S-ar putea să vă placă și

- Tugas 6 AKM1 Muhammad Alfarizi 142200278 EA-IDocument9 paginiTugas 6 AKM1 Muhammad Alfarizi 142200278 EA-Imuhammad alfariziÎncă nu există evaluări

- Ch7 Ex WsDocument6 paginiCh7 Ex WsFoong Chan PingÎncă nu există evaluări

- Homework Chapter 6Document10 paginiHomework Chapter 6Le Nguyen Thu UyenÎncă nu există evaluări

- E16-10 Prepare Adjusting Entry To Record Fair Value, and Indicate Statement PresentationDocument2 paginiE16-10 Prepare Adjusting Entry To Record Fair Value, and Indicate Statement PresentationRisky FernandoÎncă nu există evaluări

- 645873Document3 pagini645873mohitgaba19Încă nu există evaluări

- Deposits in Transit and Outstanding Checks PDFDocument1 paginăDeposits in Transit and Outstanding Checks PDFAaliyah Joize LegaspiÎncă nu există evaluări

- LATIH SOAL M3 3 Laporan Laba Rugi Dan Hal Lain Yg BerkaitanDocument2 paginiLATIH SOAL M3 3 Laporan Laba Rugi Dan Hal Lain Yg BerkaitanBlue FinderÎncă nu există evaluări

- Akuntansi Keuangan 1 TUGAS E5.11, E5.12, E5.15 DAN E5.16 Kelas ADocument8 paginiAkuntansi Keuangan 1 TUGAS E5.11, E5.12, E5.15 DAN E5.16 Kelas ADedep0% (1)

- Pa 2Document9 paginiPa 2Aditya DzikirÎncă nu există evaluări

- 20210213174013D3066 - Soal Cost System and Cost AccumulationDocument6 pagini20210213174013D3066 - Soal Cost System and Cost AccumulationLydia limÎncă nu există evaluări

- Kieso Chapter 13Document98 paginiKieso Chapter 13GraceÎncă nu există evaluări

- Tutorial Laporan Arus KasDocument17 paginiTutorial Laporan Arus KasRatna DwiÎncă nu există evaluări

- Erika Christina - LD53 - Latihan KPDocument14 paginiErika Christina - LD53 - Latihan KPNatasha HerlianaÎncă nu există evaluări

- Flow of Production: Physica L Units Direct Materials Conversio NDocument2 paginiFlow of Production: Physica L Units Direct Materials Conversio NMhea Ann Pauline Arsino100% (1)

- Chapter 7 Supplemental QuestionsDocument7 paginiChapter 7 Supplemental QuestionsDita Ens100% (1)

- Week 4 Practice Questions 1Document17 paginiWeek 4 Practice Questions 1Gabriel Abdillah100% (1)

- Tugas CompletingDocument6 paginiTugas CompletingWidad NadiaÎncă nu există evaluări

- Hercules Poirot WorksheetDocument6 paginiHercules Poirot WorksheetvaldaÎncă nu există evaluări

- P2 41 2 42 SolutionsDocument3 paginiP2 41 2 42 SolutionsMarjorie PalmaÎncă nu există evaluări

- P11Document7 paginiP11Arif RahmanÎncă nu există evaluări

- Exercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueDocument9 paginiExercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueManuel Magadatu100% (1)

- Condensed Income Statement, Periodic Inventory MethodDocument2 paginiCondensed Income Statement, Periodic Inventory MethodAsma HatamÎncă nu există evaluări

- Working 4Document8 paginiWorking 4Hà Lê DuyÎncă nu există evaluări

- TR 2 IndahDocument3 paginiTR 2 IndahIndahyuliaputriÎncă nu există evaluări

- Tugas PPE 1Document12 paginiTugas PPE 1Bertha Liona0% (1)

- Process CostingDocument19 paginiProcess CostingmilleranÎncă nu există evaluări

- IFRS Edition-2nd: The Accounting Information SystemDocument88 paginiIFRS Edition-2nd: The Accounting Information SystemmariaÎncă nu există evaluări

- Tugas 4 AKM - Kelompok 5 - 142200278Document13 paginiTugas 4 AKM - Kelompok 5 - 142200278muhammad alfariziÎncă nu există evaluări

- Chapter 3 Homework Chapter 3 HomeworkDocument8 paginiChapter 3 Homework Chapter 3 HomeworkPhương NguyễnÎncă nu există evaluări

- Be16 P16 2aDocument7 paginiBe16 P16 2aLisa Hammerle ClarkÎncă nu există evaluări

- Chapter-04 Completing The Accounting Cycle (Maths)Document9 paginiChapter-04 Completing The Accounting Cycle (Maths)ShifatÎncă nu există evaluări

- Pembahasan CH 3 4 5Document30 paginiPembahasan CH 3 4 5bella0% (1)

- Week 5 Tute Chapter 4 SolutionsDocument8 paginiWeek 5 Tute Chapter 4 SolutionsRaine PiliinÎncă nu există evaluări

- Quiz Review CH 5 6 7Document8 paginiQuiz Review CH 5 6 7yanto ismailÎncă nu există evaluări

- Fitzgeraldhyne Rappan - A031221038Document2 paginiFitzgeraldhyne Rappan - A031221038Fitzgeraldhyne RappanÎncă nu există evaluări

- E7 25Document2 paginiE7 25Muhammad Syafiq RamadhanÎncă nu există evaluări

- Chapter 13 Akun Keuangan TugasDocument2 paginiChapter 13 Akun Keuangan Tugassegeri kec0% (1)

- Akn p5 3a Pa1Document10 paginiAkn p5 3a Pa1Alche MistÎncă nu există evaluări

- Kieso IFRS4 TB ch17Document68 paginiKieso IFRS4 TB ch17Scarlet WitchÎncă nu există evaluări

- Ch09 Inventories - Additional Valuation IssuesDocument31 paginiCh09 Inventories - Additional Valuation IssuesNela Nafaza100% (1)

- Pengakun CH 09Document10 paginiPengakun CH 09nadia salsabilaÎncă nu există evaluări

- Tugas Kas PiutangDocument14 paginiTugas Kas PiutangDeby Nailatun FitriyahÎncă nu există evaluări

- Ch9 ExercisesDocument15 paginiCh9 ExercisesMarshanda BerliantiÎncă nu există evaluări

- Tugas 4 - AkuntansiDocument3 paginiTugas 4 - AkuntansiYusuf HadiÎncă nu există evaluări

- Latihan Accounts ReceivableDocument2 paginiLatihan Accounts ReceivableAlghifary RamadhanÎncă nu există evaluări

- End. 12,133 End. 6,950 End. 612Document3 paginiEnd. 12,133 End. 6,950 End. 612Nam NguyenÎncă nu există evaluări

- P3 4Document3 paginiP3 4Nam Nguyen100% (1)

- D6 F0121108 Helmy FebrianoDocument9 paginiD6 F0121108 Helmy FebrianohelmyÎncă nu există evaluări

- Inventory Valuation TutorialDocument4 paginiInventory Valuation TutorialSalma HazemÎncă nu există evaluări

- Fa2 TutorialDocument59 paginiFa2 TutorialNam PhươngÎncă nu există evaluări

- Regression Line of Overhead Costs On LaborDocument3 paginiRegression Line of Overhead Costs On LaborElliot Richard100% (1)

- Dzaky Farhansyah - V1620034 - E5-19 - P5-8A - P5-7ADocument15 paginiDzaky Farhansyah - V1620034 - E5-19 - P5-8A - P5-7ADzaky FarhansyahÎncă nu există evaluări

- Ganang Surya Hananta Swara 1901572691 Tugas Personal Ke-4 Minggu 8Document22 paginiGanang Surya Hananta Swara 1901572691 Tugas Personal Ke-4 Minggu 8Vira JilmiÎncă nu există evaluări

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 paginiNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarÎncă nu există evaluări

- CH 14Document39 paginiCH 14Iris MaÎncă nu există evaluări

- TaufiqAlInsanSiahaan - Tugas Akuntansi Keuangan Menengah 1Document6 paginiTaufiqAlInsanSiahaan - Tugas Akuntansi Keuangan Menengah 1taufiq al insanÎncă nu există evaluări

- Tugas MK Dasar Akuntansi Pertemuan Ke-15Document2 paginiTugas MK Dasar Akuntansi Pertemuan Ke-15Mochamad Ardan FauziÎncă nu există evaluări

- TALE - Meeting 4 (Lesson 6)Document17 paginiTALE - Meeting 4 (Lesson 6)Kevin ChandraÎncă nu există evaluări

- Units Remaining in Ending InventoryDocument4 paginiUnits Remaining in Ending InventoryQuynh Cao PhuongÎncă nu există evaluări

- Beginning Inventory Cost of Goods SoldDocument8 paginiBeginning Inventory Cost of Goods SoldAndres BorreroÎncă nu există evaluări

- HW 4Document4 paginiHW 4Mishalm96Încă nu există evaluări

- Final ExamDocument5 paginiFinal ExamMishalm96Încă nu există evaluări

- Golda Bear Acupuncturist Income Statement For The Month Ended September 30, 2019 RevenuesDocument2 paginiGolda Bear Acupuncturist Income Statement For The Month Ended September 30, 2019 RevenuesMishalm96Încă nu există evaluări

- HW 1Document4 paginiHW 1Mishalm96Încă nu există evaluări

- HW 2 RevisedDocument2 paginiHW 2 RevisedMishalm96Încă nu există evaluări

- HW 5Document1 paginăHW 5Mishalm96Încă nu există evaluări

- Mishal Mustafa BTA111 Prof. WuDocument2 paginiMishal Mustafa BTA111 Prof. WuMishalm96Încă nu există evaluări

- HW 2Document2 paginiHW 2Mishalm96Încă nu există evaluări

- HW 7Document2 paginiHW 7Mishalm96Încă nu există evaluări

- Evans PicsDocument2 paginiEvans PicsMishalm96Încă nu există evaluări

- HW 8Document4 paginiHW 8Mishalm96Încă nu există evaluări

- Monuments RevisedDocument1 paginăMonuments RevisedMishalm96Încă nu există evaluări

- PhotographsDocument2 paginiPhotographsMishalm96Încă nu există evaluări

- Prepayments LiabilitesDocument1 paginăPrepayments LiabilitesKrishele G. GotejerÎncă nu există evaluări

- 69 Customs Duty Tariff and Taxes in Ethiopia 1Document3 pagini69 Customs Duty Tariff and Taxes in Ethiopia 1Esrom AbebeÎncă nu există evaluări

- Ma101 Review Questions Part 1Document3 paginiMa101 Review Questions Part 1Ayush PatelÎncă nu există evaluări

- Pointers To Review BUSINESS TAXATIONDocument4 paginiPointers To Review BUSINESS TAXATIONFaizal MutiaÎncă nu există evaluări

- Bill FormsDocument12 paginiBill FormsVeerapandianÎncă nu există evaluări

- Local TaxationDocument240 paginiLocal TaxationJulia Inez BlandoÎncă nu există evaluări

- Revenue Memorandum Order No. 34-01Document8 paginiRevenue Memorandum Order No. 34-01johnnayelÎncă nu există evaluări

- LBP NO. 2 (Certified Statement of Receipts & Expenditures) (2013) GenDocument6 paginiLBP NO. 2 (Certified Statement of Receipts & Expenditures) (2013) GenBar2012Încă nu există evaluări

- Leases Income Taxes Employee Benefits: Rsoriano/JmaglinaoDocument3 paginiLeases Income Taxes Employee Benefits: Rsoriano/JmaglinaoMerliza JusayanÎncă nu există evaluări

- Treaty-Based Return Position Disclosure Under Section 6114 or 7701 (B)Document5 paginiTreaty-Based Return Position Disclosure Under Section 6114 or 7701 (B)Mohammed Ziaur RahamanÎncă nu există evaluări

- Transfer Pricing Country Profile BulgariaDocument16 paginiTransfer Pricing Country Profile BulgariaIoanna ZlatevaÎncă nu există evaluări

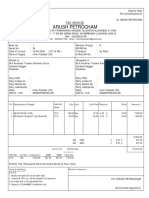

- InvoiceDocument1 paginăInvoiceChandrika NagarajÎncă nu există evaluări

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document4 paginiIncome Tax Department: Computerized Payment Receipt (CPR - It)M Naveed SultanÎncă nu există evaluări

- BIR RULING DA 202-08 NotesDocument2 paginiBIR RULING DA 202-08 NotesBal Nikko Joville - RocamoraÎncă nu există evaluări

- CIR Vs Cebu Toyo CorporationDocument2 paginiCIR Vs Cebu Toyo Corporationjancelmido1100% (2)

- Taxbanter Special Topic MaterialsDocument84 paginiTaxbanter Special Topic MaterialsJessica YuÎncă nu există evaluări

- Inheritance Tax Planning and Compliance RequirementsDocument4 paginiInheritance Tax Planning and Compliance RequirementsstflanagÎncă nu există evaluări

- OECD Report On PEs 2010Document241 paginiOECD Report On PEs 2010jcesar_pinedo1651Încă nu există evaluări

- Eco 1)Document3 paginiEco 1)A BPÎncă nu există evaluări

- Financial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Document2 paginiFinancial Results & Limited Review Report For June 30, 2015 (Standalone) (Result)Shyam SunderÎncă nu există evaluări

- Land Law Assignment TopicsDocument13 paginiLand Law Assignment TopicsShivani SinghÎncă nu există evaluări

- Supply Outward - 34Document3 paginiSupply Outward - 34DIVYANSHI PHOTO STATEÎncă nu există evaluări

- Annexure Gstam-ViiiDocument17 paginiAnnexure Gstam-ViiiHarsh ManiÎncă nu există evaluări

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument3 paginiBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountA&P ConsultancyÎncă nu există evaluări

- FINAL EXAMINATION 2019 Income TaxationDocument21 paginiFINAL EXAMINATION 2019 Income TaxationMark RevarezÎncă nu există evaluări

- 2022-23 TDSDocument6 pagini2022-23 TDSMujtabaAliKhanÎncă nu există evaluări

- SME Taxation in EuropeDocument631 paginiSME Taxation in EuropeAnonymous 4x7MVHcÎncă nu există evaluări

- Back Duty Investigations PDFDocument7 paginiBack Duty Investigations PDFSimon silaÎncă nu există evaluări

- Ecu - 08606 Lecture 6Document21 paginiEcu - 08606 Lecture 6DanielÎncă nu există evaluări

- Crowding OutDocument3 paginiCrowding OutRashmi RaniÎncă nu există evaluări