S-ar putea să vă placă și

- Benton VRT PDFDocument134 paginiBenton VRT PDFabc123-1100% (1)

- NORSOKDocument35 paginiNORSOKSasa ZivkovicÎncă nu există evaluări

- Ca. CM: Copyrioht by Modeverlag Lutterloh MCMLXXXIIDocument2 paginiCa. CM: Copyrioht by Modeverlag Lutterloh MCMLXXXIIgtyd100% (1)

- CPM Scoring Sheet and NormDocument5 paginiCPM Scoring Sheet and NormPankhuri MishraÎncă nu există evaluări

- 14 PDFDocument8 pagini14 PDFDr. Sashibhusan MishraÎncă nu există evaluări

- Aflz P"' T'/: Krna'kDocument1 paginăAflz P"' T'/: Krna'kMayur MuradeÎncă nu există evaluări

- Darfur ThrowersDocument23 paginiDarfur ThrowersPersean LoveÎncă nu există evaluări

- Investor Problems in Capital MarketDocument33 paginiInvestor Problems in Capital MarketaswinecebeÎncă nu există evaluări

- Casebook: EditionDocument30 paginiCasebook: EditionNaura TsabitaÎncă nu există evaluări

- Naval Dockyard Mumbai Bharti 2024 For 301 Appretice PostsDocument8 paginiNaval Dockyard Mumbai Bharti 2024 For 301 Appretice Postslokmudragroup37Încă nu există evaluări

- Microscale Inorganic Chemistry - A Comprehensive Laboratory Experience - Szafran, ZviDocument392 paginiMicroscale Inorganic Chemistry - A Comprehensive Laboratory Experience - Szafran, ZviJade Fromage79% (14)

- 1958 Gov Gazette Pretoria, 10dec1958 - Vol - CLXVII No.2741Document40 pagini1958 Gov Gazette Pretoria, 10dec1958 - Vol - CLXVII No.2741nix111Încă nu există evaluări

- ........ - FTLLLLL: Liii.iDocument1 pagină........ - FTLLLLL: Liii.isamelÎncă nu există evaluări

- Shop Manual D 85SSDocument1 paginăShop Manual D 85SSsigit prihantoÎncă nu există evaluări

- PN008098 eDocument9 paginiPN008098 eSangita BawareÎncă nu există evaluări

- Zlatni Kroj: 40xgocm 26oxgocmDocument2 paginiZlatni Kroj: 40xgocm 26oxgocmgtyd100% (2)

- Itp WMMDocument3 paginiItp WMMRitesh kumarÎncă nu există evaluări

- Civit: IN Engineering ! YearDocument28 paginiCivit: IN Engineering ! YearVivek S. Suryawanshi-PatilÎncă nu există evaluări

- Financial Accounting 2Document421 paginiFinancial Accounting 2Charlz BanksÎncă nu există evaluări

- Centenia: Certified CompanDocument14 paginiCentenia: Certified CompanContra Value BetsÎncă nu există evaluări

- Tabla 5B APIDocument24 paginiTabla 5B APIJhonatan Perez RamirezÎncă nu există evaluări

- Marketing Slides - Prof Hooi Den Huan - 31 May 2016Document80 paginiMarketing Slides - Prof Hooi Den Huan - 31 May 2016Heru LimÎncă nu există evaluări

- Present UtilityDocument1 paginăPresent UtilityrashedÎncă nu există evaluări

- Ts Asuka JiipeDocument1 paginăTs Asuka Jiipeamir bahrudinÎncă nu există evaluări

- Tommy Emmanuel Avalon Caas 2009 PDFDocument5 paginiTommy Emmanuel Avalon Caas 2009 PDFRaúl HernánÎncă nu există evaluări

- SL NO.9 (Illupakadu Kuttai)Document2 paginiSL NO.9 (Illupakadu Kuttai)kkodgeÎncă nu există evaluări

- Manifiesto B014-2022 RAN 09-Nov-22 PDFDocument3 paginiManifiesto B014-2022 RAN 09-Nov-22 PDFMiguel BarriosÎncă nu există evaluări

- Work Together 6-1 6-2 6-3Document1 paginăWork Together 6-1 6-2 6-3James SargentÎncă nu există evaluări

- Pid ChlorinationDocument2 paginiPid ChlorinationShanmuganathan ShanÎncă nu există evaluări

- Business Transformation Initiative (BTI) - Supplier Collaboration Sales PackageDocument23 paginiBusiness Transformation Initiative (BTI) - Supplier Collaboration Sales Packagedivya2882Încă nu există evaluări

- Short Strangle 300 Pts Re EntryDocument32 paginiShort Strangle 300 Pts Re EntryDivyansh WayneÎncă nu există evaluări

- Bloc de Notas Sin TítuloDocument8 paginiBloc de Notas Sin TítuloVictor RodriguezÎncă nu există evaluări

- GAZ13 The Shadow Elves (Basic) (10495734)Document103 paginiGAZ13 The Shadow Elves (Basic) (10495734)xorrynhexbladeÎncă nu există evaluări

- TPDF - 2 MosdorferDocument2 paginiTPDF - 2 MosdorferLiciu CiprianÎncă nu există evaluări

- CH 1+2 AnsDocument4 paginiCH 1+2 AnshahaÎncă nu există evaluări

- JUN 2 7 1990 Operating I Service Manual: Quick StartDocument6 paginiJUN 2 7 1990 Operating I Service Manual: Quick StartFouquetÎncă nu există evaluări

- s1 w5 l4 Conic Section The HyperbolaDocument8 paginis1 w5 l4 Conic Section The Hyperbolaapi-644259218Încă nu există evaluări

- Caderno Macro 3 Un. 3Document10 paginiCaderno Macro 3 Un. 3Brunno10Încă nu există evaluări

- Bce Iii I PDFDocument27 paginiBce Iii I PDFDiwas PoudelÎncă nu există evaluări

- Platinum Notes - ENTDocument55 paginiPlatinum Notes - ENTsk100% (1)

- 21-The Agnosias - 26Document26 pagini21-The Agnosias - 26Manuela Bedoya GartnerÎncă nu există evaluări

- Document 20Document1 paginăDocument 20Goodwell MzembeÎncă nu există evaluări

- Time To Say Goodbye001Document5 paginiTime To Say Goodbye001Χρύσα ΜάγιατζηÎncă nu există evaluări

- NWPCP Icb2 As Tech 0103 ADocument1 paginăNWPCP Icb2 As Tech 0103 AAshoka Indunil WickramapalaÎncă nu există evaluări

- Public Finance and TaxationDocument341 paginiPublic Finance and TaxationkimÎncă nu există evaluări

- AD0312751(新炮的比较)Document21 paginiAD0312751(新炮的比较)114514Încă nu există evaluări

- Williams 1990 Funhouse Operations Manual November 1990 Includes Schematics OCR SearchableDocument125 paginiWilliams 1990 Funhouse Operations Manual November 1990 Includes Schematics OCR SearchableJ JÎncă nu există evaluări

- DenahDocument1 paginăDenahMuhammad MansurÎncă nu există evaluări

- Cara Cari Sizing Bushing Eye PDFDocument1 paginăCara Cari Sizing Bushing Eye PDFNanda PerdanaÎncă nu există evaluări

- GAZ13 - The Shadow ElvesDocument110 paginiGAZ13 - The Shadow ElvesPascal Leroy100% (2)

- Rhcaeta: Structural Design Calculation Sheet For Block of Duplex FOR MR & Mrs Adokiye Precious CharlesDocument17 paginiRhcaeta: Structural Design Calculation Sheet For Block of Duplex FOR MR & Mrs Adokiye Precious CharlesEze NonsoÎncă nu există evaluări

- Consignment Note No.:.: U: NOT CDocument1 paginăConsignment Note No.:.: U: NOT CS DasÎncă nu există evaluări

- For Gettinq Connection For IndustrialDocument5 paginiFor Gettinq Connection For IndustrialDrasti K ShahÎncă nu există evaluări

- Motor Starting MethodsDocument1 paginăMotor Starting MethodsAhmed Abd El WahabÎncă nu există evaluări

- Reporte de Gestion - Sso Smart Camps PeruDocument3 paginiReporte de Gestion - Sso Smart Camps PeruAbel GireÎncă nu există evaluări

- Scan 19 Dec 2022Document2 paginiScan 19 Dec 2022Noha badrÎncă nu există evaluări

- KK 016Document1 paginăKK 016Choky FhÎncă nu există evaluări

- MOBILEDocument1 paginăMOBILEEugene BokeaÎncă nu există evaluări

- Wisdom of the Elders: Native Traditions on the Northwest CoastDe la EverandWisdom of the Elders: Native Traditions on the Northwest CoastÎncă nu există evaluări

- CRM-Prof - Pravesh Oct 2019Document81 paginiCRM-Prof - Pravesh Oct 2019Ankaj AroraÎncă nu există evaluări

- Chapter-Vii: Purpose and OverviewDocument14 paginiChapter-Vii: Purpose and OverviewAnkaj AroraÎncă nu există evaluări

- CodesDocument3 paginiCodesAnkaj AroraÎncă nu există evaluări

- Marketing and Branding Strategies of Consumer Durable CompaniesDocument101 paginiMarketing and Branding Strategies of Consumer Durable CompaniesAnkaj AroraÎncă nu există evaluări

- A Project Report On Sales and Distribution of TVSDocument8 paginiA Project Report On Sales and Distribution of TVSAnkaj AroraÎncă nu există evaluări

- External Growth Strategiesclass18-20Document15 paginiExternal Growth Strategiesclass18-20Ankaj AroraÎncă nu există evaluări

- A Project Report On Sales and Distribution Strategy Of: Submitted By: Sahil Garg Roll No: 18PGDM-BHU065 Section: BDocument8 paginiA Project Report On Sales and Distribution Strategy Of: Submitted By: Sahil Garg Roll No: 18PGDM-BHU065 Section: BAnkaj AroraÎncă nu există evaluări

- External Growth Strategiesclass18-20Document15 paginiExternal Growth Strategiesclass18-20Ankaj AroraÎncă nu există evaluări

- OrganizationDocument1 paginăOrganizationAnkaj AroraÎncă nu există evaluări

- CodesDocument3 paginiCodesAnkaj AroraÎncă nu există evaluări

- Annual Report 2018 2019Document253 paginiAnnual Report 2018 2019Ankaj AroraÎncă nu există evaluări

- JD Format - IMI - ToppscholarsDocument2 paginiJD Format - IMI - ToppscholarsAnkaj AroraÎncă nu există evaluări

- Guidelines For Field Based Comprehensive Project: Post Graduate Diploma in ManagementDocument8 paginiGuidelines For Field Based Comprehensive Project: Post Graduate Diploma in ManagementAnkaj AroraÎncă nu există evaluări

- Profitability and Cost Analysis of BercosDocument1 paginăProfitability and Cost Analysis of BercosAnkaj AroraÎncă nu există evaluări

- RPG EnterpriseDocument1 paginăRPG EnterpriseAnkaj AroraÎncă nu există evaluări

- RPG EnterpriseDocument1 paginăRPG EnterpriseAnkaj AroraÎncă nu există evaluări

- Profitability and Cost Analysis of BercosDocument1 paginăProfitability and Cost Analysis of BercosAnkaj AroraÎncă nu există evaluări

- "Comparative Study On Defects and Inspection System of Woven Fabrics in Different RMG Industry in Bangladesh" 1Document17 pagini"Comparative Study On Defects and Inspection System of Woven Fabrics in Different RMG Industry in Bangladesh" 1S.m. MahasinÎncă nu există evaluări

- MyNotesOnCNBCSoFar 2016Document38 paginiMyNotesOnCNBCSoFar 2016Tony C.Încă nu există evaluări

- Breweries ListDocument15 paginiBreweries Listtuscan23Încă nu există evaluări

- BHP Billiton CaseDocument30 paginiBHP Billiton CaseMonjurul Hassan100% (2)

- The Impact of Motivation On Organizational PerformanceDocument96 paginiThe Impact of Motivation On Organizational PerformanceRandolph Ogbodu100% (2)

- Quiz 7Document3 paginiQuiz 7朱潇妤Încă nu există evaluări

- Dodi SetyawanDocument2 paginiDodi SetyawanEgao Mayukko Dina MizushimaÎncă nu există evaluări

- Real Estate Player in BangaloreDocument20 paginiReal Estate Player in BangaloreAnkit GoelÎncă nu există evaluări

- Process Planning and Cost EstimationDocument13 paginiProcess Planning and Cost EstimationsanthoshjoysÎncă nu există evaluări

- True False and MCQ Demand and Supply.Document2 paginiTrue False and MCQ Demand and Supply.Nikoleta TrudovÎncă nu există evaluări

- Maruti CaseDocument5 paginiMaruti CaseBishwadeep Purkayastha100% (1)

- Manila City - Ordinance No. 8330 s.2013Document5 paginiManila City - Ordinance No. 8330 s.2013Franco SenaÎncă nu există evaluări

- Account Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 paginiAccount Statement From 3 Nov 2020 To 3 May 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRajwinder SandhuÎncă nu există evaluări

- Barro and Grossman - A General Disequilibrium Model of Income and Employment PDFDocument12 paginiBarro and Grossman - A General Disequilibrium Model of Income and Employment PDFDouglas Fabrízzio CamargoÎncă nu există evaluări

- IB Business and Management Example CommentaryDocument24 paginiIB Business and Management Example CommentaryIB Screwed94% (33)

- VAT Registration CertificateDocument1 paginăVAT Registration Certificatelucas.saleixo88Încă nu există evaluări

- Notice of Ex Parte IEPDocument9 paginiNotice of Ex Parte IEPonell.soto653Încă nu există evaluări

- A Study On Customer Satisfaction of Honda Activa Among Customers in Changanacherry TalukDocument55 paginiA Study On Customer Satisfaction of Honda Activa Among Customers in Changanacherry TalukgunÎncă nu există evaluări

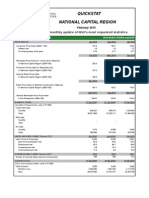

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocument3 paginiQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiÎncă nu există evaluări

- Journal of Rock Mechanics and Geotechnical EngineeringDocument13 paginiJournal of Rock Mechanics and Geotechnical EngineeringMichael TiconaÎncă nu există evaluări

- 10 TPH Cil Equipment-20171022Document10 pagini10 TPH Cil Equipment-20171022KareemAmen100% (1)

- OD126193179886369000Document6 paginiOD126193179886369000Refill positivityÎncă nu există evaluări

- Plan Contable EmpresarialDocument432 paginiPlan Contable EmpresarialJhamil Nirek PascasioÎncă nu există evaluări

- To Sell or Scale Up: Canada's Patent Strategy in A Knowledge EconomyDocument22 paginiTo Sell or Scale Up: Canada's Patent Strategy in A Knowledge EconomyInstitute for Research on Public Policy (IRPP)Încă nu există evaluări

- Seedling Trays Developed by Kal-KarDocument2 paginiSeedling Trays Developed by Kal-KarIsrael ExporterÎncă nu există evaluări

- Grammar Vocabulary 1star Unit7 PDFDocument1 paginăGrammar Vocabulary 1star Unit7 PDFLorenaAbreuÎncă nu există evaluări

- Mind Map Cost of ProductionDocument1 paginăMind Map Cost of ProductionDimas Mahendra P BozerÎncă nu există evaluări

- Acctg 1 PS 1Document3 paginiAcctg 1 PS 1Aj GuanzonÎncă nu există evaluări

- 1 Plastics Give A Helpful HandDocument10 pagini1 Plastics Give A Helpful HandNIranjanaÎncă nu există evaluări

- Methods To Initiate Ventures: Leoncio, Ma. Aira Grabrielle R. Mamigo, Princess Nicole B. G12-AB126Document21 paginiMethods To Initiate Ventures: Leoncio, Ma. Aira Grabrielle R. Mamigo, Princess Nicole B. G12-AB126Precious MamigoÎncă nu există evaluări