S-ar putea să vă placă și

- Cost & Managerial Accounting II EssentialsDe la EverandCost & Managerial Accounting II EssentialsEvaluare: 4 din 5 stele4/5 (1)

- Prelims Ms1Document6 paginiPrelims Ms1ALMA MORENAÎncă nu există evaluări

- Finance for Non-Financiers 2: Professional FinancesDe la EverandFinance for Non-Financiers 2: Professional FinancesÎncă nu există evaluări

- Module 4Document5 paginiModule 4Zvioule Ma Fuentes40% (5)

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageDe la EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageEvaluare: 5 din 5 stele5/5 (1)

- Strategic Cost Management Quiz No. 1Document5 paginiStrategic Cost Management Quiz No. 1Alexandra Nicole IsaacÎncă nu există evaluări

- The Key to Higher Profits: Pricing PowerDe la EverandThe Key to Higher Profits: Pricing PowerEvaluare: 5 din 5 stele5/5 (1)

- Module 4Document14 paginiModule 4Queenie ValleÎncă nu există evaluări

- Remodelers' Cost of Doing Business Study, 2020 EditionDe la EverandRemodelers' Cost of Doing Business Study, 2020 EditionÎncă nu există evaluări

- CVP-Analysis-Break-Even-PointDocument5 paginiCVP-Analysis-Break-Even-PointNCTÎncă nu există evaluări

- Module 4Document3 paginiModule 4Queenie ValleÎncă nu există evaluări

- How to Manage Future Costs and Risks Using Costing and MethodsDe la EverandHow to Manage Future Costs and Risks Using Costing and MethodsÎncă nu există evaluări

- EME6Document13 paginiEME6MoonlitÎncă nu există evaluări

- Throughput Accounting: A Guide to Constraint ManagementDe la EverandThroughput Accounting: A Guide to Constraint ManagementÎncă nu există evaluări

- Bobadilla Reviewer MASDocument3 paginiBobadilla Reviewer MASMae CruzÎncă nu există evaluări

- Mas 2 Departmental ExamzDocument8 paginiMas 2 Departmental ExamzjediiikÎncă nu există evaluări

- Bep and CVP Analysis Ms. NaparotaDocument4 paginiBep and CVP Analysis Ms. Naparotarichelle ann rodriguezÎncă nu există evaluări

- MANAGEMENT ADVISORY SERVICES GUIDEDocument10 paginiMANAGEMENT ADVISORY SERVICES GUIDEDanielÎncă nu există evaluări

- PrelimA2 - CVP AnalysisDocument8 paginiPrelimA2 - CVP AnalysishppddlÎncă nu există evaluări

- Mas Midterm 2020Document5 paginiMas Midterm 2020rodell pabloÎncă nu există evaluări

- CVP ANALYSIS QUIZ ASSESSMENTDocument12 paginiCVP ANALYSIS QUIZ ASSESSMENTBRYLL RODEL PONTINOÎncă nu există evaluări

- Quiz 14 - Financial ManagementDocument9 paginiQuiz 14 - Financial ManagementAurelio Delos Santos Macatulad Jr.Încă nu există evaluări

- Multiple Choice. Select The Letter That Corresponds To The Best Answer. This ExaminationDocument14 paginiMultiple Choice. Select The Letter That Corresponds To The Best Answer. This ExaminationBella ChoiÎncă nu există evaluări

- Accy111 CVP Questions and AnswersDocument32 paginiAccy111 CVP Questions and AnswersGurkiran KaurÎncă nu există evaluări

- This Study Resource Was: Preliminary Examination in MANACO1Document7 paginiThis Study Resource Was: Preliminary Examination in MANACO1Sadile May KayeÎncă nu există evaluări

- Mas - Midter-Ntc ExamDocument15 paginiMas - Midter-Ntc ExamRed YuÎncă nu există evaluări

- Pre FinalDocument8 paginiPre Finalpdmallari12Încă nu există evaluări

- CVP AssignmentDocument5 paginiCVP AssignmentAccounting MaterialsÎncă nu există evaluări

- MSQ-01 - Activity Cost & CVP Analysis (Final)Document11 paginiMSQ-01 - Activity Cost & CVP Analysis (Final)Mary Alcaflor40% (5)

- Prepared By: Jilly Boy G. Bruno Jr. and Jerome Marquez (Set A) - 1Document8 paginiPrepared By: Jilly Boy G. Bruno Jr. and Jerome Marquez (Set A) - 1BSIT 1A Yancy CaliganÎncă nu există evaluări

- Test Bank - Mgt. Acctg 2 - CparDocument16 paginiTest Bank - Mgt. Acctg 2 - CparChristian Blanza LlevaÎncă nu există evaluări

- Mas QuestionsDocument10 paginiMas QuestionsHeinie Joy PauleÎncă nu există evaluări

- Mas MidtermDocument10 paginiMas MidtermChristopher Nogot100% (2)

- Managerial Economics QuestionnairesDocument26 paginiManagerial Economics QuestionnairesClyde SaladagaÎncă nu există evaluări

- Mid TermDocument7 paginiMid Termpdmallari12Încă nu există evaluări

- Mas Variable and Absorption Costing Reviewer CompressDocument12 paginiMas Variable and Absorption Costing Reviewer CompressDanica Kaye MorcellosÎncă nu există evaluări

- Answer2 TaDocument13 paginiAnswer2 TaJohn BryanÎncă nu există evaluări

- MBA105 Managerial Accounting ExercisesDocument5 paginiMBA105 Managerial Accounting ExercisesTamieÎncă nu există evaluări

- MAS Assessment October 2020 PDFDocument15 paginiMAS Assessment October 2020 PDFARISÎncă nu există evaluări

- Management Advisory Services: ABC, CVP, and Cost AnalysisDocument8 paginiManagement Advisory Services: ABC, CVP, and Cost AnalysisNicoleÎncă nu există evaluări

- TheoryDocument9 paginiTheoryprettyÎncă nu există evaluări

- CVPDocument10 paginiCVPLorena Pernato0% (1)

- Test Bank For Cost Accounting Foundations and Evolutions 9th Edition Full DownloadDocument67 paginiTest Bank For Cost Accounting Foundations and Evolutions 9th Edition Full Downloadmatthewjacksonstjfaixoyp100% (19)

- Mas 3Document9 paginiMas 3Krishia GarciaÎncă nu există evaluări

- Cpa Review School of The Philippines Manila Management Advisory Services Variable Costing & Absorption CostingDocument12 paginiCpa Review School of The Philippines Manila Management Advisory Services Variable Costing & Absorption CostingAian GlennÎncă nu există evaluări

- MANAGEMENT ACCOUNTING EXAMDocument8 paginiMANAGEMENT ACCOUNTING EXAMChristopher NogotÎncă nu există evaluări

- Midterm Examination - MAS REVIEWDocument7 paginiMidterm Examination - MAS REVIEWFrancis MateosÎncă nu există evaluări

- Mockboard (Mas)Document3 paginiMockboard (Mas)Nezhreen MaruhomÎncă nu există evaluări

- 09 X07 C ResponsibilityDocument9 pagini09 X07 C ResponsibilityAnjo PadillaÎncă nu există evaluări

- MAS CVP Analysis HandoutsDocument8 paginiMAS CVP Analysis HandoutsMartha Nicole MaristelaÎncă nu există evaluări

- Acc102 FinalReviewDocument31 paginiAcc102 FinalReviewTiffany Beth CarltonÎncă nu există evaluări

- Cost Volume Profit AnalysisDocument9 paginiCost Volume Profit AnalysisIce Voltaire Buban GuiangÎncă nu există evaluări

- CVP ANALYSIS BREAK-EVEN POINTSDocument12 paginiCVP ANALYSIS BREAK-EVEN POINTSjayson86% (7)

- Variable Costing and Absorption CostingDocument15 paginiVariable Costing and Absorption CostingRomilCledoro100% (1)

- Module 3 Cost Volume Profit Analysis NA PDFDocument4 paginiModule 3 Cost Volume Profit Analysis NA PDFMadielyn Santarin Miranda50% (2)

- MAS MIDTERM EXAM 1ST SEM AY2017-18 - With AnswersDocument19 paginiMAS MIDTERM EXAM 1ST SEM AY2017-18 - With AnswersUy Samuel100% (1)

- Strategic Cost Management Coordinated Quiz 1Document7 paginiStrategic Cost Management Coordinated Quiz 1Kim TaehyungÎncă nu există evaluări

- MSQ-02 - Variable & Absorption Costing (Final)Document11 paginiMSQ-02 - Variable & Absorption Costing (Final)Kevin James Sedurifa OledanÎncă nu există evaluări

- Act102 Assessment2Document4 paginiAct102 Assessment2MohammadÎncă nu există evaluări

- Aatax 3Document1 paginăAatax 3ALMA MORENAÎncă nu există evaluări

- Partcorp 10Document1 paginăPartcorp 10ALMA MORENAÎncă nu există evaluări

- Cost Not Qualifying For Recognition (Expensed Immediately) : Order of Priority: 1) Fair Value of Property ReceivedDocument1 paginăCost Not Qualifying For Recognition (Expensed Immediately) : Order of Priority: 1) Fair Value of Property ReceivedALMA MORENAÎncă nu există evaluări

- Intbus 5Document1 paginăIntbus 5ALMA MORENAÎncă nu există evaluări

- Partcorp 11Document1 paginăPartcorp 11ALMA MORENAÎncă nu există evaluări

- Intbus 1Document1 paginăIntbus 1ALMA MORENAÎncă nu există evaluări

- Stratcost 5Document1 paginăStratcost 5ALMA MORENAÎncă nu există evaluări

- Partcorp 9Document1 paginăPartcorp 9ALMA MORENAÎncă nu există evaluări

- Partcorp 12Document1 paginăPartcorp 12ALMA MORENAÎncă nu există evaluări

- Recognition:: Property, Plant and Equipment (Pas 16)Document1 paginăRecognition:: Property, Plant and Equipment (Pas 16)ALMA MORENAÎncă nu există evaluări

- Partcorp 14Document1 paginăPartcorp 14ALMA MORENAÎncă nu există evaluări

- Partcorp 15Document1 paginăPartcorp 15ALMA MORENAÎncă nu există evaluări

- Intbus 4Document1 paginăIntbus 4ALMA MORENAÎncă nu există evaluări

- Intbus 2Document1 paginăIntbus 2ALMA MORENAÎncă nu există evaluări

- Intermed 1Document1 paginăIntermed 1ALMA MORENAÎncă nu există evaluări

- Ms 1Document1 paginăMs 1ALMA MORENAÎncă nu există evaluări

- Intermed3 4Document1 paginăIntermed3 4ALMA MORENAÎncă nu există evaluări

- Intbus 3Document1 paginăIntbus 3ALMA MORENAÎncă nu există evaluări

- Subsequent Measurement: Applicable To Government EntitiesDocument1 paginăSubsequent Measurement: Applicable To Government EntitiesALMA MORENAÎncă nu există evaluări

- Govt Ppe 5Document1 paginăGovt Ppe 5ALMA MORENAÎncă nu există evaluări

- Biological Assets Agricultural Produce Products That Are The Result of Processing After HarvestDocument1 paginăBiological Assets Agricultural Produce Products That Are The Result of Processing After HarvestALMA MORENAÎncă nu există evaluări

- Govt Agri 3Document1 paginăGovt Agri 3ALMA MORENAÎncă nu există evaluări

- Derecognition of Financial AssetsDocument1 paginăDerecognition of Financial AssetsALMA MORENAÎncă nu există evaluări

- Determination of Fair ValueDocument1 paginăDetermination of Fair ValueALMA MORENAÎncă nu există evaluări

- Govt Agri 1Document1 paginăGovt Agri 1ALMA MORENAÎncă nu există evaluări

- Investments: Type of Financial Asset Examples Initial Measurement Subsequent MeasurementDocument1 paginăInvestments: Type of Financial Asset Examples Initial Measurement Subsequent MeasurementALMA MORENAÎncă nu există evaluări

- Govt Agri 5Document1 paginăGovt Agri 5ALMA MORENAÎncă nu există evaluări

- Initial measurement and subsequent measurement of investmentsDocument2 paginiInitial measurement and subsequent measurement of investmentsALMA MORENAÎncă nu există evaluări

- Derivatives: Characteristics of A DerivativeDocument1 paginăDerivatives: Characteristics of A DerivativeALMA MORENAÎncă nu există evaluări

- Held-to-maturity investments amortizationDocument1 paginăHeld-to-maturity investments amortizationALMA MORENAÎncă nu există evaluări

- Edexcel Economics Unit 3 June 2010 Mark SchemeDocument16 paginiEdexcel Economics Unit 3 June 2010 Mark SchemeEkaterina MozloevaÎncă nu există evaluări

- Enagic Policies PDFDocument24 paginiEnagic Policies PDFNemie AndresÎncă nu există evaluări

- Sales Dialogue Template FinishedDocument6 paginiSales Dialogue Template FinishedSherlyn Acaba100% (1)

- Marketing of ServicesDocument8 paginiMarketing of ServicesShreya GoyalÎncă nu există evaluări

- The Coffee Corner Paper: Pick-Up & Read The Latest Edition at The Following Locations: RiddlesDocument4 paginiThe Coffee Corner Paper: Pick-Up & Read The Latest Edition at The Following Locations: Riddlesapi-123091552Încă nu există evaluări

- CRM TemplateDocument10 paginiCRM TemplateNipun TantiaÎncă nu există evaluări

- Principal of Business SBADocument18 paginiPrincipal of Business SBABla Bla100% (1)

- Joshua Kennon What Is A FranchiseDocument6 paginiJoshua Kennon What Is A FranchiseNico A. Cotzias Jr.Încă nu există evaluări

- Key sales responsibilities and preparation tacticsDocument19 paginiKey sales responsibilities and preparation tacticsJaehyun PeachÎncă nu există evaluări

- ACCT3610 - Week 4 Case Study - LucentDocument2 paginiACCT3610 - Week 4 Case Study - LucentMonica TrieuÎncă nu există evaluări

- Portfolio ManagementDocument81 paginiPortfolio ManagementPrakash ReddyÎncă nu există evaluări

- General ReportDocument128 paginiGeneral Reportsamson1190Încă nu există evaluări

- 22 Coca Cola Bottlers v. Dela CruzDocument3 pagini22 Coca Cola Bottlers v. Dela Cruzaudreydql5100% (1)

- Strategic Forces Shaping the US Steel IndustryDocument20 paginiStrategic Forces Shaping the US Steel Industrykahlil gibran 17100% (1)

- Tinplate Company of IndiaDocument17 paginiTinplate Company of IndiaZaheer NâqvîÎncă nu există evaluări

- Describe Briefly The Rights As A Hirer UnderDocument9 paginiDescribe Briefly The Rights As A Hirer UnderMika MellonÎncă nu există evaluări

- Managerial Economics Assignment AnalysisDocument8 paginiManagerial Economics Assignment AnalysissreetcÎncă nu există evaluări

- NIKE Presentation Slide EditDocument24 paginiNIKE Presentation Slide EditAtiQah NOtyhÎncă nu există evaluări

- 1.SCOPE OF SUPPLY:-Supply ofDocument6 pagini1.SCOPE OF SUPPLY:-Supply ofokman17Încă nu există evaluări

- Performing Strong by Docc HilfordDocument5 paginiPerforming Strong by Docc Hilfordwronged75% (4)

- List of Local Cable TV Channels in The NilgirisDocument7 paginiList of Local Cable TV Channels in The NilgirisApple AdsÎncă nu există evaluări

- Marketing Priciples & StrategiesDocument34 paginiMarketing Priciples & StrategiesMiguel Martinez0% (1)

- EntrepDocument31 paginiEntrepGaudie MoreÎncă nu există evaluări

- MS 07 SolvedDocument10 paginiMS 07 Solvedomshanker44Încă nu există evaluări

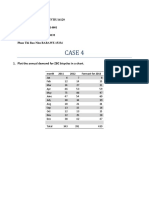

- Case 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334Document4 paginiCase 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334HuynhGiangÎncă nu există evaluări

- Six Categories of New Products and Innovation ProcessDocument19 paginiSix Categories of New Products and Innovation ProcessyodamÎncă nu există evaluări

- Transfer PricingDocument24 paginiTransfer PricingsaphaltapalveÎncă nu există evaluări

- Proposal - BingoDocument5 paginiProposal - BingoThejas MurthyÎncă nu există evaluări

- Product RealizationDocument226 paginiProduct RealizationSagar Coolkarni0% (1)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)De la EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Evaluare: 4.5 din 5 stele4.5/5 (12)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDe la EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindEvaluare: 5 din 5 stele5/5 (231)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetDe la EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetÎncă nu există evaluări

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)De la EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Evaluare: 4.5 din 5 stele4.5/5 (5)

- Profit First for Therapists: A Simple Framework for Financial FreedomDe la EverandProfit First for Therapists: A Simple Framework for Financial FreedomÎncă nu există evaluări

- Financial Accounting For Dummies: 2nd EditionDe la EverandFinancial Accounting For Dummies: 2nd EditionEvaluare: 5 din 5 stele5/5 (10)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!De la EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Evaluare: 4.5 din 5 stele4.5/5 (14)

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantDe la EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantEvaluare: 4.5 din 5 stele4.5/5 (146)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDe la EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesÎncă nu există evaluări

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyDe la EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyEvaluare: 5 din 5 stele5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDe la EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanEvaluare: 4.5 din 5 stele4.5/5 (79)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItDe la EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItEvaluare: 5 din 5 stele5/5 (13)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?De la EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Evaluare: 5 din 5 stele5/5 (1)

- Basic Accounting: Service Business Study GuideDe la EverandBasic Accounting: Service Business Study GuideEvaluare: 5 din 5 stele5/5 (2)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesDe la EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesEvaluare: 4.5 din 5 stele4.5/5 (30)

- Project Control Methods and Best Practices: Achieving Project SuccessDe la EverandProject Control Methods and Best Practices: Achieving Project SuccessÎncă nu există evaluări

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsDe la EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsEvaluare: 4 din 5 stele4/5 (7)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)De la EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Evaluare: 4 din 5 stele4/5 (33)

- Mysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungDe la EverandMysap Fi Fieldbook: Fi Fieldbuch Auf Der Systeme Anwendungen Und Produkte in Der DatenverarbeitungEvaluare: 4 din 5 stele4/5 (1)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDe la Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelÎncă nu există evaluări

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyDe la EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyEvaluare: 4 din 5 stele4/5 (4)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsDe la EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsÎncă nu există evaluări