S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

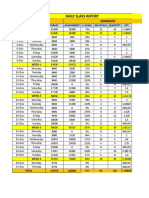

- DSR Sales ReportDocument11 paginiDSR Sales ReportSHRIKANT SAHUÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Process CostingDocument3 paginiProcess CostingSHRIKANT SAHUÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Direct Tax (Capital Gain) PDFDocument4 paginiDirect Tax (Capital Gain) PDFSHRIKANT SAHUÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- Direct Tax (Capital Gain)Document4 paginiDirect Tax (Capital Gain)SHRIKANT SAHUÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Paper 11 OcDocument1 paginăPaper 11 OcSHRIKANT SAHUÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Scope of IncomeDocument46 paginiScope of IncomeSHRIKANT SAHUÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Induction FormDocument28 paginiInduction FormSHRIKANT SAHUÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- SegrigationDocument13 paginiSegrigationSHRIKANT SAHUÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- CENG 5503 Intro to Steel & Timber StructuresDocument37 paginiCENG 5503 Intro to Steel & Timber StructuresBern Moses DuachÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- Open Far CasesDocument8 paginiOpen Far CasesGDoony8553Încă nu există evaluări

- Reading and Writing Q1 - M13Document13 paginiReading and Writing Q1 - M13Joshua Lander Soquita Cadayona100% (1)

- Laryngeal Diseases: Laryngitis, Vocal Cord Nodules / Polyps, Carcinoma LarynxDocument52 paginiLaryngeal Diseases: Laryngitis, Vocal Cord Nodules / Polyps, Carcinoma LarynxjialeongÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Stroboscopy For Benign Laryngeal Pathology in Evidence Based Health CareDocument5 paginiStroboscopy For Benign Laryngeal Pathology in Evidence Based Health CareDoina RusuÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Joining Instruction 4 Years 22 23Document11 paginiJoining Instruction 4 Years 22 23Salmini ShamteÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- EA Linear RegressionDocument3 paginiEA Linear RegressionJosh RamosÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Bad DayDocument3 paginiBad DayLink YouÎncă nu există evaluări

- Essential Rendering BookDocument314 paginiEssential Rendering BookHelton OliveiraÎncă nu există evaluări

- eHMI tool download and install guideDocument19 paginieHMI tool download and install guideNam Vũ0% (1)

- Business Case PresentationDocument27 paginiBusiness Case Presentationapi-253435256Încă nu există evaluări

- Technical specifications for JR3 multi-axis force-torque sensor modelsDocument1 paginăTechnical specifications for JR3 multi-axis force-torque sensor modelsSAN JUAN BAUTISTAÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Maharashtra Auto Permit Winner ListDocument148 paginiMaharashtra Auto Permit Winner ListSadik Shaikh50% (2)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- DBMS Architecture FeaturesDocument30 paginiDBMS Architecture FeaturesFred BloggsÎncă nu există evaluări

- Form Active Structure TypesDocument5 paginiForm Active Structure TypesShivanshu singh100% (1)

- !!!Логос - конференц10.12.21 копіяDocument141 pagini!!!Логос - конференц10.12.21 копіяНаталія БондарÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- PEDs and InterferenceDocument28 paginiPEDs and Interferencezakool21Încă nu există evaluări

- AD Chemicals - Freeze-Flash PointDocument4 paginiAD Chemicals - Freeze-Flash Pointyb3yonnayÎncă nu există evaluări

- Mrs. Universe PH - Empowering Women, Inspiring ChildrenDocument2 paginiMrs. Universe PH - Empowering Women, Inspiring ChildrenKate PestanasÎncă nu există evaluări

- HP HP3-X11 Exam: A Composite Solution With Just One ClickDocument17 paginiHP HP3-X11 Exam: A Composite Solution With Just One ClicksunnyÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Evil Days of Luckless JohnDocument5 paginiEvil Days of Luckless JohnadikressÎncă nu există evaluări

- LIST OF ENROLLED MEMBERS OF SAHIWAL CHAMBER OF COMMERCEDocument126 paginiLIST OF ENROLLED MEMBERS OF SAHIWAL CHAMBER OF COMMERCEBASIT Ali KhanÎncă nu există evaluări

- Ratio Analysis of PIADocument16 paginiRatio Analysis of PIAMalik Saad Noman100% (5)

- DOE Tank Safety Workshop Presentation on Hydrogen Tank TestingDocument36 paginiDOE Tank Safety Workshop Presentation on Hydrogen Tank TestingAlex AbakumovÎncă nu există evaluări

- Statistical Decision AnalysisDocument3 paginiStatistical Decision AnalysisTewfic SeidÎncă nu există evaluări

- Cableado de TermocuplasDocument3 paginiCableado de TermocuplasRUBEN DARIO BUCHELLYÎncă nu există evaluări

- LegoDocument30 paginiLegomzai2003Încă nu există evaluări

- LSMW With Rfbibl00Document14 paginiLSMW With Rfbibl00abbasx0% (1)

- Equilibruim of Forces and How Three Forces Meet at A PointDocument32 paginiEquilibruim of Forces and How Three Forces Meet at A PointSherif Yehia Al MaraghyÎncă nu există evaluări

- Inventory ControlDocument26 paginiInventory ControlhajarawÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)