S-ar putea să vă placă și

- Pretrial Process FlowDocument1 paginăPretrial Process FlowMosarah AltÎncă nu există evaluări

- Banking and AMLADocument26 paginiBanking and AMLAMosarah AltÎncă nu există evaluări

- 2021 Schedule of Preweek LecturesDocument1 pagină2021 Schedule of Preweek LecturesMarcky MarionÎncă nu există evaluări

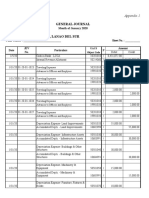

- General Journal: Appendix 1Document5 paginiGeneral Journal: Appendix 1Mosarah AltÎncă nu există evaluări

- Rights of The AccusedDocument13 paginiRights of The AccusedLorebeth EspañaÎncă nu există evaluări

- Tax Case Digests CompilationDocument207 paginiTax Case Digests CompilationFrancis Ray Arbon Filipinas83% (24)

- Tax Case Digests CompilationDocument207 paginiTax Case Digests CompilationFrancis Ray Arbon Filipinas83% (24)

- LectureDocument25 paginiLectureMarieÎncă nu există evaluări

- Politicsl LawDocument91 paginiPoliticsl LawMosarah AltÎncă nu există evaluări

- Tax DigestsDocument13 paginiTax DigestsMosarah AltÎncă nu există evaluări

- Civil Law Compilation Bar Q&a 1990-2017 PDFDocument380 paginiCivil Law Compilation Bar Q&a 1990-2017 PDFReynaldo Yu100% (10)

- Abad Vs PhilcomsatDocument2 paginiAbad Vs PhilcomsatFiels GamboaÎncă nu există evaluări

- Metropolitan Bank Vs Wilfred ChiokDocument1 paginăMetropolitan Bank Vs Wilfred ChiokMosarah AltÎncă nu există evaluări

- Equitable PCI Vs TanDocument2 paginiEquitable PCI Vs TanMosarah AltÎncă nu există evaluări

- Salazar Vs JY BrothersDocument4 paginiSalazar Vs JY BrothersMosarah AltÎncă nu există evaluări

- Ting Ting Pua V Sps TiongDocument2 paginiTing Ting Pua V Sps TiongeieipayadÎncă nu există evaluări

- Cayanan Vs North StarDocument2 paginiCayanan Vs North StarMosarah AltÎncă nu există evaluări

- People V WagasDocument1 paginăPeople V WagasMosarah AltÎncă nu există evaluări

- PNB Vs BalmacedaDocument2 paginiPNB Vs BalmacedaMosarah AltÎncă nu există evaluări

- San Miguel Corp Vs PuzonDocument2 paginiSan Miguel Corp Vs PuzonMosarah AltÎncă nu există evaluări

- Politicsl LawDocument91 paginiPoliticsl LawMosarah AltÎncă nu există evaluări

- Equitable PCI Vs TanDocument2 paginiEquitable PCI Vs TanMosarah AltÎncă nu există evaluări

- Spec Com BQsDocument15 paginiSpec Com BQsMosarah AltÎncă nu există evaluări

- Mock Trial ScriptDocument25 paginiMock Trial ScriptRonilo Subaan94% (18)

- Sps Ros Vs PNB 2011 PDFDocument8 paginiSps Ros Vs PNB 2011 PDFMosarah AltÎncă nu există evaluări

- Tax ReviewerDocument45 paginiTax ReviewerMosarah AltÎncă nu există evaluări

- Siochi Vs CA 2010 PDFDocument9 paginiSiochi Vs CA 2010 PDFMosarah AltÎncă nu există evaluări

- Sps Uy Vs CA 2000Document7 paginiSps Uy Vs CA 2000Mosarah AltÎncă nu există evaluări

- Ching Vs CA 1990Document6 paginiChing Vs CA 1990Mosarah AltÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Lecture6 - RPGT Class Exercise QDocument4 paginiLecture6 - RPGT Class Exercise QpremsuwaatiiÎncă nu există evaluări

- 2007 BP Gtcs V 2015 BP P GTCS: A Quick Re Eference E GuideDocument6 pagini2007 BP Gtcs V 2015 BP P GTCS: A Quick Re Eference E GuideAmit NehaÎncă nu există evaluări

- Revised Deed of SaleDocument2 paginiRevised Deed of Salejethro chanÎncă nu există evaluări

- Types of Business Entities PDFDocument6 paginiTypes of Business Entities PDFLaxmi PrasannaÎncă nu există evaluări

- Republic of The Philippines Vs Roque GR 203610 2016Document13 paginiRepublic of The Philippines Vs Roque GR 203610 2016Lu CasÎncă nu există evaluări

- Summary of Points Cases Law and Relevant Citations Regarding Unlawful Detainer Post ForeclosureDocument12 paginiSummary of Points Cases Law and Relevant Citations Regarding Unlawful Detainer Post ForeclosurePeter Walsh100% (4)

- Lease Agreement Myrna BanoDocument3 paginiLease Agreement Myrna BanoMon Anthony MolobocoÎncă nu există evaluări

- Frustration - ContractDocument3 paginiFrustration - ContractTyler ReneeÎncă nu există evaluări

- Music Publishing Agreement - Sample AgreementsDocument3 paginiMusic Publishing Agreement - Sample AgreementsDon Quichotte Al ArabÎncă nu există evaluări

- Cuizon v. CADocument2 paginiCuizon v. CAVhinjealeen Mae CostillasÎncă nu există evaluări

- Basic Labor LawsDocument26 paginiBasic Labor LawsIrene CunananÎncă nu există evaluări

- 13 - Sample Circular Resolution - Section 289Document3 pagini13 - Sample Circular Resolution - Section 289Khalid MahmoodÎncă nu există evaluări

- Bank Performance Ratios - 2Document29 paginiBank Performance Ratios - 2Shiba Prasad MohantyÎncă nu există evaluări

- Maloles V CADocument2 paginiMaloles V CAElah ViktoriaÎncă nu există evaluări

- Trainee AgreementDocument3 paginiTrainee Agreementanon_98704194767% (3)

- Undertaking Promissory NoteDocument2 paginiUndertaking Promissory NoteCherilou Tanglao0% (1)

- Deed of Gift: RecitalsDocument2 paginiDeed of Gift: RecitalsFaisal RafiqÎncă nu există evaluări

- Loss of The Thing DueDocument2 paginiLoss of The Thing DueVonÎncă nu există evaluări

- Real Mortgage Report FinalDocument17 paginiReal Mortgage Report FinalMaritesCatayongÎncă nu există evaluări

- Multiple ChoiceDocument5 paginiMultiple ChoicePrincess Frean VillegasÎncă nu există evaluări

- The Motor Vehicles Act PDFDocument5 paginiThe Motor Vehicles Act PDFAnupamaÎncă nu există evaluări

- Minions Colouring BookDocument10 paginiMinions Colouring Bookirina_195Încă nu există evaluări

- Deed of Sale of Motor VehicleDocument1 paginăDeed of Sale of Motor VehicleRalph AnitoÎncă nu există evaluări

- Quasi ContractsDocument20 paginiQuasi ContractsvibhahegdeÎncă nu există evaluări

- Settlement AgreementDocument24 paginiSettlement Agreementhongthanhvu100% (1)

- Bajaj Allianz Life Insurance Company Limited: Bajaj Allianz CSC Bachat Plus Part A Forwarding LetterDocument10 paginiBajaj Allianz Life Insurance Company Limited: Bajaj Allianz CSC Bachat Plus Part A Forwarding LetterAjay NainÎncă nu există evaluări

- Legal Technique Cases Digest Succession 2017 2018Document11 paginiLegal Technique Cases Digest Succession 2017 2018Ronellie Marie TinajaÎncă nu există evaluări

- 20 Cube El (Final)Document20 pagini20 Cube El (Final)ankitÎncă nu există evaluări

- Deutsche Bank No Standing in BK CT TarantolaDocument16 paginiDeutsche Bank No Standing in BK CT Tarantolabsprop7776578Încă nu există evaluări

- Negotiable Instruments LawDocument24 paginiNegotiable Instruments LawMaLizaCainapÎncă nu există evaluări