S-ar putea să vă placă și

- The Balanced Scorecard: Turn your data into a roadmap to successDe la EverandThe Balanced Scorecard: Turn your data into a roadmap to successEvaluare: 3.5 din 5 stele3.5/5 (4)

- Polytechnic University of The Philippines: Review of Literature and StudiesDocument40 paginiPolytechnic University of The Philippines: Review of Literature and StudiesCayla Mae CarlosÎncă nu există evaluări

- Balance ScorecardDocument20 paginiBalance Scorecardfiqry_afiq90Încă nu există evaluări

- The Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)De la EverandThe Balanced Scorecard (Review and Analysis of Kaplan and Norton's Book)Evaluare: 4.5 din 5 stele4.5/5 (3)

- Balanced Scorecard 5Document44 paginiBalanced Scorecard 5Cicy AmbookenÎncă nu există evaluări

- Balanced Score CardDocument19 paginiBalanced Score CardAamirx64Încă nu există evaluări

- Advance Ma AssignmentDocument9 paginiAdvance Ma AssignmentKavitha MarappanÎncă nu există evaluări

- Q.7. (A) Explain The Concept of "Balance Score Card". A N S - The Balance Score Card Is A Management System (Not Only A Measurement System) ThatDocument5 paginiQ.7. (A) Explain The Concept of "Balance Score Card". A N S - The Balance Score Card Is A Management System (Not Only A Measurement System) ThatL PatelÎncă nu există evaluări

- Project Report AnshulDocument25 paginiProject Report AnshulAnshul GoelÎncă nu există evaluări

- KPIDocument15 paginiKPIrmmmehta100% (1)

- A Study On Balance Scorecard and Its Implementation On Herbal StrategiDocument10 paginiA Study On Balance Scorecard and Its Implementation On Herbal StrategiGrety Nischala MÎncă nu există evaluări

- Balanced Score CardDocument19 paginiBalanced Score CardIwora AgaraÎncă nu există evaluări

- PCM Term PaperDocument22 paginiPCM Term Paper8130089011Încă nu există evaluări

- Balanced Scorecard: A ReportDocument10 paginiBalanced Scorecard: A ReportKhushboo RajÎncă nu există evaluări

- Review of The LiteratureDocument3 paginiReview of The LiteratureNatasha ClarenceÎncă nu există evaluări

- The 4 Perspectives of The Balanced ScorecardDocument6 paginiThe 4 Perspectives of The Balanced Scorecardnivedita patilÎncă nu există evaluări

- Balanced Scorecard and Its Importance in Legal FirmDocument17 paginiBalanced Scorecard and Its Importance in Legal FirmRashi GuptaÎncă nu există evaluări

- Balanced ScorecardDocument5 paginiBalanced ScorecardFlorentia FarahroziÎncă nu există evaluări

- New Dimension in Management and Post Review of Budget.: National SeminarDocument13 paginiNew Dimension in Management and Post Review of Budget.: National Seminarminal bhojaniÎncă nu există evaluări

- BSC ExampleDocument3 paginiBSC ExampleVinayak PatilÎncă nu există evaluări

- Balanced Scorecard for Performance MeasurementDe la EverandBalanced Scorecard for Performance MeasurementEvaluare: 3 din 5 stele3/5 (2)

- Balanced Scorecard AssignmentDocument14 paginiBalanced Scorecard AssignmentNike Alabi100% (7)

- How to Enhance Productivity Under Cost Control, Quality Control as Well as Time, in a Private or Public OrganizationDe la EverandHow to Enhance Productivity Under Cost Control, Quality Control as Well as Time, in a Private or Public OrganizationÎncă nu există evaluări

- Translating Strategy into Shareholder Value: A Company-Wide Approach to Value CreationDe la EverandTranslating Strategy into Shareholder Value: A Company-Wide Approach to Value CreationÎncă nu există evaluări

- Balanced ScorecardDocument12 paginiBalanced ScorecardBuket PedersenÎncă nu există evaluări

- Using Balance Scorecard in Educational InstitutionsDocument8 paginiUsing Balance Scorecard in Educational InstitutionsinventionjournalsÎncă nu există evaluări

- Sa Novdec08 Morgan PDFDocument3 paginiSa Novdec08 Morgan PDFGadaa BirmajiiÎncă nu există evaluări

- Balanced ScorecardDocument11 paginiBalanced ScorecardmottebossÎncă nu există evaluări

- LECTURE Balanced ScorecardDocument5 paginiLECTURE Balanced ScorecardL PatelÎncă nu există evaluări

- Balance Score Card: Made By:-Virender Singh SahuDocument17 paginiBalance Score Card: Made By:-Virender Singh SahuVirender Singh SahuÎncă nu există evaluări

- A Review of Balanced Scorecard Framework in Higher Education Institution (Heis)Document10 paginiA Review of Balanced Scorecard Framework in Higher Education Institution (Heis)GabrielGarciaOrjuelaÎncă nu există evaluări

- Ch. 3 Measuring Organizational EffectivenessDocument8 paginiCh. 3 Measuring Organizational EffectivenessDyahAyuRatnaCantikaÎncă nu există evaluări

- Jurnal Balanced ScorecardDocument13 paginiJurnal Balanced ScorecardIekar 'Fhai'100% (1)

- Assignment TwoDocument3 paginiAssignment TwoCharles MachuvaireÎncă nu există evaluări

- ASP AppD2Document2 paginiASP AppD2Farwi PhuravhathuÎncă nu există evaluări

- Rada College-Kombolcha Campus Department of Accounting and FinanceDocument5 paginiRada College-Kombolcha Campus Department of Accounting and FinanceabateÎncă nu există evaluări

- Balance ScorecardDocument10 paginiBalance ScorecardPalak MakkaÎncă nu există evaluări

- Balanced ScorecardDocument36 paginiBalanced ScorecardleesadzebondeÎncă nu există evaluări

- A Balanced Scorecard For Small BusinessDocument22 paginiA Balanced Scorecard For Small BusinessFeri100% (1)

- Transforming The Balanced Scorecard From Performance Measurement To Strategic ManagementMHDocument3 paginiTransforming The Balanced Scorecard From Performance Measurement To Strategic ManagementMHVirencarpediemÎncă nu există evaluări

- IsoraiteDocument11 paginiIsoraiteuser44448605Încă nu există evaluări

- HR Score CardDocument12 paginiHR Score CardKAVIVARMA R KÎncă nu există evaluări

- Balanced Score Card PDFDocument14 paginiBalanced Score Card PDFtyoafsÎncă nu există evaluări

- Balanced Scorecard: (1) The Financial PerspectiveDocument3 paginiBalanced Scorecard: (1) The Financial PerspectiveS. M. Zamirul IslamÎncă nu există evaluări

- Balance ScorecardDocument4 paginiBalance ScorecardMariam MahmoodÎncă nu există evaluări

- Balanced Scorecard PDFDocument11 paginiBalanced Scorecard PDFDeluchabelle E-garagesaleÎncă nu există evaluări

- Final BSC Manual 10.18FDocument61 paginiFinal BSC Manual 10.18FLeAshliÎncă nu există evaluări

- The Measures of Success: Developing A Balanced Scorecard To Measure PerformanceDocument22 paginiThe Measures of Success: Developing A Balanced Scorecard To Measure PerformanceChris LukamaÎncă nu există evaluări

- Balance Scorecard SummaryDocument4 paginiBalance Scorecard Summarywasi_aliÎncă nu există evaluări

- Performance Evaluation Through Balanced ScorecardDocument52 paginiPerformance Evaluation Through Balanced Scorecardyuvraj_bhujbalÎncă nu există evaluări

- The Performance Appraisal Tool Kit: Redesigning Your Performance Review Template to Drive Individual and Organizational ChangeDe la EverandThe Performance Appraisal Tool Kit: Redesigning Your Performance Review Template to Drive Individual and Organizational ChangeÎncă nu există evaluări

- Strategic ManagementDocument17 paginiStrategic ManagementCTJACÎncă nu există evaluări

- Feasibility Study of Implementing Balance Scorecard at IffcoDocument23 paginiFeasibility Study of Implementing Balance Scorecard at Iffcosachinabda100% (1)

- Balanced Scorecard: Basics: The Balanced Scorecard Is A Strategic Planning and Management System That Is UsedDocument4 paginiBalanced Scorecard: Basics: The Balanced Scorecard Is A Strategic Planning and Management System That Is Usedprakar2Încă nu există evaluări

- Balanced Scorecard For AIESECDocument15 paginiBalanced Scorecard For AIESECsandrolourencoÎncă nu există evaluări

- CHK-154 Implementing The Balanced ScorecardDocument6 paginiCHK-154 Implementing The Balanced ScorecardSofiya BayraktarovaÎncă nu există evaluări

- Assignment On BSCDocument18 paginiAssignment On BSCKomalJindalÎncă nu există evaluări

- Assignment On BSCDocument18 paginiAssignment On BSCginnz66Încă nu există evaluări

- Maternal and Child Nursing QuestionsDocument2 paginiMaternal and Child Nursing QuestionsCayla Mae CarlosÎncă nu există evaluări

- Volleyball: VOLLEYBALL Is A Competitive Sport. Athletes Can Enjoy It Better If They Play With ProfessionalDocument5 paginiVolleyball: VOLLEYBALL Is A Competitive Sport. Athletes Can Enjoy It Better If They Play With ProfessionalCayla Mae CarlosÎncă nu există evaluări

- Population Education of The Philippines: Carlos, Cayla Mae Nepomuceno, Clark Roncal, Meriel BSN 2-CDocument37 paginiPopulation Education of The Philippines: Carlos, Cayla Mae Nepomuceno, Clark Roncal, Meriel BSN 2-CCayla Mae Carlos100% (1)

- 1 N-109 MCN 2 LEC Syllabus (2 S, AY 19-20) REVISED PDFDocument7 pagini1 N-109 MCN 2 LEC Syllabus (2 S, AY 19-20) REVISED PDFCayla Mae CarlosÎncă nu există evaluări

- The Global EconomyDocument2 paginiThe Global EconomyCayla Mae CarlosÎncă nu există evaluări

- PE BasketballDocument12 paginiPE BasketballCayla Mae CarlosÎncă nu există evaluări

- COVIDcasepositiveDocument2 paginiCOVIDcasepositiveKrishna JandhyalaÎncă nu există evaluări

- Nursing Info Unit I To IIIDocument6 paginiNursing Info Unit I To IIICayla Mae CarlosÎncă nu există evaluări

- TCW ActivityDocument1 paginăTCW ActivityCayla Mae CarlosÎncă nu există evaluări

- Bosh (So1) HulmaDocument3 paginiBosh (So1) HulmaCayla Mae CarlosÎncă nu există evaluări

- Asian Regionalism ReportDocument22 paginiAsian Regionalism ReportCayla Mae Carlos100% (1)

- Nursing Info Unit I To IIIDocument6 paginiNursing Info Unit I To IIICayla Mae CarlosÎncă nu există evaluări

- The CorporationDocument2 paginiThe CorporationCayla Mae CarlosÎncă nu există evaluări

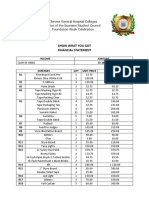

- Show What You GotDocument3 paginiShow What You GotCayla Mae CarlosÎncă nu există evaluări

- Nursing Info AbstractDocument11 paginiNursing Info AbstractCayla Mae CarlosÎncă nu există evaluări

- Awarding CeremonyDocument1 paginăAwarding CeremonyCayla Mae CarlosÎncă nu există evaluări

- Chloes AssignmenyDocument4 paginiChloes AssignmenyCayla Mae CarlosÎncă nu există evaluări

- Received 1375421425991991Document1 paginăReceived 1375421425991991Cayla Mae CarlosÎncă nu există evaluări

- NifedipineDocument3 paginiNifedipineNovi YulianaÎncă nu există evaluări

- Elpidio QuirinoDocument15 paginiElpidio QuirinoCayla Mae CarlosÎncă nu există evaluări

- TCW Readings GuideDocument4 paginiTCW Readings GuideRose Ann AriolaÎncă nu există evaluări

- Asian Regionalism ReportDocument22 paginiAsian Regionalism ReportCayla Mae Carlos100% (1)

- TCW ActivityDocument1 paginăTCW ActivityCayla Mae CarlosÎncă nu există evaluări

- Lecture 2-Small Business ManagementDocument108 paginiLecture 2-Small Business ManagementCayla Mae CarlosÎncă nu există evaluări

- Pierre de Fermat Charles Hermite: ContributionsDocument8 paginiPierre de Fermat Charles Hermite: ContributionsCayla Mae CarlosÎncă nu există evaluări

- Appendix 42 - Instructions - LDDAP-ADADocument2 paginiAppendix 42 - Instructions - LDDAP-ADATesa GD67% (3)

- Appendix 42 - Instructions - LDDAP-ADADocument2 paginiAppendix 42 - Instructions - LDDAP-ADATesa GD67% (3)

- Assessment Diagnosis Planning Intervention Rationale Evaluation Short Term GoalDocument2 paginiAssessment Diagnosis Planning Intervention Rationale Evaluation Short Term GoalCayla Mae CarlosÎncă nu există evaluări

- Maraming Tubig at Kakain NG Prutas para Makadumi Ako."Document2 paginiMaraming Tubig at Kakain NG Prutas para Makadumi Ako."Cayla Mae CarlosÎncă nu există evaluări

- DemoDocument5 paginiDemoCayla Mae CarlosÎncă nu există evaluări

- Project Report On Entrepreneurial Journey of A Local EntrepreneurDocument12 paginiProject Report On Entrepreneurial Journey of A Local EntrepreneurSai KishanÎncă nu există evaluări

- Running Head: MARKETING PLAN 1Document21 paginiRunning Head: MARKETING PLAN 1Isba RafiqueÎncă nu există evaluări

- Case Study On Business Model Adopted by The Pogo Travels: Abu Sufiyan 151GCMD006 R V Institute of ManagementDocument12 paginiCase Study On Business Model Adopted by The Pogo Travels: Abu Sufiyan 151GCMD006 R V Institute of ManagementSUFIYANÎncă nu există evaluări

- Information Sheet: Lending Company - Head OfficeDocument4 paginiInformation Sheet: Lending Company - Head OfficesakilogicÎncă nu există evaluări

- Ubaf 1Document6 paginiUbaf 1ivecita27Încă nu există evaluări

- CMS Introduction To Measures ManagementDocument27 paginiCMS Introduction To Measures ManagementiggybauÎncă nu există evaluări

- International Business: by Charles W.L. HillDocument17 paginiInternational Business: by Charles W.L. HillAshok SharmaÎncă nu există evaluări

- Session 31Document25 paginiSession 31Yashwanth Reddy AnumulaÎncă nu există evaluări

- QUIZ 1 Absorption CostingDocument1 paginăQUIZ 1 Absorption CostingJohn Carlo CruzÎncă nu există evaluări

- Accounting VoucherDocument2 paginiAccounting VoucherRavanan v.sÎncă nu există evaluări

- Contract of Sale of GoodsDocument18 paginiContract of Sale of GoodsManoj KumarÎncă nu există evaluări

- The 16 Career ClustersDocument4 paginiThe 16 Career ClusterssanchezromanÎncă nu există evaluări

- AIS Chapter 1Document8 paginiAIS Chapter 1Laurie Mae ToledoÎncă nu există evaluări

- Department of Education: Republic of The PhilippinesDocument2 paginiDepartment of Education: Republic of The PhilippinesKatrina SalasÎncă nu există evaluări

- AVT McCormick-R-26032018Document7 paginiAVT McCormick-R-26032018Siddharth DamaniÎncă nu există evaluări

- Unit 1Document38 paginiUnit 1Varsha SinghÎncă nu există evaluări

- Alliecovello ResumeDocument2 paginiAlliecovello Resumeapi-310731929Încă nu există evaluări

- Food Safety Culture Module BrochureDocument8 paginiFood Safety Culture Module Brochurejamil voraÎncă nu există evaluări

- Competency Model BooksDocument4 paginiCompetency Model Bookshoa quynh anhÎncă nu există evaluări

- Notice of 103rd AGM of Britannia Industries LimitedDocument20 paginiNotice of 103rd AGM of Britannia Industries LimitedSag SagÎncă nu există evaluări

- Distribution Network DesignDocument18 paginiDistribution Network DesignAnik AlamÎncă nu există evaluări

- Matrix Report Guideline - 2 PDFDocument27 paginiMatrix Report Guideline - 2 PDFPradeep GautamÎncă nu există evaluări

- Modern Systems Analysis and Design: Structuring System Process RequirementsDocument45 paginiModern Systems Analysis and Design: Structuring System Process RequirementsBhavikDaveÎncă nu există evaluări

- Responsibilities and Functional Areas of A Business HandoutDocument4 paginiResponsibilities and Functional Areas of A Business HandoutKerine Williams-FigaroÎncă nu există evaluări

- Q&A InvestorDocument2 paginiQ&A Investorjns1992Încă nu există evaluări

- Entry Strategies: Exporting Contractual Entry Modes Foreign Direct Investment (Document10 paginiEntry Strategies: Exporting Contractual Entry Modes Foreign Direct Investment (DianaProEraÎncă nu există evaluări

- Pas 38Document7 paginiPas 38elle friasÎncă nu există evaluări

- Chapter 4 - Part 1Document14 paginiChapter 4 - Part 1billtanÎncă nu există evaluări

- Corporate FinanceDocument7 paginiCorporate FinanceMit BakhdaÎncă nu există evaluări

- Assignment 1:: Student Name: Le Vu Anh Thu Student Number: 20431216 Wordcount: 1634 WordsDocument5 paginiAssignment 1:: Student Name: Le Vu Anh Thu Student Number: 20431216 Wordcount: 1634 WordsAnh Thư Lê VũÎncă nu există evaluări