S-ar putea să vă placă și

- Intorductory Statistics, Chapter 1 - Prem MannDocument47 paginiIntorductory Statistics, Chapter 1 - Prem MannKazi93_thefat83% (6)

- Enterprise Machine Learning Guide: The Executive's Playbook For Business Success With Machine LearningDocument17 paginiEnterprise Machine Learning Guide: The Executive's Playbook For Business Success With Machine LearningankitÎncă nu există evaluări

- Applying AI in Industries: AnalysisDocument18 paginiApplying AI in Industries: AnalysisChitta KarthikÎncă nu există evaluări

- IPC2022-87236 - Overcoming Challenges Using Machine LearningDocument10 paginiIPC2022-87236 - Overcoming Challenges Using Machine LearningOswaldo MontenegroÎncă nu există evaluări

- DP-900 Exam 1-50Document50 paginiDP-900 Exam 1-50jose_porras_19Încă nu există evaluări

- Marketing Plan For SonicDocument11 paginiMarketing Plan For SonicZanyTime50% (4)

- Big Data in Financial ServicesDocument20 paginiBig Data in Financial ServicesPALLAVI KAMBLEÎncă nu există evaluări

- Workbook AI Mastery BRANTIONDocument30 paginiWorkbook AI Mastery BRANTIONmartinovic.m04Încă nu există evaluări

- Discovering AI Application Across Value ChainDocument3 paginiDiscovering AI Application Across Value ChainSwarnendu BiswasÎncă nu există evaluări

- Security Challenges in The Evolving Fintech LandscapeDocument8 paginiSecurity Challenges in The Evolving Fintech LandscapeMorick GibsonÎncă nu există evaluări

- 1b - McKinsey - How-Pharma-Can-Accelerate-Business-Impact-From-Advanced-Analytics PDFDocument10 pagini1b - McKinsey - How-Pharma-Can-Accelerate-Business-Impact-From-Advanced-Analytics PDFDinesh PillaipakkamnattÎncă nu există evaluări

- How Is AI Changing The World We Live inDocument4 paginiHow Is AI Changing The World We Live inSyeda AlishaÎncă nu există evaluări

- Data Protection United StatesDocument10 paginiData Protection United Statesaquinas03Încă nu există evaluări

- Digital Exchange All Published Assets April 2020Document78 paginiDigital Exchange All Published Assets April 2020RKMÎncă nu există evaluări

- Banking Value ChainDocument13 paginiBanking Value ChainAshutosh MohapatraÎncă nu există evaluări

- Advanced Customer AnalyticsDocument36 paginiAdvanced Customer AnalyticsAnonymous 3Uu7G3mP11Încă nu există evaluări

- Analytics and Big DataDocument38 paginiAnalytics and Big DataSreeprada V100% (1)

- Salesforce CPG and Retailers EbookDocument11 paginiSalesforce CPG and Retailers EbookBayCreativeÎncă nu există evaluări

- Westfleet Buyers Guide 2019-11-17Document43 paginiWestfleet Buyers Guide 2019-11-17kbrinaldiÎncă nu există evaluări

- Business Analytics and Business GrowthDocument12 paginiBusiness Analytics and Business GrowthKhyati B. ShahÎncă nu există evaluări

- Analytics in Action - How Marketelligent Helped A Quick Service Restaurant Chain Identify Customer Pain PointsDocument2 paginiAnalytics in Action - How Marketelligent Helped A Quick Service Restaurant Chain Identify Customer Pain PointsMarketelligentÎncă nu există evaluări

- Dataiku Healthcare Fraud Detection GuideDocument20 paginiDataiku Healthcare Fraud Detection GuideSang VuÎncă nu există evaluări

- Spencer: Privacy and Predictive Analytics in E-CommerceDocument19 paginiSpencer: Privacy and Predictive Analytics in E-CommerceNew England Law ReviewÎncă nu există evaluări

- Improving Performance of Spatio-Temporal Machine Learning Models Using Forward Feature Selection and Target-Oriented ValidationDocument9 paginiImproving Performance of Spatio-Temporal Machine Learning Models Using Forward Feature Selection and Target-Oriented Validations8nd11d UNIÎncă nu există evaluări

- Big Data Analytics Implementation in Banking Industry Case Study Cross Selling Activity in Indonesias Commercial BankDocument12 paginiBig Data Analytics Implementation in Banking Industry Case Study Cross Selling Activity in Indonesias Commercial BankAli RakhmanÎncă nu există evaluări

- Business Analytics IntroductionDocument37 paginiBusiness Analytics IntroductionTejash GannabattulaÎncă nu există evaluări

- The Forrester Wave-Master Data Management Solutions, Q1 2014Document17 paginiThe Forrester Wave-Master Data Management Solutions, Q1 2014Pallavi ReddyÎncă nu există evaluări

- PwC's Health Research Institute ReportDocument21 paginiPwC's Health Research Institute ReportHLMeditÎncă nu există evaluări

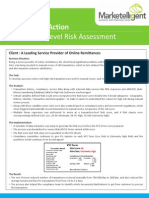

- Analytics in Action - How Marketelligent Helped An Online Remittance Firm Identify Risky TransactionsDocument2 paginiAnalytics in Action - How Marketelligent Helped An Online Remittance Firm Identify Risky TransactionsMarketelligentÎncă nu există evaluări

- Researching Alzheimer's Medicines - Setbacks and Stepping StonesDocument20 paginiResearching Alzheimer's Medicines - Setbacks and Stepping StonesOscar EspinozaÎncă nu există evaluări

- Types of Protists NotesDocument21 paginiTypes of Protists NotesMuhammad SayyadÎncă nu există evaluări

- Advanced Analytics for Government The Ultimate Step-By-Step GuideDe la EverandAdvanced Analytics for Government The Ultimate Step-By-Step GuideÎncă nu există evaluări

- DataOps Strategy A Complete Guide - 2020 EditionDe la EverandDataOps Strategy A Complete Guide - 2020 EditionEvaluare: 1 din 5 stele1/5 (2)

- Analytics in Action - How Marketelligent Helped A CPG Company Boost Store Order ValueDocument2 paginiAnalytics in Action - How Marketelligent Helped A CPG Company Boost Store Order ValueMarketelligentÎncă nu există evaluări

- Augmented Analytics Feb22 Rsallam 379393Document61 paginiAugmented Analytics Feb22 Rsallam 379393Foresight B.I. Solutions Inc.100% (1)

- Accenture Data Management Emerging Trends PDFDocument5 paginiAccenture Data Management Emerging Trends PDFjunohcu310Încă nu există evaluări

- Analytics in Action - How Marketelligent Helped A Retailer Rationalize SKU'sDocument2 paginiAnalytics in Action - How Marketelligent Helped A Retailer Rationalize SKU'sMarketelligentÎncă nu există evaluări

- Gartner Build A Data Driven Enterprise August 2019Document14 paginiGartner Build A Data Driven Enterprise August 2019BusisiweÎncă nu există evaluări

- Artificial Intelligence: Strategies For Leading Business TransformationDocument17 paginiArtificial Intelligence: Strategies For Leading Business TransformationRista55Încă nu există evaluări

- Private Equity Opportunities in Healthcare Tech VFDocument9 paginiPrivate Equity Opportunities in Healthcare Tech VFGm BaigÎncă nu există evaluări

- The Key To Delivering Analytics Advantage: Your PeopleDocument19 paginiThe Key To Delivering Analytics Advantage: Your PeopleADRIANA LOPEZ100% (1)

- 5 New Trends in BankingDocument8 pagini5 New Trends in BankingOrooj Siddiqui QaziÎncă nu există evaluări

- Become A Board AdvisorDocument5 paginiBecome A Board AdvisorWrite OriginalÎncă nu există evaluări

- Creating The Right For Startups: AI StrategyDocument23 paginiCreating The Right For Startups: AI StrategyYunquanÎncă nu există evaluări

- Analytics in Action - How Marketelligent Helped Increase Customer Engagement Via Targeted Cross-SellDocument2 paginiAnalytics in Action - How Marketelligent Helped Increase Customer Engagement Via Targeted Cross-SellMarketelligentÎncă nu există evaluări

- MismoDocument6 paginiMismoprabhublazeÎncă nu există evaluări

- Risk Estimation On High Frequency Financial DataDocument78 paginiRisk Estimation On High Frequency Financial DataXiaoyue ChenÎncă nu există evaluări

- Machine Learning Based Recommender System For E-CommerceDocument9 paginiMachine Learning Based Recommender System For E-CommerceIAES IJAIÎncă nu există evaluări

- Calculus in Football 1Document4 paginiCalculus in Football 1api-5459504270% (1)

- Venture Capital ReportDocument28 paginiVenture Capital ReportStarlettTVÎncă nu există evaluări

- Graph Technology Buyers Guide EN A4Document34 paginiGraph Technology Buyers Guide EN A4mona_mi8202Încă nu există evaluări

- Creating An Enterprise Data StrategyDocument5 paginiCreating An Enterprise Data StrategyTredence Analytics0% (1)

- PM Interview - 1Document57 paginiPM Interview - 1vrajagopal1Încă nu există evaluări

- Big Data Research: Shaokun Fan, Raymond Y.K. Lau, J. Leon ZhaoDocument5 paginiBig Data Research: Shaokun Fan, Raymond Y.K. Lau, J. Leon Zhaojulian zuluaga ochoaÎncă nu există evaluări

- Building A Data Empowered Company Domo Ebook PDFDocument12 paginiBuilding A Data Empowered Company Domo Ebook PDFDostfijiÎncă nu există evaluări

- InfoAdvisors MDM Neo4j GraphDocument14 paginiInfoAdvisors MDM Neo4j GraphRonald Paguay100% (1)

- Deception & Detection-On Amazon Reviews DatasetDocument9 paginiDeception & Detection-On Amazon Reviews Datasetyavar khanÎncă nu există evaluări

- SAP Process Mining by Celonis PDFDocument9 paginiSAP Process Mining by Celonis PDFSepty WaldaniaÎncă nu există evaluări

- Centers Of Excellence A Complete Guide - 2019 EditionDe la EverandCenters Of Excellence A Complete Guide - 2019 EditionÎncă nu există evaluări

- Using Customer Behavior Analytics To Increase RevenueDocument13 paginiUsing Customer Behavior Analytics To Increase RevenueBesty Afrah HasyatiÎncă nu există evaluări

- Allocation Rules For CRMDocument11 paginiAllocation Rules For CRMEkta VadgamaÎncă nu există evaluări

- Magic Quadrant For Data Masking TechnologyDocument11 paginiMagic Quadrant For Data Masking TechnologyGabriel SilerÎncă nu există evaluări

- White Paper - The Ultimate Guide To Data Sources and TechnologiesDocument22 paginiWhite Paper - The Ultimate Guide To Data Sources and TechnologiesFabrice K RascoÎncă nu există evaluări

- Presentation Hell: From Painful Presentations to Better StoriesDe la EverandPresentation Hell: From Painful Presentations to Better StoriesÎncă nu există evaluări

- CREAFORM Accessories Catalogue 2016Document44 paginiCREAFORM Accessories Catalogue 2016Xaocka100% (1)

- 360 Getting StartedDocument157 pagini360 Getting Started강성용Încă nu există evaluări

- Solution For All Problems in Chapter 9Document3 paginiSolution For All Problems in Chapter 9Rahmat Hidayat100% (1)

- Trade Manager (TM) : Expert AdvisorDocument21 paginiTrade Manager (TM) : Expert AdvisorDavid PutraÎncă nu există evaluări

- The LLL AlgorithmsDocument503 paginiThe LLL AlgorithmsCom DigfulÎncă nu există evaluări

- Cryptography, Winter Term 16/17: Sample Solution To Assignment 5Document3 paginiCryptography, Winter Term 16/17: Sample Solution To Assignment 5Safenat SafenatÎncă nu există evaluări

- Python Syllabus For Engineers - EngDocument2 paginiPython Syllabus For Engineers - EngmansourÎncă nu există evaluări

- API As A Product - Paypal SR PMDocument17 paginiAPI As A Product - Paypal SR PMjosh_wiggintonÎncă nu există evaluări

- 2V0-620 Examcollection Premium Exam Dumps 173q PDFDocument39 pagini2V0-620 Examcollection Premium Exam Dumps 173q PDFMohammad Tufail100% (2)

- Disk Space Is Not Released After Deleting Many FilesDocument3 paginiDisk Space Is Not Released After Deleting Many Fileselcaso34Încă nu există evaluări

- Patient Monitoring System Project Report OriginalDocument84 paginiPatient Monitoring System Project Report OriginalAmar Dharmadhikari62% (13)

- CSC 2304 01 - Syllabus - Computer ArchitectureDocument4 paginiCSC 2304 01 - Syllabus - Computer ArchitectureAmine NaitlhoÎncă nu există evaluări

- Audiocodes Session Border Controllers Mediant™ 800: Hybrid SBC and Media GatewayDocument2 paginiAudiocodes Session Border Controllers Mediant™ 800: Hybrid SBC and Media GatewayYen Lung LeeÎncă nu există evaluări

- Stucor Aucr2017 Landscape-3Document103 paginiStucor Aucr2017 Landscape-3Jeshanth JsÎncă nu există evaluări

- Three Schema Architecture: 1. Physical LayerDocument3 paginiThree Schema Architecture: 1. Physical Layerpartha sarathi guggiriÎncă nu există evaluări

- W & T SwitchDocument260 paginiW & T SwitchJeromeÎncă nu există evaluări

- NNTN7392 IMPRES BattReader UGDocument63 paginiNNTN7392 IMPRES BattReader UGmarko.jurcevicÎncă nu există evaluări

- Exam Question DumpDocument28 paginiExam Question DumpnikeshÎncă nu există evaluări

- 3 - Aac - Mini Project - Report TemplateDocument2 pagini3 - Aac - Mini Project - Report Templateosama4717Încă nu există evaluări

- Summarization of Text Based On Deep Neural NetworkDocument12 paginiSummarization of Text Based On Deep Neural NetworkIJRASETPublicationsÎncă nu există evaluări

- Instructions For Taking The ITEP Practice Test 22DEC16 1Document3 paginiInstructions For Taking The ITEP Practice Test 22DEC16 1Tony Espinosa AtocheÎncă nu există evaluări

- Methods For Dump LSASSDocument52 paginiMethods For Dump LSASSAdani KamalÎncă nu există evaluări

- 101-RadarSea JRC JMA-5200MK2 - Brochure AM 17-7-2019Document8 pagini101-RadarSea JRC JMA-5200MK2 - Brochure AM 17-7-2019Serikhi AliÎncă nu există evaluări

- LG 47lx9500 3d Led TV Infinia TrainingDocument122 paginiLG 47lx9500 3d Led TV Infinia TrainingJan Dettlaff100% (1)

- AOA AssignmentsDocument5 paginiAOA Assignments9chand3Încă nu există evaluări

- Fusing Algorithms and Analysts Open-Source Intelligence in The Age of Big Data' in Intelligence and National SecurityDocument17 paginiFusing Algorithms and Analysts Open-Source Intelligence in The Age of Big Data' in Intelligence and National SecurityKsenija TrajkovskaÎncă nu există evaluări