank You AC405DDocument13 paginiPlease Review These Questions Before You Enter For Your Test and Final Examination Thank You AC405DELIZABETHÎncă nu există evaluări

- Understand Liabilities in 4 StepsTITLEDocument6 paginiUnderstand Liabilities in 4 StepsTITLEMai RuizÎncă nu există evaluări

- Unit 2 Financial Statement AnalysisDocument17 paginiUnit 2 Financial Statement AnalysisalemayehuÎncă nu există evaluări

- Part 4 Fundamentals of Accountancy 1Document24 paginiPart 4 Fundamentals of Accountancy 1mang tomasÎncă nu există evaluări

- Statement of Financial Position (SFP) : TNHS Main - SHS - Accountancy, Business and ManagementDocument10 paginiStatement of Financial Position (SFP) : TNHS Main - SHS - Accountancy, Business and ManagementPedana RañolaÎncă nu există evaluări

- Accounting IDocument18 paginiAccounting IMohammed mostafaÎncă nu există evaluări

- Financial Statement AnalysisDocument47 paginiFinancial Statement Analysisvini2710Încă nu există evaluări

- CMA Volume 2 MergedDocument153 paginiCMA Volume 2 MergedShyaambhavi NsÎncă nu există evaluări

- Study Unit Eight Activity Measures and FinancingDocument15 paginiStudy Unit Eight Activity Measures and FinancingPaul LteifÎncă nu există evaluări

- Financial Accounting & AnalysisDocument6 paginiFinancial Accounting & AnalysisRajni KumariÎncă nu există evaluări

- Theory of Capital Structure FMDocument25 paginiTheory of Capital Structure FMalphamal2017Încă nu există evaluări

- Session 5 Solutions Equity TransactionsDocument5 paginiSession 5 Solutions Equity TransactionsAngel MéndezÎncă nu există evaluări

- CHAPTER 3 (Notes 3)Document17 paginiCHAPTER 3 (Notes 3)Nor Farhanah NanaÎncă nu există evaluări

- Cash Flow Statement & Replacement Analysis PDFDocument7 paginiCash Flow Statement & Replacement Analysis PDFDip KunduÎncă nu există evaluări

- Chapter 2 Hyperinflation LectureDocument4 paginiChapter 2 Hyperinflation LectureChristine SondonÎncă nu există evaluări

- Case 1Document5 paginiCase 1noor memekÎncă nu există evaluări

- Partnership Liquidation GuideDocument13 paginiPartnership Liquidation GuideCharles TuazonÎncă nu există evaluări

- The Best-Practice EVA Software Toolkit: AppendixDocument3 paginiThe Best-Practice EVA Software Toolkit: AppendixAshutosh GuptaÎncă nu există evaluări

- Heineken - Family Control Provides “ Capacity To Suffer”Document4 paginiHeineken - Family Control Provides “ Capacity To Suffer”Ashutosh GuptaÎncă nu există evaluări

- Hospitals Initiating CoverageDocument23 paginiHospitals Initiating CoverageAshutosh GuptaÎncă nu există evaluări

- Spotlighting Ultramarine PigmentsDocument9 paginiSpotlighting Ultramarine PigmentsAshutosh GuptaÎncă nu există evaluări

- Filatex India LimitedDocument14 paginiFilatex India LimitedAshutosh GuptaÎncă nu există evaluări

- A Study of Performance Analysis of Gold Loan Nbfcs Based On Camels ModelDocument19 paginiA Study of Performance Analysis of Gold Loan Nbfcs Based On Camels ModelAshutosh GuptaÎncă nu există evaluări

- Hudson Value Partners Special Situations New AddressDocument7 paginiHudson Value Partners Special Situations New AddressAshutosh GuptaÎncă nu există evaluări

- Filatex India LimitedDocument14 paginiFilatex India LimitedAshutosh GuptaÎncă nu există evaluări

- Otc GuideDocument24 paginiOtc GuideAshutosh GuptaÎncă nu există evaluări

- Warren Buffett Way PDFDocument8 paginiWarren Buffett Way PDFIsrael ZepahuaÎncă nu există evaluări

- 1839 - ACE & APEX Shade CardDocument2 pagini1839 - ACE & APEX Shade CardAshutosh GuptaÎncă nu există evaluări

- Shaily Engineering Plastics Limited-09-25-2019Document4 paginiShaily Engineering Plastics Limited-09-25-2019Ashutosh Gupta100% (1)

- The Unusual Billionaires Saurabh Mukherjea: March 2018Document4 paginiThe Unusual Billionaires Saurabh Mukherjea: March 2018Ashutosh GuptaÎncă nu există evaluări

- COVID-19 Impact on Packaging CompanyDocument3 paginiCOVID-19 Impact on Packaging CompanyAshutosh GuptaÎncă nu există evaluări

- Thij NGH: Packaging LimitedDocument2 paginiThij NGH: Packaging LimitedAshutosh GuptaÎncă nu există evaluări

- Saurabh Mukherjea Profiles The Unusual Billionaires' From IndiaDocument2 paginiSaurabh Mukherjea Profiles The Unusual Billionaires' From IndiaAshutosh GuptaÎncă nu există evaluări

- Care Ratings Limited (Care) : Background Stock Performance DetailsDocument5 paginiCare Ratings Limited (Care) : Background Stock Performance DetailsAshutosh GuptaÎncă nu există evaluări

- Warehousing Industry October 2018Document14 paginiWarehousing Industry October 2018Mayank RankaÎncă nu există evaluări

- Natco IC 11june2019Document33 paginiNatco IC 11june2019Ashutosh GuptaÎncă nu există evaluări

- Q2-FY19 Result Update: CMP: 125 Target: 263Document7 paginiQ2-FY19 Result Update: CMP: 125 Target: 263Ashutosh GuptaÎncă nu există evaluări

- DB Corp Annual Report PDFDocument317 paginiDB Corp Annual Report PDFAshutosh GuptaÎncă nu există evaluări

- IT Sector 4QFY19 Results PreviewDocument16 paginiIT Sector 4QFY19 Results PreviewAshutosh GuptaÎncă nu există evaluări

- TanFac Ind LTD - 4 Jan 2013Document6 paginiTanFac Ind LTD - 4 Jan 2013Ashutosh GuptaÎncă nu există evaluări

- BLS International 2QFY19 (CMP Rs 128, Mcap Rs 13bn, Fair Value Rs 277)Document1 paginăBLS International 2QFY19 (CMP Rs 128, Mcap Rs 13bn, Fair Value Rs 277)Ashutosh GuptaÎncă nu există evaluări

- IDirect MahindraLog ICDocument28 paginiIDirect MahindraLog ICAshutosh GuptaÎncă nu există evaluări

- Mahindra Logistics IPO Note Provides Tech-Enabled Logistics Solutions OverviewDocument10 paginiMahindra Logistics IPO Note Provides Tech-Enabled Logistics Solutions OverviewAshutosh GuptaÎncă nu există evaluări

- Watts & Bolts: A Monthly Round-Up of Key Data & ImplicationsDocument15 paginiWatts & Bolts: A Monthly Round-Up of Key Data & ImplicationsAshutosh GuptaÎncă nu există evaluări

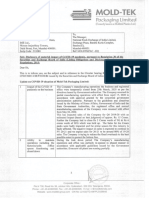

- Mold-Tek Packaging - Q3FY20 - RU - 14022020 - 17-02-2020 - 16Document6 paginiMold-Tek Packaging - Q3FY20 - RU - 14022020 - 17-02-2020 - 16Ashutosh GuptaÎncă nu există evaluări

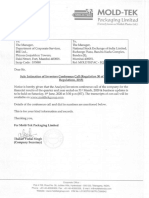

- Mold-Tek Packaging - Q4FY19 - Result Update - 12062019 - 13-06-2019 - 09Document6 paginiMold-Tek Packaging - Q4FY19 - Result Update - 12062019 - 13-06-2019 - 09Ashutosh GuptaÎncă nu există evaluări

- A real value risk model for emerging marketsDocument35 paginiA real value risk model for emerging marketsbutch28butch28Încă nu există evaluări

- No Man Can Serve Two MastersDocument11 paginiNo Man Can Serve Two Mastersnave88Încă nu există evaluări

- Star Health - RHPDocument474 paginiStar Health - RHPsaurabhÎncă nu există evaluări

- Azerbaijan Oil Company 2017 IFRS ReportsDocument96 paginiAzerbaijan Oil Company 2017 IFRS ReportsMehemmed MemmedliÎncă nu există evaluări

- Metrobank 2012 AnalysisDocument11 paginiMetrobank 2012 AnalysisJoyce Ann Sosa100% (1)

- Secondary Markets ExplainedDocument27 paginiSecondary Markets ExplainedNhi VõÎncă nu există evaluări

- UntitledDocument102 paginiUntitledPrima AditÎncă nu există evaluări

- Daily Equity Market Report - 18.01.2022Document1 paginăDaily Equity Market Report - 18.01.2022Fuaad DodooÎncă nu există evaluări

- Chapter 5 - Teacher's Manual - Far Part 1aDocument9 paginiChapter 5 - Teacher's Manual - Far Part 1aMark Anthony TibuleÎncă nu există evaluări

- CH 1 QaDocument5 paginiCH 1 QaAhmad Tawfiq DarabsehÎncă nu există evaluări

- Pilipinas Shell Vertical and Horizontal AnalysisDocument7 paginiPilipinas Shell Vertical and Horizontal Analysismaica G.Încă nu există evaluări

- Teaching Introduction To Managerial Accounting Using An Excel Spreadsheet ExampleDocument16 paginiTeaching Introduction To Managerial Accounting Using An Excel Spreadsheet Examplesamuel kebedeÎncă nu există evaluări

- Chapter 6 Controlling CashDocument10 paginiChapter 6 Controlling CashyenewÎncă nu există evaluări

- Satyarth Prakash Dwivedi-CvDocument5 paginiSatyarth Prakash Dwivedi-CvDesi Vanila IceÎncă nu există evaluări

- PAK - Resume Owais Ahmed - FC FM CFO 17 Yrs Exp - Owais AhmedDocument3 paginiPAK - Resume Owais Ahmed - FC FM CFO 17 Yrs Exp - Owais AhmedFahim FerozÎncă nu există evaluări

- Guidelines For Bonus IssueDocument23 paginiGuidelines For Bonus IssuePraneela100% (1)

- ACC3201Document6 paginiACC3201natlyhÎncă nu există evaluări

- Executive Summary: Financial AnalysisDocument67 paginiExecutive Summary: Financial AnalysisSachin JainÎncă nu există evaluări

- Creating Competitive Advantage 1Document18 paginiCreating Competitive Advantage 1Justin punelasÎncă nu există evaluări

- Stock Valuation - Wikipedia, The Free EncyclopediaDocument12 paginiStock Valuation - Wikipedia, The Free Encyclopediabhattpiyush93Încă nu există evaluări

- 09 Elms Quiz - ArgDocument3 pagini09 Elms Quiz - ArgKim Andrew Duane C. RosalesÎncă nu există evaluări

- Traditional & Modern Theory ApproachDocument12 paginiTraditional & Modern Theory Approachyash shah78% (9)

- Chapter 9: The Capital Asset Pricing Model: Problem SetsDocument10 paginiChapter 9: The Capital Asset Pricing Model: Problem SetsnouraÎncă nu există evaluări

- Chapter 14-Multinational Capital BudgetingDocument29 paginiChapter 14-Multinational Capital BudgetingDeloar Hossain SagorÎncă nu există evaluări

- SWAPDocument18 paginiSWAPashish3009Încă nu există evaluări

- Prepare Financial Statements From Trial Balance in ExcelDocument5 paginiPrepare Financial Statements From Trial Balance in ExcelShania FordeÎncă nu există evaluări

- Modigliani and Miller Reply to Criticism of Their TheoryDocument16 paginiModigliani and Miller Reply to Criticism of Their TheoryTrangÎncă nu există evaluări