S-ar putea să vă placă și

- Methods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeDe la EverandMethods to Overcome the Financial and Money Transfer Blockade against Palestine and any Country Suffering from Financial BlockadeÎncă nu există evaluări

- Premier Diagnostic Health Services Inc. - Direct Registration (DRS) AdviceDocument6 paginiPremier Diagnostic Health Services Inc. - Direct Registration (DRS) AdviceIan N. TurnerÎncă nu există evaluări

- 853 Title Smart Document 02-04-19Document5 pagini853 Title Smart Document 02-04-19Kirsten Johnston EllesÎncă nu există evaluări

- EFTPS Payment ConfirmationDocument1 paginăEFTPS Payment ConfirmationJeffrey McGahrenÎncă nu există evaluări

- Credit Card Fraud Prevention Strategies A Complete Guide - 2021 EditionDe la EverandCredit Card Fraud Prevention Strategies A Complete Guide - 2021 EditionÎncă nu există evaluări

- SynchronyDocument11 paginiSynchronytestrun555100% (1)

- Apostille/Certificate of Authentication Request: Country Where Documents Will Be Used (Required)Document2 paginiApostille/Certificate of Authentication Request: Country Where Documents Will Be Used (Required)Joshua Gonsher100% (1)

- Asce Wire Instr CurrentDocument1 paginăAsce Wire Instr CurrentArunkumarÎncă nu există evaluări

- 55 - Gov - Uscourts.ord.124749.55.0Document4 pagini55 - Gov - Uscourts.ord.124749.55.0Freeman LawyerÎncă nu există evaluări

- 600 Technology Center Drive, Stoughton, MA 02072 Toll Free Phone #: 1-877-479-7577 Toll Free Fax #: 1-800-359-2884 Rev. 04/2017Document1 pagină600 Technology Center Drive, Stoughton, MA 02072 Toll Free Phone #: 1-877-479-7577 Toll Free Fax #: 1-800-359-2884 Rev. 04/2017Dorian GailliardÎncă nu există evaluări

- Open Warka Bank IraqDocument11 paginiOpen Warka Bank IraqaiesecÎncă nu există evaluări

- UP Holder Reporting ManualDocument22 paginiUP Holder Reporting ManualJay SingletonÎncă nu există evaluări

- New Balance $6,751.10 Payment Due Date 10/05/19: American Express Classic Gold CardDocument8 paginiNew Balance $6,751.10 Payment Due Date 10/05/19: American Express Classic Gold CardIrshad aliÎncă nu există evaluări

- Debt Collection 2014 Ohio 625Document14 paginiDebt Collection 2014 Ohio 625dwisselÎncă nu există evaluări

- Veale v. CITIBANK, F.S.B., 85 F.3d 577, 11th Cir. (1996)Document6 paginiVeale v. CITIBANK, F.S.B., 85 F.3d 577, 11th Cir. (1996)Scribd Government DocsÎncă nu există evaluări

- House Hearing, 112TH Congress - Hearing On Removing Social Security Numbers From Medicare CardsDocument112 paginiHouse Hearing, 112TH Congress - Hearing On Removing Social Security Numbers From Medicare CardsScribd Government Docs100% (1)

- Applying For SBA Disaster Loans (EIDL) : SBA Disaster Customer Service Center (800) 877-8339 Deaf or Hard-Of-HearingDocument34 paginiApplying For SBA Disaster Loans (EIDL) : SBA Disaster Customer Service Center (800) 877-8339 Deaf or Hard-Of-HearingMucho FacerapeÎncă nu există evaluări

- 77 - Gov - Uscourts.ord.124749.77.0Document4 pagini77 - Gov - Uscourts.ord.124749.77.0Freeman Lawyer100% (1)

- BankofAmericaCorporation 10KDocument241 paginiBankofAmericaCorporation 10KParul MitterÎncă nu există evaluări

- Sheila McCorriston WithdrawalDocument14 paginiSheila McCorriston WithdrawalAnonymous BmFjIMShq9100% (1)

- Remittance USDDocument1 paginăRemittance USDapi-3728250Încă nu există evaluări

- XXX-XX-0934: Daniels 9 1957Document7 paginiXXX-XX-0934: Daniels 9 1957luis gonzalezÎncă nu există evaluări

- SocSecAdm Form Ssa-711 Asking SSA For Record of SS-5 ApplicationDocument2 paginiSocSecAdm Form Ssa-711 Asking SSA For Record of SS-5 Applicationminutemancdc_scÎncă nu există evaluări

- Church of The Gardens and Property OwnerDocument23 paginiChurch of The Gardens and Property OwnerValerie LopezÎncă nu există evaluări

- Account ListDocument2.132 paginiAccount ListDark SightÎncă nu există evaluări

- 2018 Bond IssueDocument13 pagini2018 Bond Issuethe kingfishÎncă nu există evaluări

- DD 2887Document1 paginăDD 2887Jake JonesÎncă nu există evaluări

- Affidavit of Written Initial Uniformed Commercial Code Financing StatementDocument6 paginiAffidavit of Written Initial Uniformed Commercial Code Financing StatementYakub Dewaine beyÎncă nu există evaluări

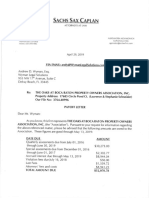

- Payoff Letter From Gonzalez, Counsel Sachs Sax Caplan For Oaks at Boca Raton Property Owners AssociationDocument4 paginiPayoff Letter From Gonzalez, Counsel Sachs Sax Caplan For Oaks at Boca Raton Property Owners Associationlarry-612445100% (1)

- Bank Seal: Demand Draft / Manager'S ChequeDocument2 paginiBank Seal: Demand Draft / Manager'S ChequeParveen KumarÎncă nu există evaluări

- Advanced Scenario 7: Quincy and Marian Pike (2017)Document10 paginiAdvanced Scenario 7: Quincy and Marian Pike (2017)Center for Economic Progress100% (1)

- DSTBoMGuhT9rFhxxnIFCbfB 1354528090573Document3 paginiDSTBoMGuhT9rFhxxnIFCbfB 1354528090573Kavitha RajendranÎncă nu există evaluări

- Us 1099 2022Document4 paginiUs 1099 2022mks12Încă nu există evaluări

- Temn Cert 2Document2 paginiTemn Cert 2smallcapsmarketÎncă nu există evaluări

- Oddo Brothers Cpas: William & Regina LittleDocument30 paginiOddo Brothers Cpas: William & Regina Littlebill littleÎncă nu există evaluări

- PNC Access Checking Account SummaryDocument2 paginiPNC Access Checking Account SummaryNiao PjÎncă nu există evaluări

- 2018-09-06 DOC Re Statement of Information (DSJ Real Estate Holdings, LLC)Document2 pagini2018-09-06 DOC Re Statement of Information (DSJ Real Estate Holdings, LLC)Doo Soo KimÎncă nu există evaluări

- Wage and Income - KULU - 101484197429Document2 paginiWage and Income - KULU - 101484197429Raymond KabutanoÎncă nu există evaluări

- CORRECTED (If Checked) : Payment Card and Third Party Network TransactionsDocument2 paginiCORRECTED (If Checked) : Payment Card and Third Party Network TransactionsROCIO menjivarÎncă nu există evaluări

- JK NoteDocument1 paginăJK NoteYarod YisraelÎncă nu există evaluări

- Colorado Application For Public Assistance (English)Document16 paginiColorado Application For Public Assistance (English)OSCAR SPENCER RAMIREZÎncă nu există evaluări

- Department of Justice V ITS Financial RulingDocument233 paginiDepartment of Justice V ITS Financial RulingKelly Phillips ErbÎncă nu există evaluări

- Litton Loan MERS AuthorizationDocument5 paginiLitton Loan MERS AuthorizationPhantoms001100% (1)

- Chime Spending Statement May 2023Document2 paginiChime Spending Statement May 2023Konami bossmanÎncă nu există evaluări

- Remittance AdviceDocument64 paginiRemittance Adviceoracleapps R12100% (1)

- Bank of America Statement Nov 2023 1Document9 paginiBank of America Statement Nov 2023 1raheemtimo1Încă nu există evaluări

- Show PDFDocument12 paginiShow PDFrita4444Încă nu există evaluări

- US Internal Revenue Service: f9325Document2 paginiUS Internal Revenue Service: f9325IRSÎncă nu există evaluări

- Wage and Income - PAGE - 104600922025Document3 paginiWage and Income - PAGE - 104600922025manuelkenzie10Încă nu există evaluări

- Your 2020 Social Security Cost of Living Increase 2019Document4 paginiYour 2020 Social Security Cost of Living Increase 2019henryÎncă nu există evaluări

- Insurance Dec Page-DummyDocument1 paginăInsurance Dec Page-DummyAjha DortchÎncă nu există evaluări

- Bank TR CodeDocument7 paginiBank TR CodeSanjivÎncă nu există evaluări

- American Express Amex Blue Cash EveryDay Card Benefits and AgreementDocument24 paginiAmerican Express Amex Blue Cash EveryDay Card Benefits and AgreementGreg JohnsonÎncă nu există evaluări

- How To Read Your RCN BillDocument1 paginăHow To Read Your RCN BillMiguel ÁngelÎncă nu există evaluări

- Direct DebitDocument2 paginiDirect DebitKylie Sheree WielandÎncă nu există evaluări

- 1 - Credit Card Validation Form .COM - enDocument2 pagini1 - Credit Card Validation Form .COM - enEljon Noel OrillosaÎncă nu există evaluări

- Articles of Incorporation NY Dos1511Document4 paginiArticles of Incorporation NY Dos1511asdfpoiuiiiiÎncă nu există evaluări

- Michael and Julie Mardock v. Michael and Virginia McClaughryDocument17 paginiMichael and Julie Mardock v. Michael and Virginia McClaughryThe Department of Official InformationÎncă nu există evaluări

- Verge LawsuitDocument21 paginiVerge LawsuitAnonymous NKPsAVw100% (1)

- Bitcoin ManipDocument89 paginiBitcoin ManipAnonymous NKPsAVwÎncă nu există evaluări

- Wright MotionDocument6 paginiWright MotionAnonymous NKPsAVwÎncă nu există evaluări

- Veritaseum Final JudgmentDocument19 paginiVeritaseum Final JudgmentAnonymous NKPsAVwÎncă nu există evaluări

- Kik Letter Motion Re DiscoveryDocument10 paginiKik Letter Motion Re DiscoveryAnonymous NKPsAVwÎncă nu există evaluări

- SEC Motion For JudgementDocument49 paginiSEC Motion For JudgementForkLogÎncă nu există evaluări

- R3 Trademark SuitDocument16 paginiR3 Trademark SuitAnonymous NKPsAVwÎncă nu există evaluări

- 7 Commissioner of Internal Revenue v. John Gotamco & Sons, Inc.Document6 pagini7 Commissioner of Internal Revenue v. John Gotamco & Sons, Inc.Vianice BaroroÎncă nu există evaluări

- 1927297165Document1 pagină1927297165Ayush SrivastavÎncă nu există evaluări

- Iesco Online BillDocument1 paginăIesco Online BillRaheel TariqÎncă nu există evaluări

- Nothing Phone (1) (Black, 128 GB) : Grand Total 27009.00Document1 paginăNothing Phone (1) (Black, 128 GB) : Grand Total 27009.00Rehan KahnÎncă nu există evaluări

- StatementOfAccount 6351700974 14112023 101336Document3 paginiStatementOfAccount 6351700974 14112023 101336sakthisundaresan36Încă nu există evaluări

- 2022 AllSlipsDocument3 pagini2022 AllSlipsAshley LehmanÎncă nu există evaluări

- Answer KeyDocument4 paginiAnswer KeyDynÎncă nu există evaluări

- GROUP 10 (Corporation Income Taxation - Regular Corporation)Document16 paginiGROUP 10 (Corporation Income Taxation - Regular Corporation)Denmark David Gaspar NatanÎncă nu există evaluări

- Chaseo: Beginning BalanceDocument1 paginăChaseo: Beginning BalanceAvalina LindaÎncă nu există evaluări

- Balance Sheet of NLC IndiaDocument8 paginiBalance Sheet of NLC IndiaSweety RoyÎncă nu există evaluări

- Uucms - Karnataka.gov - in ExamGeneral PrintExamApplicationDocument1 paginăUucms - Karnataka.gov - in ExamGeneral PrintExamApplicationb90451578Încă nu există evaluări

- Direct Tax Summary NotesDocument88 paginiDirect Tax Summary NotesAlisha LukeÎncă nu există evaluări

- Annex C RR 11-2018Document1 paginăAnnex C RR 11-2018Alyk CalionÎncă nu există evaluări

- Income Tax Ordinance 1984 - Amended Upto July 2022Document382 paginiIncome Tax Ordinance 1984 - Amended Upto July 2022Sumit GÎncă nu există evaluări

- Contoh Laporan Laba Rugi KoinWorksDocument1 paginăContoh Laporan Laba Rugi KoinWorksDiftya Twas Galih AtyasaÎncă nu există evaluări

- Cause - List HCDocument615 paginiCause - List HCPradheesh MalhotraÎncă nu există evaluări

- Christian Medical CollegeDocument1 paginăChristian Medical CollegesureshÎncă nu există evaluări

- Chapter 1 Introduction To Business Taxes PDFDocument6 paginiChapter 1 Introduction To Business Taxes PDFDudz Matienzo100% (1)

- Financial Inclusion Through Microfinance: Role of Financial Technology After Demonetization DriveDocument8 paginiFinancial Inclusion Through Microfinance: Role of Financial Technology After Demonetization DriveMuhammed Shafi MkÎncă nu există evaluări

- Assignment 2 MIS 207 1612631030Document6 paginiAssignment 2 MIS 207 1612631030shamim islam limonÎncă nu există evaluări

- Special Journals - Quiz 36Document8 paginiSpecial Journals - Quiz 36Joana TrinidadÎncă nu există evaluări

- Confirmation For Booking ID # 94140479 Check-In May 18 2016 PDFDocument1 paginăConfirmation For Booking ID # 94140479 Check-In May 18 2016 PDFAirilleÎncă nu există evaluări

- Monitor BillDocument1 paginăMonitor BillGulf JobsÎncă nu există evaluări

- Boat Bassheads 220 Wired Headset: Grand Total 524.00Document1 paginăBoat Bassheads 220 Wired Headset: Grand Total 524.00Dhawan KumarÎncă nu există evaluări

- Invoices of GTG ClientsDocument18 paginiInvoices of GTG ClientsJasanmeet SinghÎncă nu există evaluări

- Speech Delivered by Dr. Ernest Addison, Governor, at Launch of Payswitch Company LTDDocument8 paginiSpeech Delivered by Dr. Ernest Addison, Governor, at Launch of Payswitch Company LTDNana KofiÎncă nu există evaluări

- Accounting For Labor ExercisesDocument6 paginiAccounting For Labor ExercisesNichole Joy XielSera TanÎncă nu există evaluări

- CIR Vs Soriano TAX DigestDocument3 paginiCIR Vs Soriano TAX DigestGeorge PandaÎncă nu există evaluări

- Estmt - 2022 03 31Document12 paginiEstmt - 2022 03 31Laura MCGÎncă nu există evaluări

- Response of Pre-Bid Queries of The RFP For Financial Inclusion GatewayDocument72 paginiResponse of Pre-Bid Queries of The RFP For Financial Inclusion GatewayAndy_sumanÎncă nu există evaluări