S-ar putea să vă placă și

- Audit of HospitalDocument27 paginiAudit of HospitalKunal Kapoor67% (3)

- Branches of AccountingDocument7 paginiBranches of AccountingMay Angelica TenezaÎncă nu există evaluări

- Conceptual Framework of AccountingDocument29 paginiConceptual Framework of AccountingAllen Darryl Valmoria100% (1)

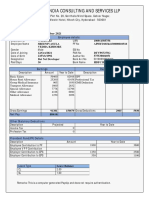

- Purview India Consulting and Services LLPDocument1 paginăPurview India Consulting and Services LLPmamatha vemulaÎncă nu există evaluări

- Audit of Hospital - Mcom Part II ProjectDocument28 paginiAudit of Hospital - Mcom Part II ProjectKunal KapoorÎncă nu există evaluări

- Process Safety Leadership Engaging With Senior ManagersDocument26 paginiProcess Safety Leadership Engaging With Senior Managerssl1828Încă nu există evaluări

- Chartered AccountantDocument33 paginiChartered AccountantSandeep Soni0% (1)

- Management AccountingDocument10 paginiManagement AccountingMohammad Fayez UddinÎncă nu există evaluări

- Quit Claim For EmployeesDocument2 paginiQuit Claim For Employeesmother material100% (1)

- SA8000 Standard 2014Document16 paginiSA8000 Standard 2014Enrique Navarrete Morales100% (2)

- Accounts 1Document14 paginiAccounts 1Piyush PatelÎncă nu există evaluări

- Ethics in AccountingDocument5 paginiEthics in Accountingxaraprotocol100% (1)

- Week 13 - Local Government (Ra 7160) and DecentralizationDocument4 paginiWeek 13 - Local Government (Ra 7160) and DecentralizationElaina JoyÎncă nu există evaluări

- How to Audit Your Account without Hiring an AuditorDe la EverandHow to Audit Your Account without Hiring an AuditorÎncă nu există evaluări

- AD9 Go-CommunityEvac Center ProposalDocument25 paginiAD9 Go-CommunityEvac Center ProposalDanielle Go100% (1)

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersDe la EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersÎncă nu există evaluări

- Factories and Machinery (Noise Exposure) Regulations, 1989 Ve - Pua1 - 1989Document15 paginiFactories and Machinery (Noise Exposure) Regulations, 1989 Ve - Pua1 - 1989Exsan OthmanÎncă nu există evaluări

- Accounting AuditorDocument2 paginiAccounting AuditorRambhupalReddyÎncă nu există evaluări

- Chapter IDocument14 paginiChapter ISugunasugiÎncă nu există evaluări

- AccountantsDocument2 paginiAccountantsJoann Saballero HamiliÎncă nu există evaluări

- Accountants and Auditors? ? ?? ? ? ?? ? ? ??Document7 paginiAccountants and Auditors? ? ?? ? ? ?? ? ? ??Hubert RamirezÎncă nu există evaluări

- Nature of The WorkDocument3 paginiNature of The WorkMax TanÎncă nu există evaluări

- Chapter 3Document6 paginiChapter 3Clarisse AnnÎncă nu există evaluări

- The Work Environment For Most Accountants and Auditors Is A Typical Office SettingDocument9 paginiThe Work Environment For Most Accountants and Auditors Is A Typical Office SettingRyan DemarsÎncă nu există evaluări

- Chartered Accountant Career DescriptionDocument2 paginiChartered Accountant Career DescriptionSKANSSialkotÎncă nu există evaluări

- Accounting and AuditingDocument7 paginiAccounting and AuditingShaibu AlhassanÎncă nu există evaluări

- Abm Lesson 1aDocument4 paginiAbm Lesson 1aAgri BasketÎncă nu există evaluări

- Quantitative InformationDocument7 paginiQuantitative InformationMagongcar hadjialiÎncă nu există evaluări

- Audit ProjectDocument23 paginiAudit ProjectPriyanka KhotÎncă nu există evaluări

- Auditing & Taxation (Chapter 1)Document9 paginiAuditing & Taxation (Chapter 1)ponyking86Încă nu există evaluări

- Accountants and Auditors: Significant PointsDocument5 paginiAccountants and Auditors: Significant Pointspagalguy1983Încă nu există evaluări

- Careers in Internal AuditingDocument5 paginiCareers in Internal Auditingtanmay agrawalÎncă nu există evaluări

- Af101 - Extra NotesDocument4 paginiAf101 - Extra Noteskaveet kavitesh kumarÎncă nu există evaluări

- Auditors: Job DescriptionDocument4 paginiAuditors: Job DescriptionChristina ImanuelÎncă nu există evaluări

- Accounting Assignment - Saad Imran LO4Document38 paginiAccounting Assignment - Saad Imran LO4Saad ImranÎncă nu există evaluări

- Auditing Chapter 1Document12 paginiAuditing Chapter 1JewelÎncă nu există evaluări

- Accounting Job TitlesDocument16 paginiAccounting Job Titlesbryan sumookÎncă nu există evaluări

- Auditing Assignment Task 4Document7 paginiAuditing Assignment Task 4Naushal SachaniyaÎncă nu există evaluări

- Esay B.inggris yDocument8 paginiEsay B.inggris yluh.Astika PramestyÎncă nu există evaluări

- Accounting - Saad Imran..Document26 paginiAccounting - Saad Imran..Saad ImranÎncă nu există evaluări

- Unethical Accounting Practices Not Only Cause Instability in The MarketDocument12 paginiUnethical Accounting Practices Not Only Cause Instability in The MarketGada AbdulcaderÎncă nu există evaluări

- Mid Term Exam-Auditing IDocument5 paginiMid Term Exam-Auditing IAmara PrabasariÎncă nu există evaluări

- Class 5 Accounting JobsDocument10 paginiClass 5 Accounting JobsJEFFERSON WILFREDO DE LEÓN CRUZÎncă nu există evaluări

- Similarities Between Management AccountingDocument3 paginiSimilarities Between Management AccountingNurul 'Ain100% (4)

- Public Accounting Services and Private Accounting ServicesDocument4 paginiPublic Accounting Services and Private Accounting ServicesALYA RASYADINA POLIBANÎncă nu există evaluări

- Unit 1Document25 paginiUnit 1Dipen DhakalÎncă nu există evaluări

- Auditing NotesDocument26 paginiAuditing Notesyash soniÎncă nu există evaluări

- ACCOUNTANCYDocument7 paginiACCOUNTANCYAnne MundinaÎncă nu există evaluări

- Accountant Play in Business OperationsDocument2 paginiAccountant Play in Business OperationsSaidur Rahman ForhadÎncă nu există evaluări

- (02.1) M1 CO1 Sole Proprietorship101Document33 pagini(02.1) M1 CO1 Sole Proprietorship101John karlo TarigaÎncă nu există evaluări

- Meaning of AuditingDocument3 paginiMeaning of AuditingPuneeth HDÎncă nu există evaluări

- Accounting Vs AuditingDocument2 paginiAccounting Vs AuditingVioleta de LaraÎncă nu există evaluări

- Financial Data Management: The Role of An Accountant in The Business IndustryDocument2 paginiFinancial Data Management: The Role of An Accountant in The Business IndustryShirlyn PerezÎncă nu există evaluări

- Day 2 Finman p2Document6 paginiDay 2 Finman p2Ericka DeguzmanÎncă nu există evaluări

- What Are Accounting BranchesDocument6 paginiWhat Are Accounting BranchesGlycel Angela JacintoÎncă nu există evaluări

- Responsibilities of AuditorsDocument3 paginiResponsibilities of AuditorsGandreti JagadeeshÎncă nu există evaluări

- Controller Resume SamplesDocument4 paginiController Resume Samplesbcqvdfyg100% (2)

- Types of AuditsDocument3 paginiTypes of AuditsRhn Habib RehmanÎncă nu există evaluări

- Steps To Finding The Perfect Arthur Pratt CPADocument4 paginiSteps To Finding The Perfect Arthur Pratt CPAfotlanhbb1Încă nu există evaluări

- Types of AccountingDocument1 paginăTypes of Accountingcbtdm27vbxÎncă nu există evaluări

- Objective and General Principles Governing and Audit of Financial StatementsDocument10 paginiObjective and General Principles Governing and Audit of Financial Statementsali_zain_7Încă nu există evaluări

- ABM - FABM11 IIIa 5Document4 paginiABM - FABM11 IIIa 5Kayelle BelinoÎncă nu există evaluări

- Expanded Services of Accountants-FABM Chapter 2Document8 paginiExpanded Services of Accountants-FABM Chapter 2Jeannie Lyn Dela CruzÎncă nu există evaluări

- What Is AuditingDocument4 paginiWhat Is Auditingjoyce nacuteÎncă nu există evaluări

- The Field of AccountingDocument6 paginiThe Field of AccountingRipto AtmajaÎncă nu există evaluări

- Audit, Auditing and AuditorDocument14 paginiAudit, Auditing and Auditormehakrotra256Încă nu există evaluări

- CH 2. Types of AuditDocument7 paginiCH 2. Types of AuditChirag KashyapÎncă nu există evaluări

- PlaceDocument6 paginiPlaceaakritiÎncă nu există evaluări

- 42745HUL Enrollment Form - 2020Document7 pagini42745HUL Enrollment Form - 2020aakritiÎncă nu există evaluări

- 5f30fshortlisted Students Interview. Simpsons & Co LTD, Fi PL 2020 NoticeDocument2 pagini5f30fshortlisted Students Interview. Simpsons & Co LTD, Fi PL 2020 NoticeaakritiÎncă nu există evaluări

- PlacementDocument3 paginiPlacementaakritiÎncă nu există evaluări

- Amity Business SchoolDocument3 paginiAmity Business SchoolaakritiÎncă nu există evaluări

- 5f30fshortlisted Students Interview. Simpsons & Co LTD, Fi PL 2020 NoticeDocument2 pagini5f30fshortlisted Students Interview. Simpsons & Co LTD, Fi PL 2020 NoticeaakritiÎncă nu există evaluări

- Sales Department RelationsDocument4 paginiSales Department RelationsaakritiÎncă nu există evaluări

- Chik Shampoo: Ishminder Pal Singh Bhatia 32211 Marketing BDocument2 paginiChik Shampoo: Ishminder Pal Singh Bhatia 32211 Marketing BaakritiÎncă nu există evaluări

- Can India Become A 5 Trillion Economy byDocument9 paginiCan India Become A 5 Trillion Economy byaakritiÎncă nu există evaluări

- Uttar Pradesh: S. No. Student's Name Enrollment No. Contact No. Program CgpaDocument2 paginiUttar Pradesh: S. No. Student's Name Enrollment No. Contact No. Program CgpaaakritiÎncă nu există evaluări

- Frequencies: NotesDocument26 paginiFrequencies: NotesaakritiÎncă nu există evaluări

- FordDocument16 paginiFordaakritiÎncă nu există evaluări

- BritaniaDocument18 paginiBritaniaaakritiÎncă nu există evaluări

- Visum UnterlagenDocument19 paginiVisum Unterlagenapi-289435089Încă nu există evaluări

- Management of Food Inspection in TanzaniaDocument104 paginiManagement of Food Inspection in TanzaniaMichael MalabejaÎncă nu există evaluări

- Governance Questions For UPSC MainsDocument4 paginiGovernance Questions For UPSC Mainscommissioner social welfareÎncă nu există evaluări

- Circuit JudgesDocument9 paginiCircuit JudgesScribd Government DocsÎncă nu există evaluări

- Assignment ID 242871 Bismarck HealhcareDocument9 paginiAssignment ID 242871 Bismarck HealhcarePETER KAMOTHOÎncă nu există evaluări

- 2011 Behind The Kitchen Door Multi Site StudyDocument2 pagini2011 Behind The Kitchen Door Multi Site StudyROCUnitedÎncă nu există evaluări

- S. Walton Letter To FDA FINALDocument13 paginiS. Walton Letter To FDA FINALJoe EskenaziÎncă nu există evaluări

- Vwa Traffic MGT ChecklistDocument1 paginăVwa Traffic MGT ChecklistAnonymous ANmMebffKRÎncă nu există evaluări

- Lifeline Supreme BrochureDocument5 paginiLifeline Supreme BrochureSumit BhandariÎncă nu există evaluări

- JV - Ohsas - Iso 45001 - Norma MccormickDocument58 paginiJV - Ohsas - Iso 45001 - Norma MccormickElkin CorreaÎncă nu există evaluări

- Internship Report On Oil and GasDocument112 paginiInternship Report On Oil and GasSadia LiaqatÎncă nu există evaluări

- Claim FormDocument4 paginiClaim Formdharani633Încă nu există evaluări

- Intro To US HealthCare Exam 1 Study GuideDocument10 paginiIntro To US HealthCare Exam 1 Study GuideMiaLeiÎncă nu există evaluări

- The Rape ("Lo Stupro") by Franca Rame Translated by Ed EmeryDocument6 paginiThe Rape ("Lo Stupro") by Franca Rame Translated by Ed EmerypremaseemaÎncă nu există evaluări

- VA-OIG - Review of Battle Creek VAMCDocument37 paginiVA-OIG - Review of Battle Creek VAMCMaster ChiefÎncă nu există evaluări

- Maharashtra Public Service Commission Maharashtra Subordinate Services Main Examination - 2019Document59 paginiMaharashtra Public Service Commission Maharashtra Subordinate Services Main Examination - 2019S KatyarmalÎncă nu există evaluări

- DSWD-RLA Form 3 (Application Form For Accreditation) - 3192019Document3 paginiDSWD-RLA Form 3 (Application Form For Accreditation) - 3192019John Denver Crusit50% (2)

- Vba 21 8940 AreDocument2 paginiVba 21 8940 AreMitchell Doogie HouserÎncă nu există evaluări

- Title 2 (Animal Welfare) Chapter 1 (General Santos City Animal Shelter) Ord No 11 S of 2013Document6 paginiTitle 2 (Animal Welfare) Chapter 1 (General Santos City Animal Shelter) Ord No 11 S of 2013roy rubaÎncă nu există evaluări

- Maine Medicad Mistakes.Document3 paginiMaine Medicad Mistakes.Vamsi KrishnaÎncă nu există evaluări

- Category: Capital, Tier 2: City: Bhopal State: Madhya PradeshDocument5 paginiCategory: Capital, Tier 2: City: Bhopal State: Madhya PradeshARSHI PARASHARÎncă nu există evaluări

- 2023 01 06 Toole FM Complaint at LawDocument18 pagini2023 01 06 Toole FM Complaint at LawNewsTeam20Încă nu există evaluări

- Chidya Et Al 2016 Testing Methods For New Pit Latrine Designs in Rural and Peri-Urban Areas of MalawiDocument7 paginiChidya Et Al 2016 Testing Methods For New Pit Latrine Designs in Rural and Peri-Urban Areas of MalawiEddiemtongaÎncă nu există evaluări