S-ar putea să vă placă și

- LIBOR Role and Interest Rate SwapsDocument2 paginiLIBOR Role and Interest Rate SwapsWOP INVESTÎncă nu există evaluări

- Part 4Document26 paginiPart 4Silvia SlavkovaÎncă nu există evaluări

- Rate of Interest - Different ConceptsDocument18 paginiRate of Interest - Different ConceptsKarthik LakshminarayanÎncă nu există evaluări

- Demystifying Interest Rate SwapsDocument17 paginiDemystifying Interest Rate SwapsbionicturtleÎncă nu există evaluări

- Ch11 SolutionsDocument21 paginiCh11 SolutionsEno CasmiÎncă nu există evaluări

- Chapter 11Document23 paginiChapter 11sarahjohnsonÎncă nu există evaluări

- Fundamentals of Credit AnalysisDocument5 paginiFundamentals of Credit Analysiskazimeister1Încă nu există evaluări

- Bonds Decoded: Unraveling the Mystery Behind Bond MarketsDe la EverandBonds Decoded: Unraveling the Mystery Behind Bond MarketsÎncă nu există evaluări

- Chap007end of CHPTDocument5 paginiChap007end of CHPTAhmed ObaidÎncă nu există evaluări

- FinQuiz - Smart Summary - Study Session 16 - Reading 56Document7 paginiFinQuiz - Smart Summary - Study Session 16 - Reading 56Rafael100% (1)

- The Benefits and Risks of Corporate Bonds Oct - 13 - 2010 ReportDocument11 paginiThe Benefits and Risks of Corporate Bonds Oct - 13 - 2010 ReportstefijÎncă nu există evaluări

- What Is A Treasury BondDocument12 paginiWhat Is A Treasury Bondmorris yenenehÎncă nu există evaluări

- Chapter Four Credit Risk: Individual Loan RiskDocument22 paginiChapter Four Credit Risk: Individual Loan RiskMd NaeemÎncă nu există evaluări

- 10.pak Qfipme Topic1 Hfis 13 Leveraged LoansDocument4 pagini10.pak Qfipme Topic1 Hfis 13 Leveraged LoansNoodles FSAÎncă nu există evaluări

- Cove Lite LoansDocument7 paginiCove Lite LoansJGARD33Încă nu există evaluări

- High Yield Bond MarketDocument6 paginiHigh Yield Bond MarketYash RajgarhiaÎncă nu există evaluări

- Managing Financial RiskDocument36 paginiManaging Financial RisksharonulyssesÎncă nu există evaluări

- Impact of Interest Rates on Foreign Exchange, Equity & Debt Mutual FundsDocument9 paginiImpact of Interest Rates on Foreign Exchange, Equity & Debt Mutual FundsTariq MahmoodÎncă nu există evaluări

- Market: What The DebtDocument6 paginiMarket: What The DebtArpit GuptaÎncă nu există evaluări

- Fab - Ch05.manual.2006-Final 2Document28 paginiFab - Ch05.manual.2006-Final 2LauraÎncă nu există evaluări

- DebtDocument4 paginiDebtmeetwithsanjayÎncă nu există evaluări

- A Primer On Syndicated Term Loans PDFDocument4 paginiA Primer On Syndicated Term Loans PDFtrkhoa2002Încă nu există evaluări

- 2 - Debt and CovenantsDocument4 pagini2 - Debt and CovenantsVincenzo CassoneÎncă nu există evaluări

- What Does Credit Crisis Mean?Document14 paginiWhat Does Credit Crisis Mean?amardeeprocksÎncă nu există evaluări

- RR 5 (Corporate Laons)Document33 paginiRR 5 (Corporate Laons)Pranathi TallaÎncă nu există evaluări

- Mutual Fund EvaluationDocument21 paginiMutual Fund Evaluationsaravan1891Încă nu există evaluări

- BondsDocument10 paginiBondsGeorge William100% (1)

- 54556Document22 pagini54556rellimnojÎncă nu există evaluări

- Lending Institution in IndiaDocument24 paginiLending Institution in IndiaMann SainiÎncă nu există evaluări

- DebtCapitalMarkets TheBasics AsiaEditionDocument28 paginiDebtCapitalMarkets TheBasics AsiaEditionVivek AgÎncă nu există evaluări

- Corporate Bonds vs Bank Loans for Firm FundingDocument7 paginiCorporate Bonds vs Bank Loans for Firm FundingYssa MallenÎncă nu există evaluări

- Understanding Debentures: Key TakeawaysDocument8 paginiUnderstanding Debentures: Key TakeawaysRichard DuniganÎncă nu există evaluări

- Cost of Bank LoanDocument12 paginiCost of Bank LoanTokib TowfiqÎncă nu există evaluări

- Bond ChapterDocument30 paginiBond ChapterstarkeychicoÎncă nu există evaluări

- ch05 FinanceDocument30 paginich05 FinancePhil ArcoriaÎncă nu există evaluări

- Financial RisksDocument3 paginiFinancial RisksViz PrezÎncă nu există evaluări

- Banking Credit ManagementDocument7 paginiBanking Credit ManagementashwatinairÎncă nu există evaluări

- Case Study Solution - Speculation HedgersDocument5 paginiCase Study Solution - Speculation HedgersIlya BratenkovÎncă nu există evaluări

- Critical Financial Problems: 1. Volatility in Interest Rate and Its Impact On Bond PriceDocument2 paginiCritical Financial Problems: 1. Volatility in Interest Rate and Its Impact On Bond PriceKshitishÎncă nu există evaluări

- Credit Risk Mgmt. at ICICIDocument60 paginiCredit Risk Mgmt. at ICICIRikesh Daliya100% (1)

- Chapter 9 - Interest Rate and Currency Swaps (Q&A)Document5 paginiChapter 9 - Interest Rate and Currency Swaps (Q&A)Nuraisyahnadhirah MohamadtaibÎncă nu există evaluări

- Swap Risk Management ToolsDocument22 paginiSwap Risk Management ToolsMahveen KhurranaÎncă nu există evaluări

- Case For High Yield Sep 10Document6 paginiCase For High Yield Sep 10Yu ZhouÎncă nu există evaluări

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2De la EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2Încă nu există evaluări

- Allecks Juel R. Luchana Group No. 6 TTH 7:30Am-9:00Am The Crisis of CreditDocument3 paginiAllecks Juel R. Luchana Group No. 6 TTH 7:30Am-9:00Am The Crisis of CreditAllecks Juel LuchanaÎncă nu există evaluări

- Bank Financial Statements & Risk AnalysisDocument8 paginiBank Financial Statements & Risk AnalysisDương PhạmÎncă nu există evaluări

- Learn about interest rates, bonds, stocks valuation and risk assessmentDocument8 paginiLearn about interest rates, bonds, stocks valuation and risk assessmentLeslie OrgelÎncă nu există evaluări

- Liquidity Risk in BondsDocument3 paginiLiquidity Risk in BondsAanchal MahajanÎncă nu există evaluări

- Debt Capital Markets: The Basics For IssuersDocument28 paginiDebt Capital Markets: The Basics For Issuersvinaymathew100% (1)

- FIN2601-chapter 6Document28 paginiFIN2601-chapter 6Atiqa Aslam100% (1)

- Chapter Eleven Credit Risk: Individual Loan RiskDocument23 paginiChapter Eleven Credit Risk: Individual Loan RiskSandra SureshÎncă nu există evaluări

- Adjustable Rate MortgageDocument17 paginiAdjustable Rate MortgageMuhammad TamimÎncă nu există evaluări

- Risk Management in Banks EmergenceDocument63 paginiRisk Management in Banks EmergenceNagireddy KalluriÎncă nu există evaluări

- Scribd 2Document6 paginiScribd 2Angel NuevoÎncă nu există evaluări

- Seminar Presentation On::-Debt Instuments: - Structure of Intrest Rates in India: - Fixed Deposits: - Bond ValuationDocument20 paginiSeminar Presentation On::-Debt Instuments: - Structure of Intrest Rates in India: - Fixed Deposits: - Bond ValuationRavindra NimbalkarÎncă nu există evaluări

- ch14-Off-Balance Sheet ActivitiesDocument15 paginich14-Off-Balance Sheet ActivitiesYousif Agha100% (2)

- Fin 480 Exam2Document14 paginiFin 480 Exam2OpheliaNiuÎncă nu există evaluări

- 7-81 Last Pages Rupanshi CompleteDocument65 pagini7-81 Last Pages Rupanshi Completehimanshu.ahirwarfeaÎncă nu există evaluări

- Debt Markets Black Book RevisedDocument63 paginiDebt Markets Black Book RevisedPrasad Naik100% (1)

- General Research PDFDocument4 paginiGeneral Research PDFGeorge LernerÎncă nu există evaluări

- Edp Imp QuestionsDocument3 paginiEdp Imp QuestionsAshutosh SinghÎncă nu există evaluări

- Tax 2 - Midterm ExamDocument2 paginiTax 2 - Midterm ExamMichelle MatubisÎncă nu există evaluări

- Optional Credit RemovalDocument3 paginiOptional Credit RemovalKNOWLEDGE SOURCEÎncă nu există evaluări

- Your Account Summary: Airtel Number MR Bucha Reddy ADocument8 paginiYour Account Summary: Airtel Number MR Bucha Reddy AKothamasu PrasadÎncă nu există evaluări

- Topic 6 Stances On Economic Global IntegrationDocument43 paginiTopic 6 Stances On Economic Global IntegrationLady Edzelle Aliado100% (1)

- Monopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineDocument36 paginiMonopoly: Principles of Microeconomics Douglas Curtis & Ian IrvineNameÎncă nu există evaluări

- Mineral and Energy ResourcesDocument4 paginiMineral and Energy ResourcesJoseph ZotooÎncă nu există evaluări

- October 16, 2023 Philippine Stock ExchangeDocument5 paginiOctober 16, 2023 Philippine Stock ExchangePaul De CastroÎncă nu există evaluări

- Inter-regional disparities in industrial growthDocument100 paginiInter-regional disparities in industrial growthrks_rmrctÎncă nu există evaluări

- Portfolio Management - Chapter 7Document85 paginiPortfolio Management - Chapter 7Dr Rushen SinghÎncă nu există evaluări

- c6. Test 1. Listening. AnswerDocument5 paginic6. Test 1. Listening. AnswerLê VinhÎncă nu există evaluări

- Option To PurchaseDocument3 paginiOption To PurchaseAlberta Real EstateÎncă nu există evaluări

- CTM Tutorial 3Document4 paginiCTM Tutorial 3crsÎncă nu există evaluări

- NajmDocument2 paginiNajmAthar KhanÎncă nu există evaluări

- Book Building Process and Types ExplainedDocument15 paginiBook Building Process and Types ExplainedPoojaDesaiÎncă nu există evaluări

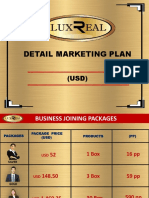

- Luxreal Detail Marketing Plan (2019) UsdDocument32 paginiLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Economic Impact of Accelerating Permit Local Development and Govt RevenuesDocument6 paginiEconomic Impact of Accelerating Permit Local Development and Govt RevenuesQQuestorÎncă nu există evaluări

- An Introduction To Private Sector Financing of Transportation InfrastructureDocument459 paginiAn Introduction To Private Sector Financing of Transportation InfrastructureBob DiamondÎncă nu există evaluări

- Hostile Takeover of Mindtree: An Analysis of Benefits and ChallengesDocument4 paginiHostile Takeover of Mindtree: An Analysis of Benefits and Challengesanuj rakheja100% (1)

- Bullock CartDocument23 paginiBullock CartsrajeceÎncă nu există evaluări

- Solutions: ECO 100Y Introduction To Economics Midterm Test # 2Document15 paginiSolutions: ECO 100Y Introduction To Economics Midterm Test # 2examkillerÎncă nu există evaluări

- Pre Test of Bahasa Inggris 21 - 9 - 2020Document5 paginiPre Test of Bahasa Inggris 21 - 9 - 2020magdalena sriÎncă nu există evaluări

- Schram y Pavlovskaya ED 2017 Rethinking Neoliberalism. Resisiting The Disciplinary Regime LIBRODocument285 paginiSchram y Pavlovskaya ED 2017 Rethinking Neoliberalism. Resisiting The Disciplinary Regime LIBROJessica ArgüelloÎncă nu există evaluări

- Exercises: Set B: Standard CustomDocument4 paginiExercises: Set B: Standard CustomMalik HamidÎncă nu există evaluări

- Bridge Over Bhagirathi AllotmentDocument6 paginiBridge Over Bhagirathi AllotmentKyle CruzÎncă nu există evaluări

- Radical Culture Research Collective - Nicolas BourriaudDocument3 paginiRadical Culture Research Collective - Nicolas BourriaudGwyddion FlintÎncă nu există evaluări

- The Impact of Colonialism On African Economic DevelopmentDocument13 paginiThe Impact of Colonialism On African Economic Developmentsulaiman yusufÎncă nu există evaluări

- Healthcare Industry in India PESTEL AnalysisDocument3 paginiHealthcare Industry in India PESTEL AnalysisAASHNA SOOD 1827228Încă nu există evaluări

- Aqa Econ2 QP Jan13Document16 paginiAqa Econ2 QP Jan13api-247036342Încă nu există evaluări

- Akpk SlideDocument13 paginiAkpk SlideizzatiÎncă nu există evaluări