S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Exhibit Discovery Letter Exhibits N.Y V SRVHSDocument87 paginiExhibit Discovery Letter Exhibits N.Y V SRVHSSouwesterdocsÎncă nu există evaluări

- Michael and Jennifer Brabson Preliminary ReportDocument10 paginiMichael and Jennifer Brabson Preliminary ReportmikekvolpeÎncă nu există evaluări

- Notes Cases Succession Art. 805-806Document17 paginiNotes Cases Succession Art. 805-806Alex RamosÎncă nu există evaluări

- Amado MacasaetDocument2 paginiAmado MacasaetNathalie TanÎncă nu există evaluări

- ATTCustomerServiceSummary OrdId 100087931Document6 paginiATTCustomerServiceSummary OrdId 100087931Diwakar RajaÎncă nu există evaluări

- Bill of Rights Sec 1Document295 paginiBill of Rights Sec 1Anabelle Talao-UrbanoÎncă nu există evaluări

- Mendoza-Ong vs. Sandiganbayan 414 SCRA 181 23oct2003 PDFDocument11 paginiMendoza-Ong vs. Sandiganbayan 414 SCRA 181 23oct2003 PDFGJ LaderaÎncă nu există evaluări

- League of Cities Vs ComelecDocument2 paginiLeague of Cities Vs Comelecangelsu04Încă nu există evaluări

- Legal Research Memorandum - Company BDocument7 paginiLegal Research Memorandum - Company BJillian AsdalaÎncă nu există evaluări

- SPA RefundDocument2 paginiSPA Refundakocmacky50% (4)

- In Re - Judge MarcosDocument9 paginiIn Re - Judge MarcosJon Joshua FalconeÎncă nu există evaluări

- Petitioner's Claim For Refund or Issuance of Tax Credit Certificate Representing Alleged Excess and Unutilized Input VAT For Taxable YearDocument1 paginăPetitioner's Claim For Refund or Issuance of Tax Credit Certificate Representing Alleged Excess and Unutilized Input VAT For Taxable YearPrhylleÎncă nu există evaluări

- Art 1458 Photoshop SalesDocument1 paginăArt 1458 Photoshop SalesPrhylleÎncă nu există evaluări

- Sales Lease Rent Civil Code NotesDocument3 paginiSales Lease Rent Civil Code NotesPrhylleÎncă nu există evaluări

- Fujen Hooo ProsecutionDocument1 paginăFujen Hooo ProsecutionPrhylleÎncă nu există evaluări

- Expenses Subject To CWTDocument3 paginiExpenses Subject To CWTPrhylleÎncă nu există evaluări

- G. R. No. 167146 PDFDocument16 paginiG. R. No. 167146 PDFPrhylleÎncă nu există evaluări

- G.R. Nos. L-48134-37 Whatever Is ItDocument6 paginiG.R. Nos. L-48134-37 Whatever Is ItPrhylleÎncă nu există evaluări

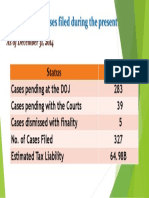

- RATE STATUS Dec 2014 - CopyDocument1 paginăRATE STATUS Dec 2014 - CopyPrhylleÎncă nu există evaluări

- Yomade Aborishade Defense Sentencing MemoDocument9 paginiYomade Aborishade Defense Sentencing MemoEmily BabayÎncă nu există evaluări

- Peoria County Jail Booking Sheet 6/19/2016Document8 paginiPeoria County Jail Booking Sheet 6/19/2016Journal Star police documentsÎncă nu există evaluări

- Villaluz v. Zaldivar, G.R. No. L-22754, December 31, 1965.Document3 paginiVillaluz v. Zaldivar, G.R. No. L-22754, December 31, 1965.Emerson NunezÎncă nu există evaluări

- ChecklistDocument27 paginiChecklistTinn ApÎncă nu există evaluări

- Poe-Llamanzares Vs ComelecDocument372 paginiPoe-Llamanzares Vs ComelecDean LozarieÎncă nu există evaluări

- UNITED STATES v. NICOLAS JAVIER, ET AL G.R. No. 10379 August 5, 1915 PDFDocument4 paginiUNITED STATES v. NICOLAS JAVIER, ET AL G.R. No. 10379 August 5, 1915 PDFIvan Angelo ApostolÎncă nu există evaluări

- Format of Suit of Dissolution of Marriage On The Basis of KhulaDocument4 paginiFormat of Suit of Dissolution of Marriage On The Basis of KhulaHome TuitionÎncă nu există evaluări

- Ethics Individual AssignmentDocument4 paginiEthics Individual AssignmentIan MurimiÎncă nu există evaluări

- Civil Liberties Union V Executive Secretary (194 SCRA 317)Document7 paginiCivil Liberties Union V Executive Secretary (194 SCRA 317)Grace DÎncă nu există evaluări

- Indemnification Clauses: A Practical Look at Everyday IssuesDocument149 paginiIndemnification Clauses: A Practical Look at Everyday IssuesewhittemÎncă nu există evaluări

- MCKEE V IACDocument5 paginiMCKEE V IACMario BagesbesÎncă nu există evaluări

- EJKDocument8 paginiEJKmz rphÎncă nu există evaluări

- The Survey Act, 1875Document32 paginiThe Survey Act, 1875Rizwan Niaz RaiyanÎncă nu există evaluări

- U.S. Bill of RightsDocument3 paginiU.S. Bill of RightsfreemantruthÎncă nu există evaluări

- Royaya Bte Abdullah & Anor V Public ProsecutorDocument7 paginiRoyaya Bte Abdullah & Anor V Public ProsecutorDima Naquira Mohd RafiÎncă nu există evaluări

- Reported By: Tomelden, Arvin LDocument14 paginiReported By: Tomelden, Arvin LJerrielle CastroÎncă nu există evaluări

- Incest in Zimbabwe and South America NewDocument7 paginiIncest in Zimbabwe and South America NewFaraiÎncă nu există evaluări

- AuthoritarianDocument4 paginiAuthoritarianMarketing ResearchÎncă nu există evaluări

- Rem 2 FinalsDocument133 paginiRem 2 FinalsBay NazarenoÎncă nu există evaluări