S-ar putea să vă placă și

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Total 1 473 900.00 1 473 900.00Document4 paginiTotal 1 473 900.00 1 473 900.00Angela GarciaÎncă nu există evaluări

- KsebBill 1165411013809Document1 paginăKsebBill 1165411013809Jio CpyÎncă nu există evaluări

- Contract of LeaseDocument2 paginiContract of LeaseElain OrtizÎncă nu există evaluări

- Hanson CaseDocument14 paginiHanson CaseSanah Bijlani40% (5)

- Accounting: Page 1 of 3Document3 paginiAccounting: Page 1 of 3Laskar REAZÎncă nu există evaluări

- Business PlanDocument5 paginiBusiness PlanColegiul de Constructii din HincestiÎncă nu există evaluări

- Negotiable Instrument Act 1881Document29 paginiNegotiable Instrument Act 1881Anonymous WtjVcZCgÎncă nu există evaluări

- Islamic PawnbrokingDocument10 paginiIslamic PawnbrokingAwatif RamliÎncă nu există evaluări

- Question #1 of 25Document15 paginiQuestion #1 of 25ALL ROUNDÎncă nu există evaluări

- Screenshot 2021-06-22 at 12.21.23 PMDocument18 paginiScreenshot 2021-06-22 at 12.21.23 PMHarshad130Încă nu există evaluări

- Bala Raksha Bhavan Rent Not File DT 07.02.2020Document2 paginiBala Raksha Bhavan Rent Not File DT 07.02.2020District Child Protection Officer VikarabadÎncă nu există evaluări

- 24.4 SebiDocument30 pagini24.4 SebijashuramuÎncă nu există evaluări

- Bankin and Fin Law Relationship Between Bank and Its CustomersDocument6 paginiBankin and Fin Law Relationship Between Bank and Its CustomersPersephone WestÎncă nu există evaluări

- SIP Report OldDocument27 paginiSIP Report OldAbhishek rajÎncă nu există evaluări

- Blackbook Project On Merchant BankingDocument66 paginiBlackbook Project On Merchant BankingElton Andrade75% (12)

- 1ROF07100.024 INV-2611994RevDocument1 pagină1ROF07100.024 INV-2611994RevSiddiq Khan100% (1)

- Focus On Japan Risk Specialist Issue 7Document4 paginiFocus On Japan Risk Specialist Issue 7Megha JhanjiÎncă nu există evaluări

- Framework of Economic Resilience Analysis: From Enigma To Solution Proposals by Musoko KayembeDocument10 paginiFramework of Economic Resilience Analysis: From Enigma To Solution Proposals by Musoko KayembeKayembeÎncă nu există evaluări

- 21 VBHN-BTC 512873Document78 pagini21 VBHN-BTC 512873LET LEARN ABCÎncă nu există evaluări

- Complaint - Colorado Fire & Police Pension Vs CDN Banks CDOR ManipulationDocument100 paginiComplaint - Colorado Fire & Police Pension Vs CDN Banks CDOR ManipulationNationalObserverÎncă nu există evaluări

- APC Corporation Exercises Chapter 10Document5 paginiAPC Corporation Exercises Chapter 10AnnGabrielleUretaÎncă nu există evaluări

- Sustainable Pre Leased 06122019Document2 paginiSustainable Pre Leased 06122019vaibhav vermaÎncă nu există evaluări

- Quiz 1 2Document4 paginiQuiz 1 2UndebaynÎncă nu există evaluări

- AgreementtoLease Commercial ShortForm 511 PDFDocument3 paginiAgreementtoLease Commercial ShortForm 511 PDFtom75% (4)

- Subject: Welcome To Hero Fincorp Family Reference Your Used Car Loan Account No. Deo0Uc00100006379290Document4 paginiSubject: Welcome To Hero Fincorp Family Reference Your Used Car Loan Account No. Deo0Uc00100006379290Rimpa SenapatiÎncă nu există evaluări

- Paper 5 - Corporate & MGMT Acs MCQs Part 1 PDFDocument60 paginiPaper 5 - Corporate & MGMT Acs MCQs Part 1 PDFSeema NaharÎncă nu există evaluări

- PDFDocument1 paginăPDFKRUNAL ParmarÎncă nu există evaluări

- Insurance Bar Review New Code. 2014Document465 paginiInsurance Bar Review New Code. 2014Ed NerosaÎncă nu există evaluări

- Management SOPDocument12 paginiManagement SOPsparkle shresthaÎncă nu există evaluări

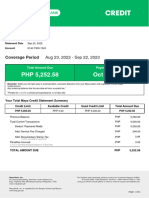

- MayaCredit SoA 2023SEPDocument3 paginiMayaCredit SoA 2023SEPjepoy palaruanÎncă nu există evaluări