S-ar putea să vă placă și

- 07audit of PPEDocument9 pagini07audit of PPEJeanette FormenteraÎncă nu există evaluări

- Chapter 8 Quiz - InventoriesDocument8 paginiChapter 8 Quiz - InventoriesDarleen CantiladoÎncă nu există evaluări

- Bond Valuation Exam 1Document2 paginiBond Valuation Exam 1Ronah Abigail BejocÎncă nu există evaluări

- Week 4 - Lesson 4 Cash and Cash EquivalentsDocument21 paginiWeek 4 - Lesson 4 Cash and Cash EquivalentsRose RaboÎncă nu există evaluări

- Partnership ExercisesDocument2 paginiPartnership ExercisesKoreangelica ChipeÎncă nu există evaluări

- MidtermsDocument8 paginiMidtermsRhea BadanaÎncă nu există evaluări

- Ia 2 Finals AnswersDocument1 paginăIa 2 Finals AnswersErica VillaruelÎncă nu există evaluări

- Land and BuildingDocument5 paginiLand and BuildingDianna DayawonÎncă nu există evaluări

- Apino Jan Dave T. BSA 4-1 QuizDocument14 paginiApino Jan Dave T. BSA 4-1 QuizRosemarie RamosÎncă nu există evaluări

- Diagnostic Exercises2Document32 paginiDiagnostic Exercises2HanaÎncă nu există evaluări

- Midterm Examination AnswersDocument3 paginiMidterm Examination AnswersMilani Joy LazoÎncă nu există evaluări

- Parcor ExamDocument2 paginiParcor ExamRose Ann GarciaÎncă nu există evaluări

- Multiple Choice:: Solution 21-1 Answer CDocument5 paginiMultiple Choice:: Solution 21-1 Answer Cleshz zynÎncă nu există evaluări

- 6902 - Investment Property and Other InvestmentDocument3 pagini6902 - Investment Property and Other InvestmentAljur SalamedaÎncă nu există evaluări

- Balance SheetDocument18 paginiBalance SheetAndriaÎncă nu există evaluări

- Investments AssignmentDocument3 paginiInvestments AssignmentKhai Supleo PabelicoÎncă nu există evaluări

- FAR FPB With Answer KeysDocument16 paginiFAR FPB With Answer KeysPj ManezÎncă nu există evaluări

- P2 BautistaDocument8 paginiP2 BautistaMedalla NikkoÎncă nu există evaluări

- Quiz 1B - Cash and Cash Equivalents, Bank ReconciliationDocument9 paginiQuiz 1B - Cash and Cash Equivalents, Bank ReconciliationLorence IbañezÎncă nu există evaluări

- Foreign Currency Transactions2021 3Document6 paginiForeign Currency Transactions2021 3Sheira Mae GuzmanÎncă nu există evaluări

- CASH QuestionsDocument9 paginiCASH QuestionsKenncyÎncă nu există evaluări

- Notes PayableDocument4 paginiNotes PayableShilla Mae BalanceÎncă nu există evaluări

- Chap16 ProblemsDocument20 paginiChap16 ProblemsYen YenÎncă nu există evaluări

- Problems: Problem 4 - 1Document4 paginiProblems: Problem 4 - 1KioÎncă nu există evaluări

- Chapter 6C 2 24 Ex 26 PB 54Document5 paginiChapter 6C 2 24 Ex 26 PB 54ruqayya muhammedÎncă nu există evaluări

- PartnershipDocument27 paginiPartnershipkrys_elleÎncă nu există evaluări

- SPOUSES ANTONIO BELTRAN AND FELISA BELTRAN, Petitioners, v. SPOUSES APOLONIO CANGAYDA, JR. AND LORETA E. CANGAYDADocument6 paginiSPOUSES ANTONIO BELTRAN AND FELISA BELTRAN, Petitioners, v. SPOUSES APOLONIO CANGAYDA, JR. AND LORETA E. CANGAYDARIZZA MAE OLANOÎncă nu există evaluări

- Business CombinationDocument3 paginiBusiness CombinationNicoleÎncă nu există evaluări

- Accounting For Special Transactions Partnership AccountingDocument15 paginiAccounting For Special Transactions Partnership AccountingJessaÎncă nu există evaluări

- Answer Key Far Assessment Questionairre 1Document22 paginiAnswer Key Far Assessment Questionairre 1Johnfree VallinasÎncă nu există evaluări

- Business Cup Level 1 Quiz BeeDocument28 paginiBusiness Cup Level 1 Quiz BeeRowellPaneloSalapareÎncă nu există evaluări

- Exclusions and Inclusions - MANTUANODocument8 paginiExclusions and Inclusions - MANTUANODonita MantuanoÎncă nu există evaluări

- Acctg201 IntroductionDocument10 paginiAcctg201 Introductionaaron manacapÎncă nu există evaluări

- Module 1 Notes and Loans ReceivableDocument21 paginiModule 1 Notes and Loans ReceivableEryn GabrielleÎncă nu există evaluări

- Conversion ProblemsDocument6 paginiConversion ProblemsAce Maynard DiancoÎncă nu există evaluări

- BLTDocument4 paginiBLTJaylord PidoÎncă nu există evaluări

- Set A Leases Problem SERANADocument6 paginiSet A Leases Problem SERANASherri BonquinÎncă nu există evaluări

- Solutions 11 18Document7 paginiSolutions 11 18Ariel LusaresÎncă nu există evaluări

- Which Statement Is Incorrect Regarding The Application of The Equity Method of Accounting For Investments in AssociatesDocument1 paginăWhich Statement Is Incorrect Regarding The Application of The Equity Method of Accounting For Investments in Associatesjahnhannalei marticio0% (1)

- LTCC AnswerDocument4 paginiLTCC AnswerRhina MagnawaÎncă nu există evaluări

- Chapter 2 Cash and Cash Equivalents Exercises T3AY2021Document7 paginiChapter 2 Cash and Cash Equivalents Exercises T3AY2021Carl Vincent BarituaÎncă nu există evaluări

- ACC117-CON09 Module 3 ExamDocument16 paginiACC117-CON09 Module 3 ExamMarlon LadesmaÎncă nu există evaluări

- Examination About Investment 1Document3 paginiExamination About Investment 1BLACKPINKLisaRoseJisooJennieÎncă nu există evaluări

- 6809 Accounts ReceivableDocument2 pagini6809 Accounts ReceivableEsse Valdez0% (1)

- Cash and Cash Equivalents QuizDocument2 paginiCash and Cash Equivalents QuizMarkJoven Bergantin100% (1)

- SimexDocument3 paginiSimexRoland Ron BantilanÎncă nu există evaluări

- Ia3 Review On Notes To FSDocument11 paginiIa3 Review On Notes To FSErich Posillo AranasÎncă nu există evaluări

- Ppe Post TestDocument31 paginiPpe Post TestMarie MagallanesÎncă nu există evaluări

- Accounts Receivable and Estimation of AFBDDocument1 paginăAccounts Receivable and Estimation of AFBDeia aieÎncă nu există evaluări

- Submissions - B-BLAW211 Law On Obligations and Contracts BSA21 1S AY20-21 - DLSU-D College - GSDocument3 paginiSubmissions - B-BLAW211 Law On Obligations and Contracts BSA21 1S AY20-21 - DLSU-D College - GSChesca AlonÎncă nu există evaluări

- 2nd Sem 2021 Acctg 5a NCADocument7 pagini2nd Sem 2021 Acctg 5a NCARUNEL J. PACOTÎncă nu există evaluări

- Shaine Andrea P. Sabiña Project 1st HalfDocument15 paginiShaine Andrea P. Sabiña Project 1st HalfNicole Anne Santiago SibuloÎncă nu există evaluări

- Semi Final Exam AE23Document6 paginiSemi Final Exam AE23HotcheeseramyeonÎncă nu există evaluări

- Mock 3 FARDocument10 paginiMock 3 FARRodelLaborÎncă nu există evaluări

- Partnership Accounting - Paula GozunDocument8 paginiPartnership Accounting - Paula GozunPaupauÎncă nu există evaluări

- Computation For Formation of PartnershipDocument10 paginiComputation For Formation of PartnershipErille Julianne (Rielianne)Încă nu există evaluări

- Solution Manual Ch. 1 19Document55 paginiSolution Manual Ch. 1 19Aira Mae TaborÎncă nu există evaluări

- Quiz 1 Lump Sum Liquidation Answer Key PeresDocument7 paginiQuiz 1 Lump Sum Liquidation Answer Key PeresChelit LadylieGirl FernandezÎncă nu există evaluări

- FAR 1 Reviewer AnswerDocument27 paginiFAR 1 Reviewer AnswerZace Hayo100% (1)

- FAR 1 Reviewer AnswerDocument27 paginiFAR 1 Reviewer AnswerMary Joy CabilÎncă nu există evaluări

- 02 ReceivablesDocument3 pagini02 ReceivablesRenz Angel M. RiveraÎncă nu există evaluări

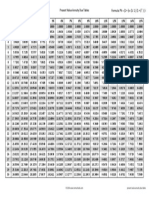

- Present Value Annuity Due TablesDocument1 paginăPresent Value Annuity Due TablesDecereen Pineda Rodrigueza100% (2)

- Accounting QuestionDocument40 paginiAccounting QuestionMohsinRazaÎncă nu există evaluări

- Single Entry FormulasDocument3 paginiSingle Entry FormulasDexter DeeÎncă nu există evaluări

- Ho BRDocument3 paginiHo BRSummer Star33% (3)

- Introduction PR3Document6 paginiIntroduction PR3Decereen Pineda RodriguezaÎncă nu există evaluări

- 04 InvestmentsDocument3 pagini04 InvestmentsVan TaeÎncă nu există evaluări

- Ias 16 Property Plant and Equipment Summary PDFDocument8 paginiIas 16 Property Plant and Equipment Summary PDFPuneeth DhondaleÎncă nu există evaluări

- TESDA Circular No. 002-2019 - Schedule of CostDocument22 paginiTESDA Circular No. 002-2019 - Schedule of CostGazza Bimar DimalantaÎncă nu există evaluări

- 02 ReceivablesDocument3 pagini02 ReceivablesRenz Angel M. RiveraÎncă nu există evaluări

- Problems Audit of Shareholdersx27 Equitydocx PDFDocument23 paginiProblems Audit of Shareholdersx27 Equitydocx PDFRaisa GeleraÎncă nu există evaluări

- The Emergence of Consensus: A Primer: ReviewDocument13 paginiThe Emergence of Consensus: A Primer: ReviewDecereen Pineda RodriguezaÎncă nu există evaluări

- Bookkeeping NC IIIDocument73 paginiBookkeeping NC IIILonAtanacio82% (11)

- PPEDocument3 paginiPPEDecereen Pineda RodriguezaÎncă nu există evaluări

- PPEDocument3 paginiPPEDecereen Pineda RodriguezaÎncă nu există evaluări

- Problems On SHEDocument2 paginiProblems On SHEDecereen Pineda RodriguezaÎncă nu există evaluări

- Chapter 5 Accounting For Merchandising OperationsDocument15 paginiChapter 5 Accounting For Merchandising OperationsDecereen Pineda RodriguezaÎncă nu există evaluări

- Sa Sept10 Ias16Document7 paginiSa Sept10 Ias16Muiz QureshiÎncă nu există evaluări

- Extrinsic and Intrinsic Factors Influencing Employee Motivation: Lessons From AMREF Health Africa in KenyaDocument12 paginiExtrinsic and Intrinsic Factors Influencing Employee Motivation: Lessons From AMREF Health Africa in KenyaDecereen Pineda RodriguezaÎncă nu există evaluări

- Problems On Retained EarningsDocument2 paginiProblems On Retained EarningsDecereen Pineda RodriguezaÎncă nu există evaluări

- The Intermediate Accounting Series Volume 2 2016 Empleo Robles SolmanDocument86 paginiThe Intermediate Accounting Series Volume 2 2016 Empleo Robles SolmanSutnek Isly94% (17)

- Chapter 12 FinalDocument19 paginiChapter 12 FinalMichael Hu100% (1)

- Module 17 - Property, Plant and Equipment: Iasc Foundation: Training Material For The Ifrs For SmesDocument44 paginiModule 17 - Property, Plant and Equipment: Iasc Foundation: Training Material For The Ifrs For SmesEphreen Grace MartyÎncă nu există evaluări

- Chap 013Document21 paginiChap 013Intal XDÎncă nu există evaluări

- African Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryDocument52 paginiAfrican Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryDecereen Pineda Rodrigueza100% (1)

- IFRS in Your Pocket 2019 PDFDocument116 paginiIFRS in Your Pocket 2019 PDFzahid hameedÎncă nu există evaluări

- Safe FoodDocument45 paginiSafe FoodDecereen Pineda RodriguezaÎncă nu există evaluări

- The Emergence of Consensus: A Primer: ReviewDocument13 paginiThe Emergence of Consensus: A Primer: ReviewDecereen Pineda RodriguezaÎncă nu există evaluări

- African Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryDocument52 paginiAfrican Swine Fever: Pesti Porcine Africaine, Peste Porcina Africana, Maladie de MontgomeryDecereen Pineda Rodrigueza100% (1)

- Far 2 Exercise 5 Page 286Document5 paginiFar 2 Exercise 5 Page 286Kay HispanoÎncă nu există evaluări

- Computerised Accounting SystemDocument196 paginiComputerised Accounting SystemSaiqua Parveen100% (2)

- Annual Report 2017Document158 paginiAnnual Report 2017speedenquiryÎncă nu există evaluări

- Champion CattlefarmsDocument24 paginiChampion Cattlefarmsshaniah1475% (4)

- "Kotak Mahindra Bank Q2FY21 Earnings Conference Call": October 26, 2020Document24 pagini"Kotak Mahindra Bank Q2FY21 Earnings Conference Call": October 26, 2020divya mÎncă nu există evaluări

- W8 TutorialSolutionsDocument12 paginiW8 TutorialSolutionsCJÎncă nu există evaluări

- 67-2-1 AccountancyDocument27 pagini67-2-1 AccountancytejÎncă nu există evaluări

- Notes-INTERM 2-Module 4-Depletion of Natural ResourcesDocument3 paginiNotes-INTERM 2-Module 4-Depletion of Natural ResourcesLeonoramarie BernosÎncă nu există evaluări

- Advance Accounting - LUPISAN-CHAPTER 3 PDFDocument25 paginiAdvance Accounting - LUPISAN-CHAPTER 3 PDFATLASÎncă nu există evaluări

- Q2 - Week 7 8Document4 paginiQ2 - Week 7 8Winston MurphyÎncă nu există evaluări

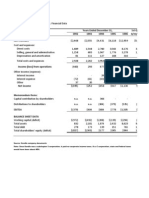

- Exhibit 1 Kendle International Inc. Financial Data Years Ended December 31Document12 paginiExhibit 1 Kendle International Inc. Financial Data Years Ended December 31Kito Minying ChenÎncă nu există evaluări

- Fa I MidDocument7 paginiFa I MidFãhâd Õró ÂhmédÎncă nu există evaluări

- FAR1 - Lecture 01 The Accounting EquationDocument5 paginiFAR1 - Lecture 01 The Accounting EquationPatricia Camille AustriaÎncă nu există evaluări

- Case Study #2: Growing PainsDocument13 paginiCase Study #2: Growing PainsTricia Ann Jungco Maquirang100% (1)

- Chapter8-WCMgt-working CapitalDocument28 paginiChapter8-WCMgt-working CapitalLefty Renewang0% (1)

- Salapa P M I ChartDocument2 paginiSalapa P M I ChartGelo MoloÎncă nu există evaluări

- What Is A Balance Sheet AuditDocument6 paginiWhat Is A Balance Sheet AuditSOMOSCOÎncă nu există evaluări

- CSEC POA June 2017 P2Document23 paginiCSEC POA June 2017 P2Britaney Reid100% (1)

- IAS 7 - Grand Thornton PDFDocument36 paginiIAS 7 - Grand Thornton PDFrisxaÎncă nu există evaluări

- Lahore School of Economics. Advance Corporate Finance. MBA II - Winter 2014. Dr. Sohail ZafarDocument6 paginiLahore School of Economics. Advance Corporate Finance. MBA II - Winter 2014. Dr. Sohail Zafarsarakhan0622Încă nu există evaluări

- JP Morgan Financial StatementsDocument8 paginiJP Morgan Financial StatementsTamar PirtskhalaishviliÎncă nu există evaluări

- Model Test Paper-2 (Ans.) (21.3.2023)Document18 paginiModel Test Paper-2 (Ans.) (21.3.2023)SihecÎncă nu există evaluări

- Study of Debt MarketDocument199 paginiStudy of Debt Marketbhar4tp0% (1)

- ACC XI SEE QP For RevisionDocument31 paginiACC XI SEE QP For Revisionvarshitha reddyÎncă nu există evaluări

- TEST BANK For Government and Not For Profit Accounting Concepts and Practices 6th Edition by Granof Khumawala20190702 86031 1d2i3lg PDFDocument16 paginiTEST BANK For Government and Not For Profit Accounting Concepts and Practices 6th Edition by Granof Khumawala20190702 86031 1d2i3lg PDFMaria Ceth SerranoÎncă nu există evaluări

- 5769 - Toa Test Bank 74Document12 pagini5769 - Toa Test Bank 74Rod Lester de GuzmanÎncă nu există evaluări

- Acc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)Document1 paginăAcc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)nicole bancoroÎncă nu există evaluări

- ch10 PDFDocument9 paginich10 PDFcris lu salemÎncă nu există evaluări

- WaterPlant ProjectDocument18 paginiWaterPlant ProjectYogesh Dhandharia0% (1)

- Basic Accounting ExamDocument8 paginiBasic Accounting ExamMikaela SalvadorÎncă nu există evaluări