S-ar putea să vă placă și

- Sea of Thieves 1Document34 paginiSea of Thieves 1Marcus MachadoÎncă nu există evaluări

- Fundamental Analysis of Bandhan BankDocument41 paginiFundamental Analysis of Bandhan BankAbhishekÎncă nu există evaluări

- Fundamental Analysis of Bandhan BankDocument41 paginiFundamental Analysis of Bandhan BankAbhishekÎncă nu există evaluări

- Individual Case Study Home DepotDocument13 paginiIndividual Case Study Home DepotMirandaLaBate100% (5)

- Strategic Decision MakingDocument14 paginiStrategic Decision MakingChandrajeet SharmaÎncă nu există evaluări

- Broker 1Document3 paginiBroker 1RituÎncă nu există evaluări

- MCQDocument15 paginiMCQjitendra100% (1)

- BusinessPlan BusinessSimulation 12-18-18Document76 paginiBusinessPlan BusinessSimulation 12-18-18Stephanie Ann Asuncion100% (2)

- Manorama IndustriesDocument35 paginiManorama IndustriesManas BaghÎncă nu există evaluări

- 1.1 Identifying The Market Problem To Be Solved or The Market Need To Be MetDocument23 pagini1.1 Identifying The Market Problem To Be Solved or The Market Need To Be MetJo-Angela BallenerÎncă nu există evaluări

- Answer KeyDocument33 paginiAnswer KeyRenz TitongÎncă nu există evaluări

- Consumer DurablesDocument29 paginiConsumer DurablesSwapnil Chinchwankar100% (1)

- Creating A Product Business CaseDocument7 paginiCreating A Product Business CaseDemand MetricÎncă nu există evaluări

- Asian Paints Research PaperDocument4 paginiAsian Paints Research PaperSunil RathodÎncă nu există evaluări

- Crisil Sme ConnectDocument52 paginiCrisil Sme ConnectbarkalyanÎncă nu există evaluări

- Written Analysis CaseDocument4 paginiWritten Analysis CaseKeeben Badoy100% (1)

- Name of Institiution Office Address: Fimmda Member ListDocument5 paginiName of Institiution Office Address: Fimmda Member ListAbhishek BiswasÎncă nu există evaluări

- India Office MarketView Q1 2019 PuneDocument7 paginiIndia Office MarketView Q1 2019 PuneAbhilash BhatÎncă nu există evaluări

- A Review of Stakeholder Management Performance Attributes in PDFDocument15 paginiA Review of Stakeholder Management Performance Attributes in PDFAbhishekÎncă nu există evaluări

- 500 India's Most Valuable Companies 2018Document76 pagini500 India's Most Valuable Companies 2018Naveen Cb100% (1)

- Bangaluru Commercial: Real Estate Analysis ofDocument16 paginiBangaluru Commercial: Real Estate Analysis ofmanojkumarmishratÎncă nu există evaluări

- Data BankDocument47 paginiData BankSanket AiyaÎncă nu există evaluări

- Auto Component ManufacturersDocument9 paginiAuto Component ManufacturersKishore NaiduÎncă nu există evaluări

- A Project Report On "Motilal Oswal Financial Service LTD"Document61 paginiA Project Report On "Motilal Oswal Financial Service LTD"Aman BasantwaniÎncă nu există evaluări

- Bangalore Office 1Q 2012 Cushman & WakefieldDocument2 paginiBangalore Office 1Q 2012 Cushman & WakefieldReuben JacobÎncă nu există evaluări

- Founded By: Nithin Kamath & Nikhil KamathDocument6 paginiFounded By: Nithin Kamath & Nikhil KamathTushar ranaÎncă nu există evaluări

- SEBI List of Defaulters 24 April 2018Document57 paginiSEBI List of Defaulters 24 April 2018Moneylife Foundation100% (1)

- List of Top 25 Audit Firms and Their Audit FeesDocument37 paginiList of Top 25 Audit Firms and Their Audit Feesibelieveinmagic000Încă nu există evaluări

- Mangalam CementDocument65 paginiMangalam Cementsejal2009100% (1)

- Sector Fund - Risk or Opportunity For InvestorsDocument46 paginiSector Fund - Risk or Opportunity For InvestorsGANESHÎncă nu există evaluări

- A Study On Awareness and Accessing Behavior of Demat AccountDocument21 paginiA Study On Awareness and Accessing Behavior of Demat AccountSana KhanÎncă nu există evaluări

- Balance Sheet A2z AccountingDocument21 paginiBalance Sheet A2z AccountingWilson PrashanthÎncă nu există evaluări

- Indiabulls Real Estate ProjectDocument12 paginiIndiabulls Real Estate ProjectYatin DhallÎncă nu există evaluări

- Bill DiscountingDocument43 paginiBill DiscountingVamshi Palavajala100% (1)

- IFCI EmpaneLMENT PDFDocument11 paginiIFCI EmpaneLMENT PDFSatyanarayana Moorthy Piratla100% (1)

- Burgundy Private Hurun India 500Document37 paginiBurgundy Private Hurun India 500Bhurishrwa AbhishekÎncă nu există evaluări

- Affordable HousingDocument11 paginiAffordable HousingMayank JainÎncă nu există evaluări

- Large Retailer 2020Document54 paginiLarge Retailer 2020surjitrajput8Încă nu există evaluări

- Wanaparthy Peddamandadi Peddamandadi GP INRM PlanDocument35 paginiWanaparthy Peddamandadi Peddamandadi GP INRM PlanSrajeshKÎncă nu există evaluări

- Company Profile: DLF Limited or DLF (Delhi Land and Finance) Is The India's Biggest Real Estate DeveloperDocument12 paginiCompany Profile: DLF Limited or DLF (Delhi Land and Finance) Is The India's Biggest Real Estate DeveloperAtul LxÎncă nu există evaluări

- Fintech Workshop Brochure PDFDocument4 paginiFintech Workshop Brochure PDFDharini Raje SisodiaÎncă nu există evaluări

- Census GurgaonDocument280 paginiCensus GurgaonRimjhim SwamiÎncă nu există evaluări

- Mms-Ente-Case StudyDocument2 paginiMms-Ente-Case Studyvivek ghatbandheÎncă nu există evaluări

- India Business Directory AgricultureDocument4 paginiIndia Business Directory AgricultureAnurag TiwariÎncă nu există evaluări

- "Indirect Tax (GST) ": A Project OnDocument56 pagini"Indirect Tax (GST) ": A Project OnTasmay EnterprisesÎncă nu există evaluări

- Shivam Real EstateDocument46 paginiShivam Real EstateTasmay EnterprisesÎncă nu există evaluări

- Dhanuka Agritech: LimitedDocument224 paginiDhanuka Agritech: LimitedPradeep HÎncă nu există evaluări

- Indore - Madhya Pradesh India - Business Industrial Directory Database List of Companies Small & Medium Enterprises - SME & Industries (.XLSX Excel Format) 6th EditionDocument3 paginiIndore - Madhya Pradesh India - Business Industrial Directory Database List of Companies Small & Medium Enterprises - SME & Industries (.XLSX Excel Format) 6th EditionSubaru StarÎncă nu există evaluări

- MR1753 - Mansi Sharma - 1CR19MBA44Document53 paginiMR1753 - Mansi Sharma - 1CR19MBA44ihda0farhatun0nisakÎncă nu există evaluări

- Strategic Management - UberEATS Case StudyDocument1 paginăStrategic Management - UberEATS Case StudyArti KumariÎncă nu există evaluări

- Jatin Ahuja Ceo Big Boy Toyz Presented by Mr. PrinceDocument6 paginiJatin Ahuja Ceo Big Boy Toyz Presented by Mr. Princesanskriti goelÎncă nu există evaluări

- Surat Outlet ListDocument7 paginiSurat Outlet ListKrishna PatelÎncă nu există evaluări

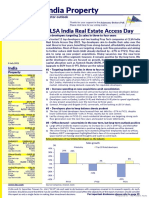

- India Property: CLSA India Real Estate Access DayDocument21 paginiIndia Property: CLSA India Real Estate Access DayManideep KumarÎncă nu există evaluări

- List of ExhibitorsDocument7 paginiList of ExhibitorsdeepakmukhiÎncă nu există evaluări

- Guidelines For Organizational Structure Training (OST) MBA (2022 - 2024 Batch)Document30 paginiGuidelines For Organizational Structure Training (OST) MBA (2022 - 2024 Batch)Arjun SalwanÎncă nu există evaluări

- Role of Angel Investor in IndiDocument13 paginiRole of Angel Investor in IndiValentine RothÎncă nu există evaluări

- FipbDocument608 paginiFipbrahul_nissanÎncă nu există evaluări

- Belkin - Dealer ListDocument6 paginiBelkin - Dealer ListJN ChoudhuriÎncă nu există evaluări

- List of The Top Sports Management Companies in IndiaDocument4 paginiList of The Top Sports Management Companies in IndiaAmardeep KaushalÎncă nu există evaluări

- List of IncubatorsDocument11 paginiList of IncubatorsAjit ChauhanÎncă nu există evaluări

- Business Plan For EdTech Startup - LearnSmart Case Study (Lecture 2)Document4 paginiBusiness Plan For EdTech Startup - LearnSmart Case Study (Lecture 2)BISMA RAFIQÎncă nu există evaluări

- NISM Mock TestDocument6 paginiNISM Mock Testdheerajw88Încă nu există evaluări

- Bright Flexi International Private Limited, PadubidireDocument9 paginiBright Flexi International Private Limited, PadubidirePratheek PoojaryÎncă nu există evaluări

- Lock Indusrty (CLG Report)Document31 paginiLock Indusrty (CLG Report)Radheyy Gupta100% (1)

- Enlistment Rule For Contractor in CPWDDocument55 paginiEnlistment Rule For Contractor in CPWDShahnawaz MohdÎncă nu există evaluări

- Directory of Associate 2014Document78 paginiDirectory of Associate 2014Edward SmithÎncă nu există evaluări

- Summer Internship ReportDocument21 paginiSummer Internship ReportSHIVANGI SINGH 212210430% (1)

- Acc Report On RMC Industry in AhmedabadDocument43 paginiAcc Report On RMC Industry in AhmedabadMaulik Padh100% (1)

- Market Research Organizations in IndiaDocument16 paginiMarket Research Organizations in IndiaJJMuthukattilÎncă nu există evaluări

- Ipo Report Polycab India Ltd.Document11 paginiIpo Report Polycab India Ltd.Pratik BobadeÎncă nu există evaluări

- Corporate Presentation PDFDocument28 paginiCorporate Presentation PDFAnonymous WOiz9n8Încă nu există evaluări

- LATENTVIEW - Investor Presentation - 24-Jan-23 - TickertapeDocument29 paginiLATENTVIEW - Investor Presentation - 24-Jan-23 - TickertapePeace KeeperÎncă nu există evaluări

- LATENTVIEW - Investor Presentation - 27-Jul-22 - TickertapeDocument29 paginiLATENTVIEW - Investor Presentation - 27-Jul-22 - Tickertapekishor bholeÎncă nu există evaluări

- Chapter-1 Economic AnalysisDocument56 paginiChapter-1 Economic AnalysisAbhishekÎncă nu există evaluări

- KhalifaDocument37 paginiKhalifaAbhishekÎncă nu există evaluări

- Sandeep PareekDocument53 paginiSandeep PareekAbhishekÎncă nu există evaluări

- Private Banks Fundamentals: Siddesh Naik Abhishek RanjanDocument19 paginiPrivate Banks Fundamentals: Siddesh Naik Abhishek RanjanAbhishekÎncă nu există evaluări

- Kev Issues in Telecommunications Planning PDFDocument11 paginiKev Issues in Telecommunications Planning PDFAbhishekÎncă nu există evaluări

- ConstructionprojectmanagementinIndia PDFDocument21 paginiConstructionprojectmanagementinIndia PDFAbhishekÎncă nu există evaluări

- Citation 46437553Document1 paginăCitation 46437553AbhishekÎncă nu există evaluări

- The Importance of Risk Assessment in The Context of Investment Project Management A Case Study PDFDocument9 paginiThe Importance of Risk Assessment in The Context of Investment Project Management A Case Study PDFAbhishekÎncă nu există evaluări

- Critical Success Factors in Large Projects in The Aerospace and Defense Sectors PDFDocument7 paginiCritical Success Factors in Large Projects in The Aerospace and Defense Sectors PDFAbhishekÎncă nu există evaluări

- Construction Project Management in IndiaDocument21 paginiConstruction Project Management in IndiaAbhishekÎncă nu există evaluări

- ConstructionprojectmanagementinIndia PDFDocument21 paginiConstructionprojectmanagementinIndia PDFAbhishekÎncă nu există evaluări

- A Review of Stakeholder Management Performance Attributes in PDFDocument15 paginiA Review of Stakeholder Management Performance Attributes in PDFAbhishekÎncă nu există evaluări

- Kev Issues in Telecommunications Planning PDFDocument11 paginiKev Issues in Telecommunications Planning PDFAbhishekÎncă nu există evaluări

- Managing The Project Management Importnat PDFDocument7 paginiManaging The Project Management Importnat PDFAbhishekÎncă nu există evaluări

- Kev Issues in Telecommunications Planning PDFDocument11 paginiKev Issues in Telecommunications Planning PDFAbhishekÎncă nu există evaluări

- Managing The Project Management Importnat PDFDocument7 paginiManaging The Project Management Importnat PDFAbhishekÎncă nu există evaluări

- Critical Success Factors in Large Projects in The Aerospace and Defense Sectors PDFDocument7 paginiCritical Success Factors in Large Projects in The Aerospace and Defense Sectors PDFAbhishekÎncă nu există evaluări

- Project Management Concepts and Applications Mba-532ADocument25 paginiProject Management Concepts and Applications Mba-532AAbhishekÎncă nu există evaluări

- PM Course PackDocument22 paginiPM Course PackAbhishekÎncă nu există evaluări

- Budget For IPL MatchDocument3 paginiBudget For IPL MatchAbhishekÎncă nu există evaluări

- Case StudyDocument12 paginiCase StudyAbhishekÎncă nu există evaluări

- Case Study Part 1Document13 paginiCase Study Part 1AbhishekÎncă nu există evaluări

- 1 Criteria Weights Project 1 Total of P1: Ipl FinalDocument20 pagini1 Criteria Weights Project 1 Total of P1: Ipl FinalAbhishekÎncă nu există evaluări

- A Report Submitted On Qualitative Analysis of HDFC BankDocument24 paginiA Report Submitted On Qualitative Analysis of HDFC BankAbhishek100% (1)

- Project ScopeDocument2 paginiProject ScopeAbhishekÎncă nu există evaluări

- The Coimbatore Bypass Road ProjectDocument5 paginiThe Coimbatore Bypass Road ProjectAbhishekÎncă nu există evaluări

- Case Study AnswersDocument1 paginăCase Study AnswersAbhishekÎncă nu există evaluări

- OGILVY's Report On E27's Social Media StrategiesDocument4 paginiOGILVY's Report On E27's Social Media Strategiese27100% (2)

- Team 8Document22 paginiTeam 8LaVette LaGonÎncă nu există evaluări

- Screening For Dollars: Craig Wallin September 3, 2014Document2 paginiScreening For Dollars: Craig Wallin September 3, 2014James ZacharyÎncă nu există evaluări

- REPORT GvmitmDocument85 paginiREPORT GvmitmKanisha MittalÎncă nu există evaluări

- Nontsikelelo Mbatha CV Without ImageDocument3 paginiNontsikelelo Mbatha CV Without ImageNtsiki MbathaÎncă nu există evaluări

- Rubric For Marking Case StudyDocument6 paginiRubric For Marking Case Study127amasonÎncă nu există evaluări

- Salaar FlourDocument71 paginiSalaar FlourZubair TradersÎncă nu există evaluări

- Bussines Development StrategyDocument27 paginiBussines Development Strategymuhammad rizqi agustinoÎncă nu există evaluări

- Meditech Surgical: Group MembersDocument18 paginiMeditech Surgical: Group MembersPatxiAranaÎncă nu există evaluări

- Marketing Midterm KeytermsDocument4 paginiMarketing Midterm KeytermsRihana Nhat KhueÎncă nu există evaluări

- Calza Passaro EDI 1997 PDFDocument15 paginiCalza Passaro EDI 1997 PDFRafia TariqÎncă nu există evaluări

- Personal Brand Creation TemplateDocument1 paginăPersonal Brand Creation Templateavik0381Încă nu există evaluări

- Egypt Country Commercial GuideDocument128 paginiEgypt Country Commercial GuideAlann83Încă nu există evaluări

- Pradeep TihadiaDocument2 paginiPradeep TihadiasayaaqÎncă nu există evaluări

- A Summer Internship Project Genmo LabsDocument46 paginiA Summer Internship Project Genmo Labssaikumar0% (2)

- Board of DirectorDocument5 paginiBoard of DirectorjatinÎncă nu există evaluări

- Kalinga Commercial Corporation New FinalDocument21 paginiKalinga Commercial Corporation New Finalsekhar_chanduÎncă nu există evaluări

- Business Plan. Group 4. BSN-1Document15 paginiBusiness Plan. Group 4. BSN-1jazzermill acobÎncă nu există evaluări

- Dhonuk Case StudyDocument25 paginiDhonuk Case StudyvinaytoshchoudharyÎncă nu există evaluări