S-ar putea să vă placă și

- The PAYTECH Book: The Payment Technology Handbook for Investors, Entrepreneurs, and FinTech VisionariesDe la EverandThe PAYTECH Book: The Payment Technology Handbook for Investors, Entrepreneurs, and FinTech VisionariesÎncă nu există evaluări

- The Digital Banking Revolution: How financial technology companies are rapidly transforming the traditional retail banking industry through disruptive innovation.De la EverandThe Digital Banking Revolution: How financial technology companies are rapidly transforming the traditional retail banking industry through disruptive innovation.Încă nu există evaluări

- Data Privacy Fintech A Complete Guide - 2021 EditionDe la EverandData Privacy Fintech A Complete Guide - 2021 EditionÎncă nu există evaluări

- Banking As A Service A Complete Guide - 2020 EditionDe la EverandBanking As A Service A Complete Guide - 2020 EditionÎncă nu există evaluări

- Core Banking System A Complete Guide - 2019 EditionDe la EverandCore Banking System A Complete Guide - 2019 EditionÎncă nu există evaluări

- Core Banking System Strategy A Complete Guide - 2020 EditionDe la EverandCore Banking System Strategy A Complete Guide - 2020 EditionÎncă nu există evaluări

- Core Banking System A Complete Guide - 2020 EditionDe la EverandCore Banking System A Complete Guide - 2020 EditionÎncă nu există evaluări

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersDe la EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersÎncă nu există evaluări

- E Payment Gateway A Complete Guide - 2020 EditionDe la EverandE Payment Gateway A Complete Guide - 2020 EditionÎncă nu există evaluări

- Fair Lending Compliance: Intelligence and Implications for Credit Risk ManagementDe la EverandFair Lending Compliance: Intelligence and Implications for Credit Risk ManagementÎncă nu există evaluări

- Digital Banking Platform A Complete Guide - 2021 EditionDe la EverandDigital Banking Platform A Complete Guide - 2021 EditionÎncă nu există evaluări

- Blockchain Consortium The Ultimate Step-By-Step GuideDe la EverandBlockchain Consortium The Ultimate Step-By-Step GuideÎncă nu există evaluări

- Bankruption: How Community Banking Can Survive FintechDe la EverandBankruption: How Community Banking Can Survive FintechEvaluare: 3 din 5 stele3/5 (1)

- E-Payment Gateway A Complete Guide - 2019 EditionDe la EverandE-Payment Gateway A Complete Guide - 2019 EditionEvaluare: 1 din 5 stele1/5 (1)

- The WEALTHTECH Book: The FinTech Handbook for Investors, Entrepreneurs and Finance VisionariesDe la EverandThe WEALTHTECH Book: The FinTech Handbook for Investors, Entrepreneurs and Finance VisionariesÎncă nu există evaluări

- Payment card industry A Complete Guide - 2019 EditionDe la EverandPayment card industry A Complete Guide - 2019 EditionÎncă nu există evaluări

- Credit Card Fraud Prevention Strategies A Complete Guide - 2021 EditionDe la EverandCredit Card Fraud Prevention Strategies A Complete Guide - 2021 EditionÎncă nu există evaluări

- Regulatory Technology A Complete Guide - 2021 EditionDe la EverandRegulatory Technology A Complete Guide - 2021 EditionÎncă nu există evaluări

- Demystifying Digital Lending PDFDocument44 paginiDemystifying Digital Lending PDFHitesh DhaddhaÎncă nu există evaluări

- API Monetization A Complete Guide - 2020 EditionDe la EverandAPI Monetization A Complete Guide - 2020 EditionÎncă nu există evaluări

- Embedded Finance: When Payments Become An ExperienceDe la EverandEmbedded Finance: When Payments Become An ExperienceÎncă nu există evaluări

- Methods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeDe la EverandMethods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeÎncă nu există evaluări

- Payment Gateway A Complete Guide - 2020 EditionDe la EverandPayment Gateway A Complete Guide - 2020 EditionEvaluare: 4 din 5 stele4/5 (2)

- Electronic Financial Services: Technology and ManagementDe la EverandElectronic Financial Services: Technology and ManagementEvaluare: 5 din 5 stele5/5 (1)

- Blockchain in e-Governance: Driving the next Frontier in G2C Services (English Edition)De la EverandBlockchain in e-Governance: Driving the next Frontier in G2C Services (English Edition)Încă nu există evaluări

- Open BankingDocument8 paginiOpen BankingAadithyan T GÎncă nu există evaluări

- Digital Fix - Fix Digital: How to renew the digital world from the ground upDe la EverandDigital Fix - Fix Digital: How to renew the digital world from the ground upÎncă nu există evaluări

- Capgemini - World Payments Report 2013Document60 paginiCapgemini - World Payments Report 2013Carlo Di Domenico100% (1)

- The Rise of Artificial Intelligence: Real-world Applications for Revenue and Margin GrowthDe la EverandThe Rise of Artificial Intelligence: Real-world Applications for Revenue and Margin GrowthÎncă nu există evaluări

- Export Credit Insurance and Guarantees: A Practitioner's GuideDe la EverandExport Credit Insurance and Guarantees: A Practitioner's GuideÎncă nu există evaluări

- Blockchain Business A Complete Guide - 2019 EditionDe la EverandBlockchain Business A Complete Guide - 2019 EditionÎncă nu există evaluări

- Open BankingDocument23 paginiOpen BankingJayesh BaliÎncă nu există evaluări

- Blockchain As A Service A Complete Guide - 2020 EditionDe la EverandBlockchain As A Service A Complete Guide - 2020 EditionÎncă nu există evaluări

- Payment As A Service A Complete Guide - 2020 EditionDe la EverandPayment As A Service A Complete Guide - 2020 EditionÎncă nu există evaluări

- Fintech and the Remaking of Financial InstitutionsDe la EverandFintech and the Remaking of Financial InstitutionsEvaluare: 5 din 5 stele5/5 (1)

- Middle East/Africa: Purchase Volume 2015 vs. 2014Document11 paginiMiddle East/Africa: Purchase Volume 2015 vs. 2014Charan TejaÎncă nu există evaluări

- Digital Financial Services in the Pacific: Experiences and Regulatory IssuesDe la EverandDigital Financial Services in the Pacific: Experiences and Regulatory IssuesÎncă nu există evaluări

- FinTech Rising: Navigating the maze of US & EU regulationsDe la EverandFinTech Rising: Navigating the maze of US & EU regulationsEvaluare: 5 din 5 stele5/5 (1)

- Elft Workstyles Inventory ScoringDocument2 paginiElft Workstyles Inventory Scoringdarma bonarÎncă nu există evaluări

- Daftar Alamat Kantor Pusat Bank Umum Dan Syariah Desember 2019Document12 paginiDaftar Alamat Kantor Pusat Bank Umum Dan Syariah Desember 2019sales manxi0% (1)

- Profitable Growth Will Define Success: The New World of Virtual BanksDocument1 paginăProfitable Growth Will Define Success: The New World of Virtual Banksdarma bonarÎncă nu există evaluări

- Bankreport-Laporan-Neraca-Juni-2019-219 SulutGoDocument1 paginăBankreport-Laporan-Neraca-Juni-2019-219 SulutGodarma bonarÎncă nu există evaluări

- 2019-07-29 - LKTT JUNI 2019-2 VictoriaDocument149 pagini2019-07-29 - LKTT JUNI 2019-2 Victoriadarma bonarÎncă nu există evaluări

- Designing A Customer Service Strategy: SEEP Annual Meeting & Workshops 23 October 2003Document11 paginiDesigning A Customer Service Strategy: SEEP Annual Meeting & Workshops 23 October 2003Kuldeep BishtÎncă nu există evaluări

- Contoh Action Plan Penerapan - English VersionDocument2 paginiContoh Action Plan Penerapan - English VersionDiah NurJulianaÎncă nu există evaluări

- Rating Asset Bank Q2-2019Document11 paginiRating Asset Bank Q2-2019darma bonarÎncă nu există evaluări

- Direktori Fintech Juni 2019Document24 paginiDirektori Fintech Juni 2019Adam BasrinduÎncă nu există evaluări

- Working Styles Characteristics: A - Analytical B - DriverDocument2 paginiWorking Styles Characteristics: A - Analytical B - Driverdarma bonarÎncă nu există evaluări

- 1-Jan 1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-AugDocument41 pagini1-Jan 1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-Augdarma bonarÎncă nu există evaluări

- Bank Jtrust Indonesia Vendor Evaluation Form: Kreteria Rating Komentar (1 2 3 4 5)Document2 paginiBank Jtrust Indonesia Vendor Evaluation Form: Kreteria Rating Komentar (1 2 3 4 5)darma bonarÎncă nu există evaluări

- Tabel1 17Document30 paginiTabel1 17Soesiadhy PalimbuÎncă nu există evaluări

- I.24 Posisi Simpanan Berjangka Bank Umum Dan BPR Menurut Jangka Waktu (Miliar RP)Document2 paginiI.24 Posisi Simpanan Berjangka Bank Umum Dan BPR Menurut Jangka Waktu (Miliar RP)Izzuddin AbdurrahmanÎncă nu există evaluări

- 1) Termasuk Modal Cadangan: Statistik Ekonomi Dan Keuangan Indonesia Bank IndonesiaDocument2 pagini1) Termasuk Modal Cadangan: Statistik Ekonomi Dan Keuangan Indonesia Bank Indonesiadarma bonarÎncă nu există evaluări

- I.37. Posisi Deposito Berjangka Pada Seluruh Bank Menurut Penggolongan Pemilikan 1) (Miliar RP)Document33 paginiI.37. Posisi Deposito Berjangka Pada Seluruh Bank Menurut Penggolongan Pemilikan 1) (Miliar RP)darma bonarÎncă nu există evaluări

- SOC Incident Log BookDocument13 paginiSOC Incident Log Bookdarma bonarÎncă nu există evaluări

- Letter of Credit Checklist: If You Receive An L/C Please Pay Attention To Following PointsDocument2 paginiLetter of Credit Checklist: If You Receive An L/C Please Pay Attention To Following PointsJessica WardÎncă nu există evaluări

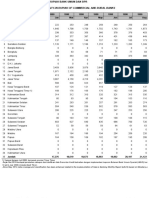

- (Billions of RP) I.20 Outstanding of Private Deposits in Rupiah of Commercial and Rural Banks by ProvincesDocument42 pagini(Billions of RP) I.20 Outstanding of Private Deposits in Rupiah of Commercial and Rural Banks by Provincesdarma bonarÎncă nu există evaluări

- Direktori LKM - Desember 2019Document239 paginiDirektori LKM - Desember 2019Darma Bonar TampubolonÎncă nu există evaluări

- AR IK 2019 - Struktur Perseroan Corporate Structure en IDDocument1 paginăAR IK 2019 - Struktur Perseroan Corporate Structure en IDdarma bonarÎncă nu există evaluări

- Ratio TreeDocument1 paginăRatio Treedarma bonarÎncă nu există evaluări

- Direktori Dana Pensiun Januari 2020Document55 paginiDirektori Dana Pensiun Januari 2020Darma Bonar Tampubolon100% (1)

- Daftar Alamat Kantor Pusat Bank Umum Dan Syariah Desember 2019Document12 paginiDaftar Alamat Kantor Pusat Bank Umum Dan Syariah Desember 2019sales manxi0% (1)

- Minutes Funding Weekly 080419Document1 paginăMinutes Funding Weekly 080419darma bonarÎncă nu există evaluări

- Direktori Perusahaan Pialang Reasuransi - Maret 2020Document8 paginiDirektori Perusahaan Pialang Reasuransi - Maret 2020darma bonarÎncă nu există evaluări

- Outlets EChannelDocument1 paginăOutlets EChanneldarma bonarÎncă nu există evaluări

- Mom 01112018Document1 paginăMom 01112018darma bonarÎncă nu există evaluări

- Tabel1 10Document4 paginiTabel1 10ali jabarÎncă nu există evaluări

- BCP Template 2012Document58 paginiBCP Template 2012Amirul IqbalÎncă nu există evaluări

- Marketing Plan On PepsicoDocument24 paginiMarketing Plan On PepsicoWaqar AfzaalÎncă nu există evaluări

- Damac Inventorydetail Clone PDFDocument4 paginiDamac Inventorydetail Clone PDFAnonymous 2rYmgRÎncă nu există evaluări

- ODI Administration and Development OutlineDocument7 paginiODI Administration and Development OutlinerameshibmÎncă nu există evaluări

- PAT Ch1 - Eurotech V CuizonDocument1 paginăPAT Ch1 - Eurotech V CuizonAlthea M. SuerteÎncă nu există evaluări

- Rule 16 (Motion To Dismiss)Document36 paginiRule 16 (Motion To Dismiss)Eunice SaavedraÎncă nu există evaluări

- Cason Company Profile Eng 2011Document11 paginiCason Company Profile Eng 2011Mercedesz TrumÎncă nu există evaluări

- Vernon Paltoo - TIC-Melamine Workshop June 1230hrsDocument54 paginiVernon Paltoo - TIC-Melamine Workshop June 1230hrsRajendra VegadÎncă nu există evaluări

- CFO VP Finance Project Controls Engineer in Morristown NJ Resume Matthew GentileDocument2 paginiCFO VP Finance Project Controls Engineer in Morristown NJ Resume Matthew GentileMatthewGentileÎncă nu există evaluări

- Kertas Tugasan: (Assignment Sheet)Document5 paginiKertas Tugasan: (Assignment Sheet)Danish HasanahÎncă nu există evaluări

- Rousselot Gelatine: Dedicated To Your SuccessDocument28 paginiRousselot Gelatine: Dedicated To Your SuccessChristopher RiveroÎncă nu există evaluări

- Public ManagementDocument1 paginăPublic ManagementDr. Syed Saqlain RazaÎncă nu există evaluări

- 2.SK EO SK Inventory SK Pob. Zone 3Document3 pagini2.SK EO SK Inventory SK Pob. Zone 3Barangay BotongonÎncă nu există evaluări

- Encyclopaedia Britannica vs. NLRCDocument1 paginăEncyclopaedia Britannica vs. NLRCYsabel PadillaÎncă nu există evaluări

- True-False Perfect CompetitionTrue-false Perfect CompetitionDocument37 paginiTrue-False Perfect CompetitionTrue-false Perfect CompetitionVlad Guzunov50% (2)

- Literature ReviewDocument6 paginiLiterature Reviewanon_230550501Încă nu există evaluări

- Tutorial 3 QN 3Document2 paginiTutorial 3 QN 3Rias SahulÎncă nu există evaluări

- Dear SirDocument2 paginiDear SircaressaÎncă nu există evaluări

- Certif I CteDocument13 paginiCertif I CteJoielyn Dy DimaanoÎncă nu există evaluări

- Unit 7 Test. 1 Complete The Sentences With A Word From The BoxDocument2 paginiUnit 7 Test. 1 Complete The Sentences With A Word From The BoxGleb ParkÎncă nu există evaluări

- 2.05 CTQC DetailsDocument3 pagini2.05 CTQC DetailsJawaid IqbalÎncă nu există evaluări

- University of Madras: B.Sc. (Ism) and Bcom. (Informationsystemsmanagement) Degree Examinations, April 2014Document6 paginiUniversity of Madras: B.Sc. (Ism) and Bcom. (Informationsystemsmanagement) Degree Examinations, April 2014Dolce UdayÎncă nu există evaluări

- HLB Receipt-2023-03-08Document2 paginiHLB Receipt-2023-03-08zu hairyÎncă nu există evaluări

- Solved Astrostar Inc Has A Board of Directors Consisting of Three Members PDFDocument1 paginăSolved Astrostar Inc Has A Board of Directors Consisting of Three Members PDFAnbu jaromiaÎncă nu există evaluări

- Walmart Analyst ReportDocument29 paginiWalmart Analyst ReportAlexander Mauricio BarretoÎncă nu există evaluări

- Juan Pedro Gamondés: Purchasing & Procurement ProfessionalDocument2 paginiJuan Pedro Gamondés: Purchasing & Procurement Professionaltuxedo_flyerÎncă nu există evaluări

- Types of Risk of An EntrepreneurDocument15 paginiTypes of Risk of An Entrepreneurvinayhn0783% (24)

- Acca F2 Management Accounting Mock Test Dec 2008 Prepared By: Ben LeeDocument17 paginiAcca F2 Management Accounting Mock Test Dec 2008 Prepared By: Ben Leesomica100% (4)

- DepreciationDocument35 paginiDepreciationAlexie Gonzales60% (5)

- Spread Trading Guide PDFDocument18 paginiSpread Trading Guide PDFMiguel Teixeira CouteiroÎncă nu există evaluări

- RC SCM310 ProductionOrdersDocument327 paginiRC SCM310 ProductionOrdersRRROMANCAÎncă nu există evaluări