S-ar putea să vă placă și

- 001dec052019 2 PDFDocument8 pagini001dec052019 2 PDFjdbejxbdbdjÎncă nu există evaluări

- 'Account StatementDocument11 pagini'Account StatementSikander Qazi100% (2)

- Donors TaxDocument83 paginiDonors TaxAndyvergys Aldrin MistulaÎncă nu există evaluări

- Sample Q&A On PEZADocument1 paginăSample Q&A On PEZAMichael Jim PolancosÎncă nu există evaluări

- AGENCYDocument20 paginiAGENCYJoshua CabinasÎncă nu există evaluări

- Inc Tax CGTDocument15 paginiInc Tax CGTace zero80% (5)

- Zain Traders Assignment 2Document2 paginiZain Traders Assignment 2Bilal Ahmed100% (1)

- Translation Invoice Template v3Document1 paginăTranslation Invoice Template v3ysÎncă nu există evaluări

- PDFDocument3 paginiPDFRojan BhattaraiÎncă nu există evaluări

- Accounting Methods And: Installment Reporting of IncomeDocument15 paginiAccounting Methods And: Installment Reporting of IncomeRoronoa ZoroÎncă nu există evaluări

- Exempt Sale of Goods Properties and Services NotesDocument2 paginiExempt Sale of Goods Properties and Services NotesSelene DimlaÎncă nu există evaluări

- Lifted From BAR Exam Questions & QuizzersDocument17 paginiLifted From BAR Exam Questions & QuizzersabcdefgÎncă nu există evaluări

- Tax Quiz 4Document61 paginiTax Quiz 4Seri CrisologoÎncă nu există evaluări

- 3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Document13 pagini3 Floor, Business & Engineering Building, Matina, Davao City Telefax: (082) 300-1496 Phone No.: (082) 244-34-00 Local 137Abigail Ann PasiliaoÎncă nu există evaluări

- CorporationDocument18 paginiCorporationSarah GoÎncă nu există evaluări

- TAXATION 2 Chapter 4 Estate Tax Deductions From Gross EstateDocument8 paginiTAXATION 2 Chapter 4 Estate Tax Deductions From Gross EstateKim Cristian MaañoÎncă nu există evaluări

- Inclusion and Exclusion of Gross Income Summary Review by ValenciaDocument6 paginiInclusion and Exclusion of Gross Income Summary Review by ValenciaMichael Pelingon Severo100% (1)

- Gross Income Deductions - Lecture Handout PDFDocument4 paginiGross Income Deductions - Lecture Handout PDFKarl RendonÎncă nu există evaluări

- T 2Document3 paginiT 2Corazon Lim LeeÎncă nu există evaluări

- Value Added TaxDocument8 paginiValue Added TaxErica VillaruelÎncă nu există evaluări

- Income Tax Reviewer Updated 0403Document99 paginiIncome Tax Reviewer Updated 0403quedan_socotÎncă nu există evaluări

- Under What Conditions May A Foreigner Be Allowed TDocument3 paginiUnder What Conditions May A Foreigner Be Allowed TANGELU RANE BAGARES INTOLÎncă nu există evaluări

- Taxn03B: Transfer and Business TaxesDocument18 paginiTaxn03B: Transfer and Business TaxesKerby GripoÎncă nu există evaluări

- Business and Transfer Reviewer CompressDocument11 paginiBusiness and Transfer Reviewer CompressMarko JerichoÎncă nu există evaluări

- Theories Chapter 1Document16 paginiTheories Chapter 1Farhana GuiandalÎncă nu există evaluări

- Final Income TaxationDocument15 paginiFinal Income TaxationElizalen MacarilayÎncă nu există evaluări

- Income Taxation Ind PracticeDocument3 paginiIncome Taxation Ind PracticeJanine Tividad100% (1)

- Gains or Losses in Dealings in PropertyDocument6 paginiGains or Losses in Dealings in PropertyRussel RuizÎncă nu există evaluări

- Input:Output Tax ReviewerDocument2 paginiInput:Output Tax ReviewerHiedi SugamotoÎncă nu există evaluări

- Final Income TaxationDocument4 paginiFinal Income TaxationJean Diane Jovelo100% (1)

- 1.1 MC - Exercises On Estate Tax (PRTC)Document8 pagini1.1 MC - Exercises On Estate Tax (PRTC)marco poloÎncă nu există evaluări

- Tax 101 Exclusions To Gross Income PDFDocument25 paginiTax 101 Exclusions To Gross Income PDFJade Berlyn AgcaoiliÎncă nu există evaluări

- HQ01 General Principles of TaxationDocument12 paginiHQ01 General Principles of TaxationRenzo RamosÎncă nu există evaluări

- Afar 2019Document9 paginiAfar 2019TakuriÎncă nu există evaluări

- Tariff and Customs Code of The Philippines - Test BankDocument3 paginiTariff and Customs Code of The Philippines - Test BankTyrelle CastilloÎncă nu există evaluări

- 89 07 Gross IncomeDocument9 pagini89 07 Gross IncomeNah HamzaÎncă nu există evaluări

- CTDI Final Pre-Board Special Laws Only PDFDocument4 paginiCTDI Final Pre-Board Special Laws Only PDFPatricia Marie MercaderÎncă nu există evaluări

- 1.1 MC - Exercises On Estate Tax (PRTC)Document8 pagini1.1 MC - Exercises On Estate Tax (PRTC)marco poloÎncă nu există evaluări

- Taxation Sia/Tabag TAX.2814-Community Tax MAY 2020: Lecture Notes A. IndividualsDocument1 paginăTaxation Sia/Tabag TAX.2814-Community Tax MAY 2020: Lecture Notes A. IndividualsMay Grethel Joy PeranteÎncă nu există evaluări

- Incometaxation1 PDFDocument543 paginiIncometaxation1 PDFmae annÎncă nu există evaluări

- Introduction To Estate TaxDocument71 paginiIntroduction To Estate TaxMiko ArniñoÎncă nu există evaluări

- Taxation of Fringe Benefits: (Art 212, Labor Code)Document7 paginiTaxation of Fringe Benefits: (Art 212, Labor Code)Lyca VÎncă nu există evaluări

- Partnership Law Atty. Macmod: Multiple ChoiceDocument10 paginiPartnership Law Atty. Macmod: Multiple ChoiceJomarÎncă nu există evaluări

- University of Perpetual Help System DaltaDocument9 paginiUniversity of Perpetual Help System DaltaJeanette LampitocÎncă nu există evaluări

- CHAPTER 11 Compensation IncomeDocument15 paginiCHAPTER 11 Compensation IncomeGIRLÎncă nu există evaluări

- Income Recognition, Measurement and Reporting and Taxpayer ClassificationsDocument27 paginiIncome Recognition, Measurement and Reporting and Taxpayer ClassificationsAries Queencel Bernante BocarÎncă nu există evaluări

- Taxation Module 3 5Document57 paginiTaxation Module 3 5Ma VyÎncă nu există evaluări

- BFINMAX Handout - Gross Profit Variance AnalysisDocument6 paginiBFINMAX Handout - Gross Profit Variance AnalysisDeo CoronaÎncă nu există evaluări

- 1st Semester Transfer Taxation Module 1 Succession and Transfer TaxDocument5 pagini1st Semester Transfer Taxation Module 1 Succession and Transfer TaxNah HamzaÎncă nu există evaluări

- INTGR TAX 009 DeductionsDocument6 paginiINTGR TAX 009 DeductionsJohn Paul SiodacalÎncă nu există evaluări

- October 2010 Business Law & Taxation Final Pre-BoardDocument9 paginiOctober 2010 Business Law & Taxation Final Pre-BoardPatrick ArazoÎncă nu există evaluări

- TAX.2814 Community-Taxes AnswersDocument1 paginăTAX.2814 Community-Taxes AnswersCams DlunaÎncă nu există evaluări

- General Principles of TaxationDocument17 paginiGeneral Principles of TaxationJericho Pedragosa33% (3)

- TAX Final-PB FEUDocument9 paginiTAX Final-PB FEUkarim abitagoÎncă nu există evaluări

- Ampongan Chap 2Document1 paginăAmpongan Chap 2iamjan_101Încă nu există evaluări

- Estate Tax Activities (Questions)Document4 paginiEstate Tax Activities (Questions)Christine Nathalie BalmesÎncă nu există evaluări

- Allowable Deductions Part 1Document3 paginiAllowable Deductions Part 1John Rich GamasÎncă nu există evaluări

- QUIZ in AUDIT OF SHAREHOLDERS EQUITYDocument2 paginiQUIZ in AUDIT OF SHAREHOLDERS EQUITYLugh Tuatha DeÎncă nu există evaluări

- Quiz4-Responsibilityacctg TP BalscoreDocument5 paginiQuiz4-Responsibilityacctg TP BalscoreRambell John RodriguezÎncă nu există evaluări

- Tax MockboardDocument8 paginiTax MockboardJaneÎncă nu există evaluări

- TTTDocument6 paginiTTTAngelika BalmeoÎncă nu există evaluări

- PDF Valix Theory of PDF Valix Theory of Accounts AccountsDocument2 paginiPDF Valix Theory of PDF Valix Theory of Accounts AccountsPhilip Dan Jayson LarozaÎncă nu există evaluări

- TAXATION 2 Chapter 5 Estate Tax Payable PDFDocument5 paginiTAXATION 2 Chapter 5 Estate Tax Payable PDFKim Cristian MaañoÎncă nu există evaluări

- Accounting Review: TaxationDocument3 paginiAccounting Review: TaxationPatriciaÎncă nu există evaluări

- AFARDocument15 paginiAFARBetchelyn Dagwayan BenignosÎncă nu există evaluări

- Items of Gross Income Subject To RegularDocument2 paginiItems of Gross Income Subject To Regularhannah drew ovejasÎncă nu există evaluări

- Standard CostingDocument11 paginiStandard Costingace zeroÎncă nu există evaluări

- Franchise p3Document4 paginiFranchise p3ace zeroÎncă nu există evaluări

- MAS MidtermDocument6 paginiMAS Midtermace zeroÎncă nu există evaluări

- Int AssetDocument21 paginiInt Assetace zeroÎncă nu există evaluări

- Quiz p2Document6 paginiQuiz p2ace zeroÎncă nu există evaluări

- p2 Home OfficeDocument9 paginip2 Home Officeace zeroÎncă nu există evaluări

- Developing Our Future Professionals - Cross-Cultural Dialogues in The Workplace - LCC and HCC Characteristics EHall PDFDocument1 paginăDeveloping Our Future Professionals - Cross-Cultural Dialogues in The Workplace - LCC and HCC Characteristics EHall PDFace zeroÎncă nu există evaluări

- Q19 - Audit Procedures, Evidence and DocumentationDocument7 paginiQ19 - Audit Procedures, Evidence and Documentationace zero0% (1)

- Statements 3Document69 paginiStatements 3ace zeroÎncă nu există evaluări

- Intermediate Examination: Suggested Answers To QuestionsDocument21 paginiIntermediate Examination: Suggested Answers To Questionsace zeroÎncă nu există evaluări

- Rit ExclusionDocument21 paginiRit Exclusionace zeroÎncă nu există evaluări

- Scanned by CamscannerDocument4 paginiScanned by Camscannerace zeroÎncă nu există evaluări

- PromoDocument1 paginăPromoace zeroÎncă nu există evaluări

- Scanned by CamscannerDocument9 paginiScanned by Camscannerace zeroÎncă nu există evaluări

- Account Statement PDFDocument2 paginiAccount Statement PDFHshÎncă nu există evaluări

- Client Prepaid Form: Customer InformationDocument2 paginiClient Prepaid Form: Customer InformationTony GaryÎncă nu există evaluări

- GSI ISSMGE Membership Form 2020-2021Document1 paginăGSI ISSMGE Membership Form 2020-2021marketing_925862570Încă nu există evaluări

- JDE TransportDocument24 paginiJDE TransportsivaÎncă nu există evaluări

- Sol. Man. - Chapter 8 - Adjusting EntriesDocument11 paginiSol. Man. - Chapter 8 - Adjusting EntriesPerdito John Vin100% (3)

- Books of Himanshu JournalDocument4 paginiBooks of Himanshu Journalrakesh19865Încă nu există evaluări

- CMTADocument36 paginiCMTAPisto PalubosÎncă nu există evaluări

- 5 Disbursements 1Document199 pagini5 Disbursements 1John Karl Mabini100% (1)

- BCA Fee Slip 210728 65182 11012023Document1 paginăBCA Fee Slip 210728 65182 11012023Sohail KarimÎncă nu există evaluări

- Hospital AccountingDocument477 paginiHospital Accountingnicevenu100% (1)

- Supply Chain Management1Document1 paginăSupply Chain Management1Nilabjo Kanti Paul100% (1)

- TermsDocument1 paginăTermsedÎncă nu există evaluări

- Consolidation Warehousing 2Document25 paginiConsolidation Warehousing 2sanjeev kumarÎncă nu există evaluări

- U) HZFT CF - SM8"DF// 0 F.JZ sJU"v#f VG (58Fjf/F LCTGL Ju"V$Gl Vgi Huifvmgl EztlDocument22 paginiU) HZFT CF - SM8"DF// 0 F.JZ sJU"v#f VG (58Fjf/F LCTGL Ju"V$Gl Vgi Huifvmgl Eztlparesh4trivediÎncă nu există evaluări

- Tax 2 Sample Problem SolvingDocument2 paginiTax 2 Sample Problem SolvingAlberto NicholsÎncă nu există evaluări

- Telephone Number 08041265428 User Id 08085453679 - KKDocument3 paginiTelephone Number 08041265428 User Id 08085453679 - KKSurya RÎncă nu există evaluări

- Auditing Expenditure CycleDocument7 paginiAuditing Expenditure CycleHannaj May De GuzmanÎncă nu există evaluări

- Consolidated Tax1 Finals Exam R Complete CLEANDocument12 paginiConsolidated Tax1 Finals Exam R Complete CLEANHi Law SchoolÎncă nu există evaluări

- Ship To: Ship Via: Beckett Use Only: Your Name: - Account #Document2 paginiShip To: Ship Via: Beckett Use Only: Your Name: - Account #Hearthstone apprenticeÎncă nu există evaluări

- Gulshan Weaving Mills Limited: 1-Sales and Receivables ChecklistDocument4 paginiGulshan Weaving Mills Limited: 1-Sales and Receivables ChecklistirfanÎncă nu există evaluări

- Hindustan Petroleum Corporation Limited Direct Sales Office 130/1, Sarojini Devi Street, Secunderabad - 500 003Document1 paginăHindustan Petroleum Corporation Limited Direct Sales Office 130/1, Sarojini Devi Street, Secunderabad - 500 00379LiterÎncă nu există evaluări

- SAP SD Consignment Sales Process.Document2 paginiSAP SD Consignment Sales Process.praveennbsÎncă nu există evaluări

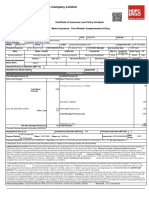

- HDFC ERGO General Insurance Company Limited: Policy No. 2312 1002 1642 6400 000Document5 paginiHDFC ERGO General Insurance Company Limited: Policy No. 2312 1002 1642 6400 000YATINDER DAHIYAÎncă nu există evaluări

- GST Challan PDFDocument2 paginiGST Challan PDFNicks N NIckÎncă nu există evaluări