S-ar putea să vă placă și

- Using Economic Indicators to Improve Investment AnalysisDe la EverandUsing Economic Indicators to Improve Investment AnalysisEvaluare: 3.5 din 5 stele3.5/5 (1)

- Balance of Payment ComparisonDocument24 paginiBalance of Payment Comparisonneeteesh_nautiyalÎncă nu există evaluări

- Tales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityDe la EverandTales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityÎncă nu există evaluări

- Debashis Chakraborty and Zaki HussainDocument28 paginiDebashis Chakraborty and Zaki HussainPARUL SINGH MBA 2019-21 (Delhi)Încă nu există evaluări

- The Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaDe la EverandThe Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaÎncă nu există evaluări

- Indira School of Business Studies: Submitted To: Prof. Guha BijoyDocument12 paginiIndira School of Business Studies: Submitted To: Prof. Guha BijoyAnkush DagorÎncă nu există evaluări

- SBI-MultiCap-Fund 2Document9 paginiSBI-MultiCap-Fund 2garvitaneja477Încă nu există evaluări

- Trade in Services in India: Implications For Poverty and InequalityDocument20 paginiTrade in Services in India: Implications For Poverty and InequalityMandeep Singh BirdiÎncă nu există evaluări

- Sbi Magnum Children S Benefit Fund - Investment PlanDocument9 paginiSbi Magnum Children S Benefit Fund - Investment PlanManoja ManivasagamÎncă nu există evaluări

- Enhancing India-Indonesia Trade Relations - Amids Pandemic Covid-19 - 28 April 21Document28 paginiEnhancing India-Indonesia Trade Relations - Amids Pandemic Covid-19 - 28 April 21Hendra NusantaraÎncă nu există evaluări

- Bab I Pendahuluan A. Latar Belakang Masalah: Estate Sangat Berperan Penting Dalam Perekonomian SuatuDocument14 paginiBab I Pendahuluan A. Latar Belakang Masalah: Estate Sangat Berperan Penting Dalam Perekonomian SuaturahayuÎncă nu există evaluări

- Ar01022 P PDFDocument78 paginiAr01022 P PDFvirat swaroopÎncă nu există evaluări

- 20231013144704MRFT, May 2023Document21 pagini20231013144704MRFT, May 2023pinakchatterjee669Încă nu există evaluări

- Polypropylene - 2023 Data - 2013-2022 Historical - 2024 Forecast - Price - QuoteDocument1 paginăPolypropylene - 2023 Data - 2013-2022 Historical - 2024 Forecast - Price - Quotepm.quenelleÎncă nu există evaluări

- Informal Sector in BangladeshDocument11 paginiInformal Sector in Bangladeshshoaiburrahman958Încă nu există evaluări

- 1 4 2 Methodology 5 3 Data Collection 6 4 Regression Analysis 7 5 Findings and Interpretation 6 Conclusion 7 Annexures 8 ReferencesDocument7 pagini1 4 2 Methodology 5 3 Data Collection 6 4 Regression Analysis 7 5 Findings and Interpretation 6 Conclusion 7 Annexures 8 ReferencesSonal GuptaÎncă nu există evaluări

- DPR PDFDocument158 paginiDPR PDFFashionnift NiftÎncă nu există evaluări

- Handling Methods TechniquesDocument11 paginiHandling Methods TechniquesDusabeyezu PacifiqueÎncă nu există evaluări

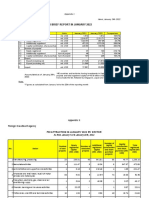

- Fdi Brief Report in January 2022: Appendix I Foreign Investment AgencyDocument11 paginiFdi Brief Report in January 2022: Appendix I Foreign Investment AgencyQuan Hong NgoÎncă nu există evaluări

- Latihan 3 RSCADocument5 paginiLatihan 3 RSCAEnrique StephanÎncă nu există evaluări

- CCATDocument19 paginiCCATgemmangbnÎncă nu există evaluări

- 2.0 Energy Questions 2Document10 pagini2.0 Energy Questions 2Raqeeb Ahmad KhanÎncă nu există evaluări

- Integrated Approach To The Growing Msme Sector: Dr. B. Yerram Raju, Ph.D. Economist & Risk Management ConsultantDocument22 paginiIntegrated Approach To The Growing Msme Sector: Dr. B. Yerram Raju, Ph.D. Economist & Risk Management ConsultantmuschiobianccoÎncă nu există evaluări

- IIP HighlightsDocument3 paginiIIP HighlightsSouravÎncă nu există evaluări

- 3-wg4-4 Retno Gumilang Dewi PDFDocument31 pagini3-wg4-4 Retno Gumilang Dewi PDFIndra Chandra SetiawanÎncă nu există evaluări

- Business Plan For Establishment of Liquid Detergent PlantDocument22 paginiBusiness Plan For Establishment of Liquid Detergent PlantĐạt Diệp0% (1)

- GroupWiseChapters 4Document414 paginiGroupWiseChapters 4Awadh GroupÎncă nu există evaluări

- Country Ranking Analysis TemplateDocument12 paginiCountry Ranking Analysis Templatesendano 0Încă nu există evaluări

- 266 JRG16 A01Document10 pagini266 JRG16 A01Ritesh ChatterjeeÎncă nu există evaluări

- HDFC Equity Fund Is An Open-Ended Growth Scheme, Which Aims To Generate Long-TermDocument8 paginiHDFC Equity Fund Is An Open-Ended Growth Scheme, Which Aims To Generate Long-Termshreedhar mohtaÎncă nu există evaluări

- 2005-10-12 - Trade Policy Review - Report by The Secretariat On Trinidad & Tobago PART1 (WTTPRS151R1-1)Document13 pagini2005-10-12 - Trade Policy Review - Report by The Secretariat On Trinidad & Tobago PART1 (WTTPRS151R1-1)Office of Trade Negotiations (OTN), CARICOM SecretariatÎncă nu există evaluări

- Input - Output Analysis: Rini Novrianti Sutardjo TuiDocument13 paginiInput - Output Analysis: Rini Novrianti Sutardjo TuiFaidel AfrianÎncă nu există evaluări

- Sbi Small Cap Fund Portfolio (November-2022-329-1)Document11 paginiSbi Small Cap Fund Portfolio (November-2022-329-1)Shivam PorwalÎncă nu există evaluări

- Part 2 Southeast Asia and The Pacific International LinkagesDocument129 paginiPart 2 Southeast Asia and The Pacific International LinkagesErizelle Anne BrunoÎncă nu există evaluări

- Microeconomics Overview of Bangladesh (Autosaved) 1Document14 paginiMicroeconomics Overview of Bangladesh (Autosaved) 159-Bushra Binte SayedÎncă nu există evaluări

- Industrial CanvasDocument27 paginiIndustrial CanvasTed Habtu Mamo AsratÎncă nu există evaluări

- Export Efforts of Manufactured Goods: Recent Trends in ExportsDocument8 paginiExport Efforts of Manufactured Goods: Recent Trends in ExportsprathlakshmiÎncă nu există evaluări

- MPRA Paper 79472Document15 paginiMPRA Paper 79472SudarismanÎncă nu există evaluări

- Leather ShoesDocument30 paginiLeather ShoesOmbrico100% (1)

- PBV Europe 21Document9 paginiPBV Europe 21g.straziotaÎncă nu există evaluări

- Cmonthly WPI Jan 2021Document5 paginiCmonthly WPI Jan 2021CuriousMan87Încă nu există evaluări

- Welding Machine Production PlantDocument26 paginiWelding Machine Production PlantJohn100% (1)

- Economic Policy Uncertainty in Times of COVID-19 Pandemic Economic Policy Uncertainty in Times of COVID-19 PandemicDocument4 paginiEconomic Policy Uncertainty in Times of COVID-19 Pandemic Economic Policy Uncertainty in Times of COVID-19 PandemicCésar MalagutiÎncă nu există evaluări

- Aeotab 20Document6 paginiAeotab 20Johannes ForstpointnerÎncă nu există evaluări

- An Analytical Study On Performance of Soyabean Crop in IndiaDocument7 paginiAn Analytical Study On Performance of Soyabean Crop in IndiaIJRASETPublicationsÎncă nu există evaluări

- Production and Export of TeaDocument4 paginiProduction and Export of TeaJose Tenny100% (1)

- Icici Prudential Amc - SharikaDocument12 paginiIcici Prudential Amc - SharikacitihdbÎncă nu există evaluări

- Economic Impact of Tariff HikesDocument19 paginiEconomic Impact of Tariff HikesThu Phương NguyễnÎncă nu există evaluări

- 2022 LuoDocument21 pagini2022 LuoKiều Lê Nhật ĐôngÎncă nu există evaluări

- Dissemination Air PDFDocument40 paginiDissemination Air PDFJhonny AguirreÎncă nu există evaluări

- 1807-Article Text-3386-1-10-20210408Document10 pagini1807-Article Text-3386-1-10-20210408Ritesh ChatterjeeÎncă nu există evaluări

- Sbi Small Cap Fund Portfolio (December-2021-329-1)Document11 paginiSbi Small Cap Fund Portfolio (December-2021-329-1)SanjivaniÎncă nu există evaluări

- Business Field: Provision of Accommodation and Food and DrinkDocument4 paginiBusiness Field: Provision of Accommodation and Food and DrinkLena LeezÎncă nu există evaluări

- List of Companies of IndiaDocument18 paginiList of Companies of IndiaKiran SonarÎncă nu există evaluări

- New Delhi, Date: November 16th, 2020 Press Release Index Numbers of Wholesale Price in India For The Month of October, 2020Document5 paginiNew Delhi, Date: November 16th, 2020 Press Release Index Numbers of Wholesale Price in India For The Month of October, 2020venuÎncă nu există evaluări

- Quant ESG Equity Fund Sep 2022Document9 paginiQuant ESG Equity Fund Sep 2022vnrÎncă nu există evaluări

- Vinyl 2Document5 paginiVinyl 2Joulo YabutÎncă nu există evaluări

- Accident Frequency RatesDocument4 paginiAccident Frequency RateskakoroÎncă nu există evaluări

- Resource Estimate Report For: Author (S)Document71 paginiResource Estimate Report For: Author (S)riecuantiqueÎncă nu există evaluări

- Conveyor Belts of TextileDocument25 paginiConveyor Belts of TextileTed Habtu Mamo AsratÎncă nu există evaluări

- SalarySlip (1001) 8 - 2019Document1 paginăSalarySlip (1001) 8 - 2019Laavanyah ManimaranÎncă nu există evaluări

- Gov't Spending P910B On Infrastructure This YearDocument2 paginiGov't Spending P910B On Infrastructure This YearChristopher SalcedoÎncă nu există evaluări

- Acct Statement - XX2482 - 04032023 PDFDocument13 paginiAcct Statement - XX2482 - 04032023 PDFKoushik ChakrabortyÎncă nu există evaluări

- About The IMFDocument6 paginiAbout The IMFkiranaishaÎncă nu există evaluări

- International Finance Assignment 2Document13 paginiInternational Finance Assignment 2M.A. TanvirÎncă nu există evaluări

- United Kingdom: 2021 Annual Research: Key HighlightsDocument2 paginiUnited Kingdom: 2021 Annual Research: Key HighlightsLisani DubeÎncă nu există evaluări

- Case Argument and Counter ArgumentDocument4 paginiCase Argument and Counter ArgumentErvin SagunÎncă nu există evaluări

- Name: Abdullah Id: A2007f0671 Group: MD-09Document2 paginiName: Abdullah Id: A2007f0671 Group: MD-09Dicoding KlompokÎncă nu există evaluări

- Acct Statement - XX6419 - 08112022Document26 paginiAcct Statement - XX6419 - 08112022AartiÎncă nu există evaluări

- Private University Industry in Bangladesh: Political FactorsDocument2 paginiPrivate University Industry in Bangladesh: Political FactorsTouhidur Rahman TuhinÎncă nu există evaluări

- QUIZ - Political Economy of International TradeDocument3 paginiQUIZ - Political Economy of International TradeAngel Chane OstrazÎncă nu există evaluări

- 1991 India Economic CrisisDocument3 pagini1991 India Economic CrisisDev DeepÎncă nu există evaluări

- Teaser - Bora Slaughter ProjectDocument1 paginăTeaser - Bora Slaughter ProjectAbegaz AmareÎncă nu există evaluări

- Error Exercise - Sentence CompletionDocument3 paginiError Exercise - Sentence CompletionsmnxwxÎncă nu există evaluări

- Tamta hw2Document2 paginiTamta hw2aleqsi gemiashviliÎncă nu există evaluări

- Production Linked Incentive (PLI) : A Well-Formulated SchemeDocument4 paginiProduction Linked Incentive (PLI) : A Well-Formulated SchemeSHIVAM SRIVASTAVAÎncă nu există evaluări

- Philippines Overview of Economy, Information About Overview of Economy in PhilippinesDocument5 paginiPhilippines Overview of Economy, Information About Overview of Economy in PhilippinesFrance TolentinoÎncă nu există evaluări

- New International Economic OrderDocument15 paginiNew International Economic OrderBharat Bhushan100% (1)

- Group 2 GLOBAL INTERSTATE SYSTEM 1Document21 paginiGroup 2 GLOBAL INTERSTATE SYSTEM 1Jashi SiosonÎncă nu există evaluări

- Exercise - Estate Tax 2Document2 paginiExercise - Estate Tax 2Mark Edgar De GuzmanÎncă nu există evaluări

- Bilateral Trade Agreements Between India & PakistanDocument15 paginiBilateral Trade Agreements Between India & PakistanSumanjit DebÎncă nu există evaluări

- What Is Economic IntegrationDocument5 paginiWhat Is Economic IntegrationRicky IsmaelÎncă nu există evaluări

- Reading Comprehension Passage-3 Read The Passage Carefully and Answer The FollowingDocument2 paginiReading Comprehension Passage-3 Read The Passage Carefully and Answer The FollowingadiG48 AtdiG48Încă nu există evaluări

- CO1 Topic 2 Global EconomyDocument17 paginiCO1 Topic 2 Global EconomyFatimah Rahima JingonaÎncă nu există evaluări

- 10000271-3-2023-Potlakayala NaveenDocument1 pagină10000271-3-2023-Potlakayala NaveenG Yugandhar Alwaz UniqueÎncă nu există evaluări

- MOGSS International (Autosaved)Document9 paginiMOGSS International (Autosaved)Ken TunÎncă nu există evaluări

- One-Customs (Paperless Goods Declaration Processing System)Document2 paginiOne-Customs (Paperless Goods Declaration Processing System)Adnan KhanÎncă nu există evaluări

- Dgca Air RegulationDocument83 paginiDgca Air RegulationprachatÎncă nu există evaluări

- Bahaging Ginagampanan NG Igo'sDocument24 paginiBahaging Ginagampanan NG Igo'sEdrei Jehezekel Javier100% (1)

- Arts and Culture's Contribution To Philippine Poitical EconomyDocument2 paginiArts and Culture's Contribution To Philippine Poitical EconomyASDFGHÎncă nu există evaluări

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDe la EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingEvaluare: 4.5 din 5 stele4.5/5 (98)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDe la EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassÎncă nu există evaluări

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationDe la EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationEvaluare: 4 din 5 stele4/5 (11)

- Economics 101: How the World WorksDe la EverandEconomics 101: How the World WorksEvaluare: 4.5 din 5 stele4.5/5 (34)

- This Changes Everything: Capitalism vs. The ClimateDe la EverandThis Changes Everything: Capitalism vs. The ClimateEvaluare: 4 din 5 stele4/5 (349)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaDe la EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaÎncă nu există evaluări

- How an Economy Grows and Why It Crashes: Collector's EditionDe la EverandHow an Economy Grows and Why It Crashes: Collector's EditionEvaluare: 4.5 din 5 stele4.5/5 (103)

- The Meth Lunches: Food and Longing in an American CityDe la EverandThe Meth Lunches: Food and Longing in an American CityEvaluare: 5 din 5 stele5/5 (5)

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsDe la EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsEvaluare: 4.5 din 5 stele4.5/5 (94)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesDe la EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesEvaluare: 4.5 din 5 stele4.5/5 (9)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailDe la EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailEvaluare: 4.5 din 5 stele4.5/5 (239)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationDe la EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationEvaluare: 4.5 din 5 stele4.5/5 (46)

- Vienna: How the City of Ideas Created the Modern WorldDe la EverandVienna: How the City of Ideas Created the Modern WorldÎncă nu există evaluări

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumDe la EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumEvaluare: 3 din 5 stele3/5 (12)

- Economics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsDe la EverandEconomics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsEvaluare: 5 din 5 stele5/5 (3)

- Requiem for the American Dream: The 10 Principles of Concentration of Wealth & PowerDe la EverandRequiem for the American Dream: The 10 Principles of Concentration of Wealth & PowerEvaluare: 4.5 din 5 stele4.5/5 (213)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyDe la EverandChip War: The Quest to Dominate the World's Most Critical TechnologyEvaluare: 4.5 din 5 stele4.5/5 (229)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetDe la EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetÎncă nu există evaluări

- Doughnut Economics: Seven Ways to Think Like a 21st-Century EconomistDe la EverandDoughnut Economics: Seven Ways to Think Like a 21st-Century EconomistEvaluare: 4.5 din 5 stele4.5/5 (37)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomDe la EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomÎncă nu există evaluări

- Second Class: How the Elites Betrayed America's Working Men and WomenDe la EverandSecond Class: How the Elites Betrayed America's Working Men and WomenÎncă nu există evaluări