S-ar putea să vă placă și

- Accounting MBA Sem I 2018Document4 paginiAccounting MBA Sem I 2018yogeshgharpureÎncă nu există evaluări

- Additional Questions 5Document13 paginiAdditional Questions 5Sanjay SiddharthÎncă nu există evaluări

- Xii AccDocument4 paginiXii AccSanjayÎncă nu există evaluări

- Proposed DividebdDocument34 paginiProposed DividebdPiyush SrivastavaÎncă nu există evaluări

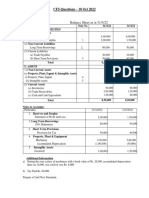

- CFS Questions - 18 - OCT - 2022Document5 paginiCFS Questions - 18 - OCT - 2022Kartik SujanÎncă nu există evaluări

- PART-B Analysis Test YtDocument8 paginiPART-B Analysis Test YtRiddhi GuptaÎncă nu există evaluări

- Solution:: Equity and LiabilitiesDocument4 paginiSolution:: Equity and LiabilitiesNIMROD MOCHAHARIÎncă nu există evaluări

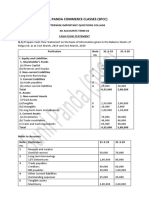

- Cash Flow StatementDocument10 paginiCash Flow Statementvsy9926Încă nu există evaluări

- Additional Illustrations-5Document19 paginiAdditional Illustrations-5goyalmanasvi06Încă nu există evaluări

- First Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20Document2 paginiFirst Model Test Paper Part - B Time: 40 Minutes Accountancy M.M. 20surbhi singhalÎncă nu există evaluări

- Imp QuestionDocument5 paginiImp QuestionKrish PaganiÎncă nu există evaluări

- AFM Assignment 2021Document7 paginiAFM Assignment 2021NARENDRA PATTELAÎncă nu există evaluări

- Accounts Important Questions by Rajat Jain SirDocument31 paginiAccounts Important Questions by Rajat Jain SirRajiv JhaÎncă nu există evaluări

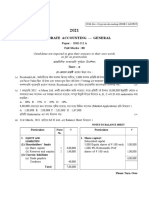

- CBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Document12 paginiCBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Sayantan DebnathÎncă nu există evaluări

- Revision Questions XiiDocument11 paginiRevision Questions XiiSahej Kaur AroraÎncă nu există evaluări

- Adobe Scan 05 Mar 2022Document5 paginiAdobe Scan 05 Mar 2022Titiksha Joshi100% (1)

- Cash Flow Statement Collage SPCC Term 2 PDFDocument11 paginiCash Flow Statement Collage SPCC Term 2 PDFTaaran ReddyÎncă nu există evaluări

- QP CODE: 22100973: Reg No: NameDocument6 paginiQP CODE: 22100973: Reg No: NameSajithaÎncă nu există evaluări

- 12 Accountancy Notes CH12 Cash Flow Statement 02Document28 pagini12 Accountancy Notes CH12 Cash Flow Statement 02Gourab GoraiÎncă nu există evaluări

- Cash Flow Statement Activity Wise 05-02-24Document7 paginiCash Flow Statement Activity Wise 05-02-24navyabindra28Încă nu există evaluări

- CAFM FULL SYLLABUS FREE TEST DEC 23-Executive-RevisionDocument7 paginiCAFM FULL SYLLABUS FREE TEST DEC 23-Executive-Revisionyogeetha saiÎncă nu există evaluări

- CFS 2023 PyqDocument15 paginiCFS 2023 PyqAnshul JainÎncă nu există evaluări

- Accountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Document3 paginiAccountancy Board Practical Paper - 2020-2021 Class - Xii Time: 1 Hour Max. Marks: 12Kairav KhuranaÎncă nu există evaluări

- Class 12 Accountancy CBSE Cash Flow StatementDocument7 paginiClass 12 Accountancy CBSE Cash Flow StatementSarvesh SreedharÎncă nu există evaluări

- Preparation of Financial Statements - QBDocument26 paginiPreparation of Financial Statements - QBHindutav arya100% (1)

- JayathDocument5 paginiJayathJayaprakash JayathÎncă nu există evaluări

- Adobe Scan 19 Mar 2024Document5 paginiAdobe Scan 19 Mar 2024anilarsha18Încă nu există evaluări

- Master Questions, Advance Level Questions and Additional Questions-Chapter 4Document18 paginiMaster Questions, Advance Level Questions and Additional Questions-Chapter 4manmeet0001Încă nu există evaluări

- Gujarat Technological UniversityDocument6 paginiGujarat Technological UniversitymansiÎncă nu există evaluări

- Acc Practical QuestionsDocument6 paginiAcc Practical QuestionsyogochkeÎncă nu există evaluări

- Financial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)Document5 paginiFinancial Reporting & Financial Statement Analysis Paper - Dse 6.1A FM - 80 Group - A (5x3 15)tanmoy sardarÎncă nu există evaluări

- Important QuestionsDocument3 paginiImportant QuestionsNayan JainÎncă nu există evaluări

- 12 DRT AccDocument2 pagini12 DRT AccDeeran DhayanithiRPÎncă nu există evaluări

- Management Accouting Assignment4 Manish Chauhan (09-1128) .Document17 paginiManagement Accouting Assignment4 Manish Chauhan (09-1128) .manishÎncă nu există evaluări

- Cash Flow Statement - 2Document9 paginiCash Flow Statement - 2Midhun PerozhiÎncă nu există evaluări

- B.B.A., Sem.-IV CC-213: Corporate Financial StatementsDocument4 paginiB.B.A., Sem.-IV CC-213: Corporate Financial StatementsJJ NayakÎncă nu există evaluări

- 4120504Document3 pagini4120504m_gadhvi6840Încă nu există evaluări

- Accounting For Decision Making or Management AU Question Paper'sDocument41 paginiAccounting For Decision Making or Management AU Question Paper'sAdhithiya dhanasekarÎncă nu există evaluări

- Cash Flow Statement of AmulDocument6 paginiCash Flow Statement of AmulArav Sarin60% (5)

- 232 FM AssignmentDocument17 pagini232 FM Assignmentbhupesh joshiÎncă nu există evaluări

- Siddharth Education Services LTDDocument5 paginiSiddharth Education Services LTDBasanta K SahuÎncă nu există evaluări

- Particulars Notes 31-3-2019 31-3-2018 I Equity and LiabilitiesDocument1 paginăParticulars Notes 31-3-2019 31-3-2018 I Equity and LiabilitiesBinoy TrevadiaÎncă nu există evaluări

- Sums On Cash Flow StatementDocument5 paginiSums On Cash Flow StatementAstha ParmanandkaÎncă nu există evaluări

- Management Accounitng - 104 (I)Document4 paginiManagement Accounitng - 104 (I)Rudraksh PareyÎncă nu există evaluări

- Cash Flow Statement Numericals QDocument3 paginiCash Flow Statement Numericals QDheeraj BholaÎncă nu există evaluări

- Cash Flow ProbDocument3 paginiCash Flow Probbimbee 13Încă nu există evaluări

- Net Working Capital Current Assets - Current LiabilitiesDocument11 paginiNet Working Capital Current Assets - Current LiabilitiesRahul YadavÎncă nu există evaluări

- Cash Flow Statement Problems PDFDocument32 paginiCash Flow Statement Problems PDFnsrivastav180% (30)

- DocumentDocument4 paginiDocumentTûshar ThakúrÎncă nu există evaluări

- Isc Mock 2Document14 paginiIsc Mock 2anshikajain3474Încă nu există evaluări

- Cash Flow Statement Test Paper IIDocument2 paginiCash Flow Statement Test Paper IIRaman SachdevaÎncă nu există evaluări

- CMA Final CFR MarathonDocument30 paginiCMA Final CFR MarathonRamanpreet KaurÎncă nu există evaluări

- Accounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Document6 paginiAccounting For Holding Co. (Lecture 3) : Total 12,00,000 6,00,000Michael JimÎncă nu există evaluări

- 12 Acs (S) - Set A 19.7.2021Document3 pagini12 Acs (S) - Set A 19.7.2021Sakshi NagotkarÎncă nu există evaluări

- Acc hw2Document5 paginiAcc hw2pujaadiÎncă nu există evaluări

- CR Assignemt Unit 3Document25 paginiCR Assignemt Unit 3Calida SoaresÎncă nu există evaluări

- 05 Corporate LiquidationDocument4 pagini05 Corporate LiquidationEric CauilanÎncă nu există evaluări

- Comparative Income StatementDocument12 paginiComparative Income StatementBISHAL ROYÎncă nu există evaluări

- Module 6 - Worksheet and Financial Statements Part IIDocument4 paginiModule 6 - Worksheet and Financial Statements Part IIMJ San Pedro100% (2)

- Equity Valuation: Models from Leading Investment BanksDe la EverandEquity Valuation: Models from Leading Investment BanksJan ViebigÎncă nu există evaluări

- Balance Sheet As Per New Schedule ViDocument11 paginiBalance Sheet As Per New Schedule ViVelayudham ThiyagarajanÎncă nu există evaluări

- Final-Project Mba HRDocument108 paginiFinal-Project Mba HRMaryam ali KazmiÎncă nu există evaluări

- Pfs Project WebinarDocument31 paginiPfs Project WebinarNeji HergliÎncă nu există evaluări

- Ink BUSINESS PLAN finalESTDocument15 paginiInk BUSINESS PLAN finalESTLKMs HUBÎncă nu există evaluări

- Working Capital Management 1Document21 paginiWorking Capital Management 1sbsÎncă nu există evaluări

- 2019-2020 Associations Income Tax Return - 2dec - 3PMDocument10 pagini2019-2020 Associations Income Tax Return - 2dec - 3PMMYO KO KOÎncă nu există evaluări

- SMC-SEC FORM 17-A (04.25.2022) Part 2-FINAL - RemovedDocument182 paginiSMC-SEC FORM 17-A (04.25.2022) Part 2-FINAL - RemovedJM MontanoÎncă nu există evaluări

- Merger Remedies GuideDocument48 paginiMerger Remedies GuidePhillip RichardsÎncă nu există evaluări

- Probate InventoryDocument4 paginiProbate Inventoryacer paulÎncă nu există evaluări

- Cranium Filament Reductions: Executive SummaryDocument15 paginiCranium Filament Reductions: Executive SummaryRegine IgnacioÎncă nu există evaluări

- FAC - Course OutlineDocument6 paginiFAC - Course OutlineJohn DoeÎncă nu există evaluări

- College of Business, Entrepreneurship and AccountancyDocument8 paginiCollege of Business, Entrepreneurship and AccountancyCherry Ann RoblesÎncă nu există evaluări

- Pengakun CH 09Document10 paginiPengakun CH 09nadia salsabilaÎncă nu există evaluări

- Corporate TaxationDocument82 paginiCorporate Taxationjayen0296755Încă nu există evaluări

- BL DeniseDocument10 paginiBL DeniseMaria Denise Belen SaclutiÎncă nu există evaluări

- Fundamental Accounting Principles: 17 Edition Larson Wild ChiappettaDocument42 paginiFundamental Accounting Principles: 17 Edition Larson Wild ChiappettaAnbuoli ParthasarathyÎncă nu există evaluări

- Format of Revised Schedule Vi To The Companies Act 1956 in ExcelDocument11 paginiFormat of Revised Schedule Vi To The Companies Act 1956 in Excelanshulagarwal62Încă nu există evaluări

- Statement of Financial Accounting Concepts No. 3Document64 paginiStatement of Financial Accounting Concepts No. 3andrejus0% (1)

- ICAEW - Accounting 2020 - Chap 2Document56 paginiICAEW - Accounting 2020 - Chap 2TRIEN DINH TIENÎncă nu există evaluări

- ACCA F3 Quiz QuestionDocument5 paginiACCA F3 Quiz QuestionA Muneeb Q100% (1)

- Government and Nonprofit Accounting Chapter 4Document12 paginiGovernment and Nonprofit Accounting Chapter 4Eyuel SintayehuÎncă nu există evaluări

- FAR.2910 - Wasting Assets.Document4 paginiFAR.2910 - Wasting Assets.Edmark LuspeÎncă nu există evaluări

- Course Material Development of Corporate Taxation: Prof. Deepak Sanghvi Mr. Rajesh Ganatra Ms. Bhoomi ParekhDocument41 paginiCourse Material Development of Corporate Taxation: Prof. Deepak Sanghvi Mr. Rajesh Ganatra Ms. Bhoomi ParekhbharatishethÎncă nu există evaluări

- Asset Accounting IssueDocument17 paginiAsset Accounting IssueAtulWalvekarÎncă nu există evaluări

- Cbse Class XII Accountancy Sample Paper - 1: I. Ii. IIIDocument224 paginiCbse Class XII Accountancy Sample Paper - 1: I. Ii. IIIAnubhav PareekÎncă nu există evaluări

- Preliminary Examination Reviewer: Intermediate Accounting 2 (Ca51010)Document11 paginiPreliminary Examination Reviewer: Intermediate Accounting 2 (Ca51010)Naomi SyÎncă nu există evaluări

- TOPIC 5. Investment IncomeDocument53 paginiTOPIC 5. Investment IncomeMadu maduÎncă nu există evaluări

- Solution Manual For College Accounting 22nd EditionDocument18 paginiSolution Manual For College Accounting 22nd EditionMichaelRamseydgjk100% (38)

- Return On Invested Capital - Michael Mauboussin On Investment ConceptsDocument8 paginiReturn On Invested Capital - Michael Mauboussin On Investment ConceptsJavi ToÎncă nu există evaluări

- April 2013 PDFDocument22 paginiApril 2013 PDFJasonSpringÎncă nu există evaluări