S-ar putea să vă placă și

- InstrumentsDocument33 paginiInstrumentsmiaaaw94Încă nu există evaluări

- Group 1Document15 paginiGroup 1Rolly BaniquedÎncă nu există evaluări

- Dimensions of TrucksDocument3 paginiDimensions of TrucksanandakumarÎncă nu există evaluări

- GG NaDocument10 paginiGG NaRolly BaniquedÎncă nu există evaluări

- Commission On Audit: 2t/rp:uhlir NFDocument4 paginiCommission On Audit: 2t/rp:uhlir NFKatherine PacenoÎncă nu există evaluări

- Explanatory Text-Urban and Rural ClassificationDocument4 paginiExplanatory Text-Urban and Rural ClassificationJawo JimenezÎncă nu există evaluări

- TRAIN PresentationDocument17 paginiTRAIN PresentationApril Mae Niego MaputeÎncă nu există evaluări

- Review of Related LiteratureDocument3 paginiReview of Related LiteratureRolly BaniquedÎncă nu există evaluări

- Direct Taxation: Study NotesDocument610 paginiDirect Taxation: Study NotesAvneet SinghÎncă nu există evaluări

- The Barangay ac-WPS OfficeDocument1 paginăThe Barangay ac-WPS OfficeRolly BaniquedÎncă nu există evaluări

- The Philippine Government Information System PDFDocument27 paginiThe Philippine Government Information System PDFGiYan SalvadorÎncă nu există evaluări

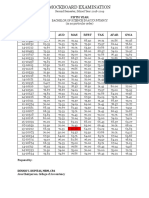

- Mockboard Examination: Id. NoDocument1 paginăMockboard Examination: Id. NoRolly BaniquedÎncă nu există evaluări

- TheoryDocument1 paginăTheoryRolly BaniquedÎncă nu există evaluări

- Case Study Written ReportDocument39 paginiCase Study Written ReportRolly BaniquedÎncă nu există evaluări

- The Revenue Cycle: Accounting Information Systems, 7eDocument46 paginiThe Revenue Cycle: Accounting Information Systems, 7ekevin nagacÎncă nu există evaluări

- LP - Acctg - 19 - 1stsem - 2019-2020Document16 paginiLP - Acctg - 19 - 1stsem - 2019-2020Rolly BaniquedÎncă nu există evaluări

- Net Operating Income Sales Sales Average Operating Assets Net Operating Income Average Operating AssetsDocument4 paginiNet Operating Income Sales Sales Average Operating Assets Net Operating Income Average Operating AssetsRolly BaniquedÎncă nu există evaluări

- Gov SEC MeetingDocument1 paginăGov SEC MeetingRolly BaniquedÎncă nu există evaluări

- Gov SEC MeetingDocument1 paginăGov SEC MeetingRolly BaniquedÎncă nu există evaluări

- University of La Salette Inc. College of Accountancy College of Accountancy Student Council Dubinan East, Santiago City, PhilippinesDocument3 paginiUniversity of La Salette Inc. College of Accountancy College of Accountancy Student Council Dubinan East, Santiago City, PhilippinesRolly BaniquedÎncă nu există evaluări

- Campus Tour Groupings and LocationDocument5 paginiCampus Tour Groupings and LocationRolly BaniquedÎncă nu există evaluări

- Dimensions of TrucksDocument3 paginiDimensions of TrucksanandakumarÎncă nu există evaluări

- Predictors of Performance in The Licensure Examination For Agriculturists: Bases For A Proposed Plan of ActionDocument8 paginiPredictors of Performance in The Licensure Examination For Agriculturists: Bases For A Proposed Plan of ActionMaryrose BaguioÎncă nu există evaluări

- Mockboard Examination Result - Fifth Year PDFDocument1 paginăMockboard Examination Result - Fifth Year PDFRolly BaniquedÎncă nu există evaluări

- Customer Privacy Policy 2019 V1Document2 paginiCustomer Privacy Policy 2019 V1Rolly BaniquedÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Infosys Life CycleDocument6 paginiInfosys Life CycleraghupadhyaÎncă nu există evaluări

- ANA Demand Generation Maturity ModelDocument2 paginiANA Demand Generation Maturity ModelDemand MetricÎncă nu există evaluări

- Profit Center ApproachDocument5 paginiProfit Center ApproachKunal ThakurÎncă nu există evaluări

- Consolidation TheoriesDocument5 paginiConsolidation TheoriesAyan RoyÎncă nu există evaluări

- Chapter 1: Cards 304Document18 paginiChapter 1: Cards 304sureshrockzÎncă nu există evaluări

- A Study of E-Filing of Income Tax ReturnsDocument4 paginiA Study of E-Filing of Income Tax ReturnsAnsh BhallaÎncă nu există evaluări

- Lambeth Contract Standing Orders PDFDocument23 paginiLambeth Contract Standing Orders PDFAshley ElizabethÎncă nu există evaluări

- World Candle Congress and Promotional CompaniesDocument36 paginiWorld Candle Congress and Promotional CompaniesRony JamesÎncă nu există evaluări

- Googles Success Ben Morrow Thesis 2008 PDFDocument31 paginiGoogles Success Ben Morrow Thesis 2008 PDFAzim MohammedÎncă nu există evaluări

- Argos Software User ManualDocument250 paginiArgos Software User Manualjvidyala50% (2)

- 20-05-15 DED20cv655 Sisvel v. Tesla ComplaintDocument26 pagini20-05-15 DED20cv655 Sisvel v. Tesla ComplaintFlorian MuellerÎncă nu există evaluări

- The Nature of Secondary Sources of InformationDocument6 paginiThe Nature of Secondary Sources of InformationSingh ViratÎncă nu există evaluări

- MATHDocument18 paginiMATHManjesh Kumar SinghÎncă nu există evaluări

- Commission Protection and Confidentiality Agreement - Petroleum and CommoditiesDocument2 paginiCommission Protection and Confidentiality Agreement - Petroleum and CommoditiesJohms Gool100% (10)

- BusinessConfiguration BA en PDFDocument68 paginiBusinessConfiguration BA en PDFPrashant SinghÎncă nu există evaluări

- COPC Standard RequirementsDocument112 paginiCOPC Standard Requirementsakdmech9621100% (1)

- AUDITING AS AN INSTRUMENT FOR ENSURING ACCOUNTABILITY ShettyDocument8 paginiAUDITING AS AN INSTRUMENT FOR ENSURING ACCOUNTABILITY ShettyAnandkumar GuptaÎncă nu există evaluări

- FunnyJunk - The Oatmeal ResponseDocument6 paginiFunnyJunk - The Oatmeal ResponseVenkat Balasubramani100% (2)

- Audit-Planning Pup Evals CLNDocument6 paginiAudit-Planning Pup Evals CLNPaula MerrilesÎncă nu există evaluări

- CYD Agreement Addendum Non Compete Agreement TemplateDocument4 paginiCYD Agreement Addendum Non Compete Agreement Templatekool waÎncă nu există evaluări

- Marketing Analysis Marketing ResearchDocument3 paginiMarketing Analysis Marketing ResearchDaisy Ann Dela CruzÎncă nu există evaluări

- Aecukbimprotocol v2 0Document46 paginiAecukbimprotocol v2 0Ivana ŽivkovićÎncă nu există evaluări

- VANET - Vehicular Applications and Inter-Networking TechnologiesDocument32 paginiVANET - Vehicular Applications and Inter-Networking TechnologiesMariam202Încă nu există evaluări

- D&D 3.5 Swords of Power PDFDocument18 paginiD&D 3.5 Swords of Power PDFArthur TinocoÎncă nu există evaluări

- Final Assignment CRMDocument24 paginiFinal Assignment CRMDumidu Chathurange Dassanayake0% (1)

- Memorandum of Understanding Template 1Document2 paginiMemorandum of Understanding Template 1AlvinGutierrezÎncă nu există evaluări

- BALAJI UDYOG in Bankura, West Bengal, India - Company ProfileDocument2 paginiBALAJI UDYOG in Bankura, West Bengal, India - Company Profilesonam6236590Încă nu există evaluări

- How To Master The Art of Selling: Tom HopkinsDocument10 paginiHow To Master The Art of Selling: Tom HopkinsRahilHakimÎncă nu există evaluări

- Consumer RMA Claim Form Ver1 0FDocument5 paginiConsumer RMA Claim Form Ver1 0Fanon_999151Încă nu există evaluări

- Laser Model Interface Reference ManualDocument18 paginiLaser Model Interface Reference ManualManny Mendoza100% (1)