S-ar putea să vă placă și

- Econ 313 Handout 3 Basic Economy Study MethodsDocument41 paginiEcon 313 Handout 3 Basic Economy Study MethodsKyle RagasÎncă nu există evaluări

- Capital Budgeting Decisions Under Uncertainity - 1 - 09 - 2019Document55 paginiCapital Budgeting Decisions Under Uncertainity - 1 - 09 - 2019Kaushik meridianÎncă nu există evaluări

- Select the most profitable capital investment alternativeDocument24 paginiSelect the most profitable capital investment alternativeDave DespabiladerasÎncă nu există evaluări

- Capital BudgetingDocument8 paginiCapital BudgetingYash PatilÎncă nu există evaluări

- Unit 5 - Single Project EvaluationDocument38 paginiUnit 5 - Single Project EvaluationAadeem NyaichyaiÎncă nu există evaluări

- Techniques of Investment AnalysisDocument32 paginiTechniques of Investment AnalysisPranjal Verma0% (1)

- Topic IV - Economic Study MethodsDocument13 paginiTopic IV - Economic Study MethodsMc John PobleteÎncă nu există evaluări

- MAS Handout - Capital BudgetingDocument7 paginiMAS Handout - Capital BudgetingDivine VictoriaÎncă nu există evaluări

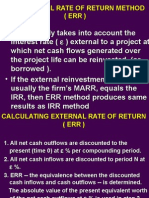

- CALCULATE EXTERNAL RATE OF RETURN (ERRDocument19 paginiCALCULATE EXTERNAL RATE OF RETURN (ERRJomer GiraoÎncă nu există evaluări

- 5 Evaluating A Single ProjectDocument32 pagini5 Evaluating A Single ProjectImie CamachoÎncă nu există evaluări

- Topic 8Document16 paginiTopic 8SUREINTHARAAN A/L NATHAN / UPMÎncă nu există evaluări

- NPV Vs - IRRDocument6 paginiNPV Vs - IRRDibakar DasÎncă nu există evaluări

- Annual Worth Method Determines Project FeasibilityDocument4 paginiAnnual Worth Method Determines Project Feasibilityraymond moscosoÎncă nu există evaluări

- Unit 4 - CEPDEDocument71 paginiUnit 4 - CEPDEsrinu02062Încă nu există evaluări

- Engineering Economics MethodsDocument44 paginiEngineering Economics MethodsCharles DemaalaÎncă nu există evaluări

- Chapter 3Document173 paginiChapter 3Maria HafeezÎncă nu există evaluări

- Financial Management Basics Capital BudgetingDocument14 paginiFinancial Management Basics Capital BudgetingVandana KaushikÎncă nu există evaluări

- FM Mod II-2Document10 paginiFM Mod II-2Irfanu NisaÎncă nu există evaluări

- Nature of Investment Decisions: Capital Budgeting, or Capital Expenditure DecisionsDocument49 paginiNature of Investment Decisions: Capital Budgeting, or Capital Expenditure DecisionsRam Krishna Krish100% (2)

- Ques No 1-Difference Between NVP and IRR?: What Is Capital Budgeting?Document4 paginiQues No 1-Difference Between NVP and IRR?: What Is Capital Budgeting?Istiaque AhmedÎncă nu există evaluări

- Ques No 1-Difference Between NVP and IRR?: What Is Capital Budgeting?Document4 paginiQues No 1-Difference Between NVP and IRR?: What Is Capital Budgeting?Istiaque AhmedÎncă nu există evaluări

- Capital Budgeting Methods and Techniques GuideDocument3 paginiCapital Budgeting Methods and Techniques Guidepratibha2031Încă nu există evaluări

- Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm'sDocument4 paginiCapital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm'spavanbhatÎncă nu există evaluări

- Unit 6 - Comparison and Selection Among AlternativesDocument51 paginiUnit 6 - Comparison and Selection Among AlternativesAadeem NyaichyaiÎncă nu există evaluări

- Chapter 02 Investment AppraisalDocument3 paginiChapter 02 Investment AppraisalMarzuka Akter KhanÎncă nu există evaluări

- Main Project Capital Budgeting MbaDocument110 paginiMain Project Capital Budgeting MbaRaviKiran Avula65% (34)

- TVM Concepts ExplainedDocument4 paginiTVM Concepts ExplainedMark AlderiteÎncă nu există evaluări

- Capital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm's Long TermDocument4 paginiCapital Budgeting (Or Investment Appraisal) Is The Planning Process Used To Determine Whether A Firm's Long TermAshish Kumar100% (2)

- Evaluating A Single ProjectDocument31 paginiEvaluating A Single ProjectDave Despabiladeras50% (2)

- Comparing Alternatives, S6Document38 paginiComparing Alternatives, S6RONALD LUIS D. BOQUIRENÎncă nu există evaluări

- Techniques of Capital BudgetingDocument20 paginiTechniques of Capital Budgetinggoogle BabaÎncă nu există evaluări

- Unit 2Document5 paginiUnit 2Aditya GuptaÎncă nu există evaluări

- Unit 4Document11 paginiUnit 4ajinkyapolÎncă nu există evaluări

- Engineering Economy 2Document73 paginiEngineering Economy 2MD Al-AminÎncă nu există evaluări

- Project Appraisal TechniquesDocument30 paginiProject Appraisal TechniquesvidhiÎncă nu există evaluări

- Financial Evaluation of LEASINGDocument7 paginiFinancial Evaluation of LEASINGmba departmentÎncă nu există evaluări

- Selecting the Best Capital Investment AlternativeDocument30 paginiSelecting the Best Capital Investment AlternativeImie CamachoÎncă nu există evaluări

- Eee221 9Document25 paginiEee221 9Zoloft Zithromax ProzacÎncă nu există evaluări

- International Capital Budgeting ExplainedDocument18 paginiInternational Capital Budgeting ExplainedHitesh Kumar100% (1)

- CH-2 RivewDocument57 paginiCH-2 RivewMulugeta DefaruÎncă nu există evaluări

- CH 08 Capital BudgetingDocument51 paginiCH 08 Capital BudgetingLitika SachdevaÎncă nu există evaluări

- Capital Iq MaterialDocument38 paginiCapital Iq MaterialMadan MohanÎncă nu există evaluări

- CB 1Document3 paginiCB 1Shreyas KothiÎncă nu există evaluări

- ProfitabilityDocument12 paginiProfitabilityAbdullah RamzanÎncă nu există evaluări

- Capital BudgetingDocument35 paginiCapital BudgetingShivam Goel100% (1)

- Capital Budgeting: Navigation SearchDocument16 paginiCapital Budgeting: Navigation SearchVenkat Narayana ReddyÎncă nu există evaluări

- MAS - Capital BudgetingDocument7 paginiMAS - Capital BudgetingJohn Mahatma AgripaÎncă nu există evaluări

- Internal Rate of ReturnDocument16 paginiInternal Rate of ReturnAnnalie Alsado BustilloÎncă nu există evaluări

- Capital BudgetingDocument3 paginiCapital Budgetinganandh30Încă nu există evaluări

- Methods of Comparing Alternative ProposalsDocument67 paginiMethods of Comparing Alternative Proposalsrobel pop50% (2)

- Madras University MBA Managerial Economics PMBSE NotesDocument11 paginiMadras University MBA Managerial Economics PMBSE NotesCircut100% (1)

- ProfitabilityDocument36 paginiProfitabilityShronik PatelÎncă nu există evaluări

- 03 - 20th Aug Capital Budgeting, 2019Document37 pagini03 - 20th Aug Capital Budgeting, 2019anujÎncă nu există evaluări

- Profitability AnalysisDocument43 paginiProfitability AnalysisAvinash Iyer100% (1)

- Internal Rate of ReturnDocument28 paginiInternal Rate of ReturnVaidyanathan Ravichandran100% (1)

- Capital Budgeting-Theory and NumericalsDocument47 paginiCapital Budgeting-Theory and Numericalssaadsaaid50% (2)

- Financial ManagementDocument20 paginiFinancial ManagementGAURAV SHARMA100% (1)

- Capital BudgetingDocument22 paginiCapital BudgetingRajatÎncă nu există evaluări

- Applied Corporate Finance. What is a Company worth?De la EverandApplied Corporate Finance. What is a Company worth?Evaluare: 3 din 5 stele3/5 (2)

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisDe la EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisÎncă nu există evaluări

- Tocardo Turbin1Document2 paginiTocardo Turbin1sanjog kshetriÎncă nu există evaluări

- X-Ray Production by Coolidge MethodDocument8 paginiX-Ray Production by Coolidge Methodsanjog kshetriÎncă nu există evaluări

- Speed Developing Practice Test No. 5: Alphabet AnalogyDocument2 paginiSpeed Developing Practice Test No. 5: Alphabet Analogysanjog kshetriÎncă nu există evaluări

- Unit A-2 3Document39 paginiUnit A-2 3sanjog kshetriÎncă nu există evaluări

- Biomolecules: Carbs, Lipids, Proteins & Nucleic AcidsDocument19 paginiBiomolecules: Carbs, Lipids, Proteins & Nucleic Acidssanjog kshetriÎncă nu există evaluări

- BTY223 Quizz 1 Set 1,2 3 With AnswersDocument13 paginiBTY223 Quizz 1 Set 1,2 3 With Answerssanjog kshetriÎncă nu există evaluări

- Unit A-1Document24 paginiUnit A-1sanjog kshetriÎncă nu există evaluări

- Lecture 6Document10 paginiLecture 6sanjog kshetriÎncă nu există evaluări

- Class Assignment For 16 Oct 10 MarksDocument2 paginiClass Assignment For 16 Oct 10 Markssanjog kshetriÎncă nu există evaluări

- Lecture 4Document46 paginiLecture 4sanjog kshetriÎncă nu există evaluări

- BTY223 Quizz 1 Set 1,2 3 With AnswersDocument13 paginiBTY223 Quizz 1 Set 1,2 3 With Answerssanjog kshetriÎncă nu există evaluări

- Unit A-1Document24 paginiUnit A-1sanjog kshetriÎncă nu există evaluări

- Construction Cost Analysis and Finances: Time Value of MoneyDocument29 paginiConstruction Cost Analysis and Finances: Time Value of Moneysanjog kshetriÎncă nu există evaluări

- NPTEL Construction Economics & Finance Module 6 Lecture 1Document23 paginiNPTEL Construction Economics & Finance Module 6 Lecture 1Saurabh Kumar SharmaÎncă nu există evaluări

- Windows ActivateDocument2 paginiWindows Activatesanjog kshetriÎncă nu există evaluări

- L-T-P: 3-1-0, Credit: 4Document1 paginăL-T-P: 3-1-0, Credit: 4sanjog kshetriÎncă nu există evaluări

- Working Capital Management for Construction ProjectsDocument10 paginiWorking Capital Management for Construction Projectssanjog kshetriÎncă nu există evaluări

- 2 Comparision of AlternativesDocument107 pagini2 Comparision of AlternativesXman ManÎncă nu există evaluări

- Tabel Tingkat Suku BungaDocument32 paginiTabel Tingkat Suku BungaFhadjroel AntekÎncă nu există evaluări

- Example of Cost AnalysisDocument1 paginăExample of Cost Analysissanjog kshetriÎncă nu există evaluări

- Introduction of Construction Cost and FinanceDocument12 paginiIntroduction of Construction Cost and Financesanjog kshetriÎncă nu există evaluări

- Time ValueDocument33 paginiTime ValueChintan TrivediÎncă nu există evaluări

- Comparision of AlternativesDocument13 paginiComparision of Alternativessanjog kshetriÎncă nu există evaluări

- 1 Semister SillabsDocument4 pagini1 Semister Sillabssanjog kshetriÎncă nu există evaluări

- Assignment - 2Document1 paginăAssignment - 2sanjog kshetriÎncă nu există evaluări

- Math II Assignment SolutionsDocument1 paginăMath II Assignment Solutionssanjog kshetriÎncă nu există evaluări

- CVL829-Analysis of Construction Cost and Finances: Assignment - 1Document1 paginăCVL829-Analysis of Construction Cost and Finances: Assignment - 1sanjog kshetriÎncă nu există evaluări

- Lab ExperimentsDocument9 paginiLab Experimentssanjog kshetriÎncă nu există evaluări

- ElasticityDocument19 paginiElasticitysanjog kshetriÎncă nu există evaluări

- IFRIC 13 - Customer Loyalty ProgrammesDocument8 paginiIFRIC 13 - Customer Loyalty ProgrammesTopy DajayÎncă nu există evaluări

- Bank loan allowance provisionsDocument3 paginiBank loan allowance provisionsJudith CastroÎncă nu există evaluări

- India's Coastal Regulation Zone Notification: A Critical AnalysisDocument69 paginiIndia's Coastal Regulation Zone Notification: A Critical Analysisajaythakur11Încă nu există evaluări

- Black Soldier Fly larvae reduce vegetable waste up to 74Document11 paginiBlack Soldier Fly larvae reduce vegetable waste up to 74Firman Nugraha100% (1)

- 9 Main Differences Between Managerial Economics and Traditional EconomicsDocument4 pagini9 Main Differences Between Managerial Economics and Traditional EconomicsDeepak KumarÎncă nu există evaluări

- Leading Wheel Manufacturer Commercial InvoiceDocument2 paginiLeading Wheel Manufacturer Commercial Invoiceadi kristianÎncă nu există evaluări

- View Property Tax Details for Ex-Service ManDocument3 paginiView Property Tax Details for Ex-Service ManAMALAADIÎncă nu există evaluări

- ICBC Presentation 09Document24 paginiICBC Presentation 09AhmadÎncă nu există evaluări

- House Hearing, 112TH Congress - Sitting On Our Assets: The Cotton AnnexDocument41 paginiHouse Hearing, 112TH Congress - Sitting On Our Assets: The Cotton AnnexScribd Government DocsÎncă nu există evaluări

- The Fdi Report 2013Document20 paginiThe Fdi Report 2013Ramsey RaulÎncă nu există evaluări

- Management Control of Non-Profit Organisations: DR P K Vasudeva 1Document7 paginiManagement Control of Non-Profit Organisations: DR P K Vasudeva 1sunnysiÎncă nu există evaluări

- Global Electric Power Steering (EPS) Market Analysis and Forecast (2013 - 2018)Document15 paginiGlobal Electric Power Steering (EPS) Market Analysis and Forecast (2013 - 2018)Sanjay MatthewsÎncă nu există evaluări

- Tradingfxhub Com Blog How To Identify Supply and Demand CurveDocument15 paginiTradingfxhub Com Blog How To Identify Supply and Demand CurveKrunal ParabÎncă nu există evaluări

- River Bank Erosion in BangladeshDocument14 paginiRiver Bank Erosion in BangladeshSanjida ShoumitÎncă nu există evaluări

- 5 Year Financial Projections for Capital, Borrowings, Income & ExpensesDocument2 pagini5 Year Financial Projections for Capital, Borrowings, Income & ExpensesCedric JohnsonÎncă nu există evaluări

- Project On Axis BankDocument36 paginiProject On Axis Bankratandeepjain86% (7)

- Cottle-Taylor: Expanding The Oral Care Group in IndiaDocument18 paginiCottle-Taylor: Expanding The Oral Care Group in IndiaManav LakhinaÎncă nu există evaluări

- 25 Most Influential Business Leaders in The PhilippinesDocument8 pagini25 Most Influential Business Leaders in The PhilippinesJon GraniadaÎncă nu există evaluări

- Cost Concepts in EconomicsDocument18 paginiCost Concepts in EconomicsHimaani ShahÎncă nu există evaluări

- A-19 BSBA Operations MGTDocument2 paginiA-19 BSBA Operations MGTEnteng NiezÎncă nu există evaluări

- 1st Year 1sem 2019-20Document2 pagini1st Year 1sem 2019-20Kuldeep MalÎncă nu există evaluări

- Boat Rockerz 255F Bluetooth Headset: Grand Total 1199.00Document3 paginiBoat Rockerz 255F Bluetooth Headset: Grand Total 1199.00Spy HanÎncă nu există evaluări

- MutiaraVille New PhaseDocument20 paginiMutiaraVille New PhaseBernard LowÎncă nu există evaluări

- January Postpay BillDocument4 paginiJanuary Postpay BillestrobetceoÎncă nu există evaluări

- Copper Mining and Women's Role in Zambia's Miners' StrugglesDocument11 paginiCopper Mining and Women's Role in Zambia's Miners' StrugglesBoris PichlerbuaÎncă nu există evaluări

- The Indian Aviation SectorDocument48 paginiThe Indian Aviation SectorRajaÎncă nu există evaluări

- Individual Income Tax ComputationDocument19 paginiIndividual Income Tax ComputationShane Sigua-Salcedo100% (2)

- 2022 Term 2 JC 2 H1 Economics SOW (Final) - Students'Document5 pagini2022 Term 2 JC 2 H1 Economics SOW (Final) - Students'PROgamer GTÎncă nu există evaluări

- Sustainable DevelopmentDocument15 paginiSustainable DevelopmentKhondokar Sabera HamidÎncă nu există evaluări

- Contemporary World Lesson 11Document5 paginiContemporary World Lesson 11Ellaine De la PazÎncă nu există evaluări