Documente Academic

Documente Profesional

Documente Cultură

Chapter 6 - Company Audit

Încărcat de

Shubham agrawalDrepturi de autor

Formate disponibile

Partajați acest document

Partajați sau inserați document

Vi se pare util acest document?

Este necorespunzător acest conținut?

Raportați acest documentDrepturi de autor:

Formate disponibile

Chapter 6 - Company Audit

Încărcat de

Shubham agrawalDrepturi de autor:

Formate disponibile

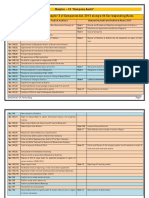

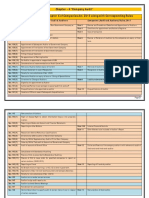

Chapter – 6 “Company Audit”

Section – Wise Index of Chapter X of Companies Act, 2013 along with Corresponding Rules

Chapter X of Companies Act, 2013 – Audit & Auditors Companies (Audit and Auditors) Rules, 2014

(Sec. 139 – 148)

Appointment of Subsequent Auditor of Non-Government Company at Rule 3 Manner and Procedure of Selection and Appointment of Auditors

Sec. 139(1)

AGM Rule 4 Conditions for appointment and Notice to Registrar

Sec. 139(2) Rotation of Auditors Rule 5 Class of Companies

Sec. 139(3) Rotation of Auditing Partner and his team

Sec. 139(4) Power of C.G. to prescribe the manner of rotation. Rule 6 Manner of Rotation of Auditors by the companies on expiry of their

term.

Sec. 139(5) Appointment of Subsequent Auditor of Government Company

Sec. 139(6) Appointment of First Auditor of Non-Government Company

Sec. 139(7) Appointment of First Auditor of Government Company

Sec. 139(8) Filling of Casual Vacancies

Sec. 139(9) Re-appointment of Retiring Auditor

Sec. 139 (10) No Auditor is appointed or reappointed at AGM

Sec. 139 (11) Considerations of recommendations of Audit Committee

Sec. 140(1) Removal of Auditor before expiry of his term Rule 7 Removal of Auditor before expiry of his term

Sec. 140(2) Filing of statement in case of Resignation Rule 8 Resignation of Auditor

Sec. 140(3) Penalty for non-compliance of Sec. 140(2)

Sec. 140(4) Removal of Auditor on expiry of tenure / Giving of Special Notice

Sec. 140(5) Directions for Change of Auditors Rule 9 Liability to devolve on concerned partners only.

Sec. 141(1) Eligibility for appointment as Auditor

Sec. 141(2) Authorised Partner to act and sign in case of audit firm and LLP

Sec. 141(3) Disqualifications to be appointed as auditor Rule 10 Disqualifications of Auditor

Sec. 141(4) Vacation of Office in case of Subsequent disqualifications

Compiled by: CA. Pankaj Garg Page 1

Sec. 142 Remuneration of Auditors

Sec. 143(1) Right of Access/Right to obtain Information/Inquiry into propriety

matters

Sec. 143(2) Reporting on Books and Accounts and Financial Statements

Sec. 143(3) Reporting on other Matters Rule 10A Internal Financial Controls

Rule 11 Other Matters to be included in Auditor’s Report

Sec. 143(4) Reasons for Adverse Remarks or Qualifications

Sec. 143(5) Directions by CAG to auditor of Government Company

Sec. 143(6) Order by CAG of Supplementary Audit of F.S. of Govt. Company.

Sec. 143(7) Order by CAG of Test audit of Accounts of Government Company

Sec. 143(8) Audit of accounts of Branch Office Rule 12 Duties and Powers of the company auditor’s with reference to audit of

the branch and the branch auditor

Sec. 143(9) Compliance with Standards of Auditing

Sec. 143(10) Powers of C.G., to prescribe the Standards of Auditing

Sec. 143(11) Powers of C.G. to issue order for specified companies to report on

certain matters. (CARO, 2015)

Sec. 143(12) Reporting on Fraud Rule 13 Reporting of Frauds by auditor

Sec. 143(13) No Breach of duty if reporting u/s 143(12) is done in good faith.

Sec. 143(14) Application of Sec. 143 over Cost Accountant and Company Secretary.

Sec. 143(15) Penalty for non-compliance of Sec. 143(12)

Sec. 144 Auditor not to render certain services

Sec. 145 Auditor to sign audit reports, etc.

Sec. 146 Auditor to attend General Meetings

Sec. 147 Punishment for contravention

Sec. 148 Central Government to specify audit of certain items of cost in respect Rule 14 Remuneration of Cost Auditor.

of certain companies

Compiled by: CA. Pankaj Garg Page 2

Appointment of Auditor

Appointment of Subsequent Auditor Appointment of First Auditor

Non-Government Company – Sec. 139(1) Government, Govt. owned Non-Government Company Government, Govt. owned /

/ controlled Companies – – Sec. 139(6) controlled Companies – Sec.

Appointment will be at First AGM Sec. 139(5) 139(7)

till conclusion of 6th AGM; and

hereafter till conclusion of every 6th AGM Appointment of Auditor First auditor shall be First Auditor shall be

appointed by appointed

in prescribed manner (Rule 3).

In respect of a Financial by CAG

Subject to following conditions:

year Board of Directors

Condition Details of condition Within 60 days of

1. Ratification Omitted by Companies registration of company

will be made by Within 30 days

(Amendment) Act, 2017

2. Written Before appointment company If CAG does not appoint the

CAG of registration of company auditor

consent shall obtain

(a) Written consent from auditor BOD will appoint within next

(b) Certificate from auditor. Within a period of 180 If Board fails, Board shall 30 days

(Rule 4) Days inform the members

3. Certificate Certificate shall indicate If Board fails, Board shall

From the commencement Members shall within 90 inform the members

Whether auditor has satisfied

the criteria as provided u/s of financial year days

Members shall within 60

141. days

4. Intimation to Company shall inform the Who shall hold the office at an EGM at an EGM

ROC auditor and ROC about the till the conclusion of next

AGM appoint the first auditor appoint the first auditor

appointment of auditor within

15 days of appointment.

Compiled by: who hold office till

Rule 4 – Intimation to ROC Who hold office till

conclusion of first AGM

will be in Form ADT-1 CA. Pankaj Garg conclusion of first AGM

Compiled by: CA. Pankaj Garg Page 3

Rule 3 & 4 of Companies (Audit & Auditor’s) Rules, 2014

Rule 3 – Manner and procedure for selection and Appointment of Auditors Rule 4 – Conditions for Appointment and

Notice to Registrar

Company is required to constitute Audit Committee u/s 177

Yes No Certificate obtained from the auditor shall

contain the following:

Audit Committee shall consider the qualifications and BOD shall consider the

experience of the person considered for appointment qualifications and experience (a) That the individual or the audit form, as

as auditor of the person considered for

appointment as auditor the case may be, is eligible for

appointment as per the provisions of

Audit Committee shall recommend the name of person BOD Agree this Act and Chartered Accountants Act,

to BOD for their consideration

Place the matter for 1949.

BOD disagree considerations by members (b) That proposed appointment is as per

in AGM.

the terms provided in the Act.

BOD shall refer back the matter to audit committee for (c) That proposed appointment is within

reconsideration the limits prescribed by the Act.

(d) That list of proceedings against the

Audit Committee agree for Audit committee decides auditor or the audit firm or any partner

reconsideration not to reconsider of the firm w.r.t. disciplinary matters as

disclosed in the Certificate, is true and

BOD will record the

reasons for disagreement correct.

BOD make its own

recommendations

Compiled by: CA. Pankaj Garg

Place the matter for considerations

by members in AGM.

Compiled by: CA. Pankaj Garg Page 4

Rotation of Auditor

Sec. 139(2) Sec. 139(3) Sec. 139(4)

Listed companies and Other prescribed companies Rule 5 Unlisted Public Companies having Members may resolve the C.G. may by Rules

Shall not appoint paid up capital > 10Cr. following:

(a) Rotation of auditing

Private Companies having paid up Prescribe the manner

partner & his team at

An individual as an auditor for more than one term of capital > 50 Cr. of rotation for Sec.

such interval as may be

139(2)

five consecutive years. Companies not covered above if prescribed.

public borrowings from banks and (b) That audit shall be

conducted by more than (Rule 6 prescribes

An audit Firm as an auditor for more than two terms of FI/ public deposits > 50Cr.

one auditor the manner of

five consecutive years. rotation)

1st Proviso Individual Auditor Not eligible for reappointment for 5 years after completing of

as auditor in same company tenure Rule 6 – Manner of Rotation

Audit Firm Not eligible for reappointment for 5 years after completing of

as auditor in same company tenure 1. For calculating period of 5 years / 10 years, period

served prior to commencement of this Act, shall also

2nd Audit Firm Having a common partner with audit firm

be considered.

Proviso Whose tenure has just expired 2. Individual auditor / Audit Firm shall not be eligible

As on date of appointment for appointment as auditor for a period of 5 years if

it belongs to same network to whom retiring auditor

Shall not be appointed as auditor of same company

belong to.

for a period of five years 3. Break in the term should be for a continuous period

3rd Proviso Every Company Existing before commencement of this Act of 5 years.

4. A partner in charge of audit firm who certifies the

Shall comply with requirement of Sec. 139(2)

financial statements of the company, if retires from

Within a period which shall not be later than the date of First the said firm and join another firm, such other firm

AGM after 3 years from the date of commencement of this Act. shall also be ineligible to be appinte da s auditor for

4th Proviso Sec. 139(2) shall not Right of company to remove auditor a period of 5 years.

prejudice the Right of auditor to resign. Compiled by: CA. Pankaj Garg

Compiled by: CA. Pankaj Garg Page 5

Other Provisions of Sec. 139

Filling of Casual vacancies Reappointment of No auditor Appointed Recommendation of

Auditor at AGM Audit Committee

– Sec. 139(8) – Sec. 139(9) – Sec. 139(10) – Sec. 139(11)

A retiring auditor may If no Auditor is Where a company is

be appointed required to constitute

Non Govt. Co. – Sec. 139(8)(i) Govt. Co./Govt. Owned/ an audit committee

controlled Co. - Sec. 139(8)(ii) Reappointed at AGM, if

at AGM (Sec. 177)

he is

Due to resignation Other Be filled by

Reasons Existing auditor will All appointments

Not disqualified under

Be filled by BOD Be filled by CAG continue including filling of

law

BOD casual vacancies

Within 30 days

Within 30 days Not unwilling to

Shall be made only after

Such appointment Within 30 continue,

AND considering the

shall be days If CAG does not fill the casual

No special resolution recommendations of

vacancy

Approved in has been passed w.r.t. audit committee.

General meeting

It will be filled by

(a) Appointing someone

Convened within 3 else as auditor

months Board of Directors (b) providing expressly

Compiled by: CA. Pankaj Garg

that retiring auditor

Of shall not be

Within next 30 days

recommendations

reappointed.

of BOD

Compiled by: CA. Pankaj Garg Page 6

Sec. 140 – Removal, Resignation of Auditor and giving of Special Notice

Sec. 140(1) – Removal before expiry Sec. 140(2) & (3) – Filing Sec. 140(4) – Special Notice Sec. 140(5) – Directions for change of Auditor

of Statement in case of

Resignation Special notice shall be required Tribunal may, by order, direct the company

Requires

to change its auditors

Auditor who has resigned to pass the Special resolution at

Special resolution of Company AGM providing that either suo motu or on an application made to

& Shall file it by the C.G. or by any person concerned,

Previous approval of CG in prescribed (a) Retiring Auditor shall not be

manner (Rule 7). re-appointed.

Within 30 days of if it is satisfied that the auditor has acted in a

or

resignation fraudulent manner or abetted or colluded in

(b) To appoint as auditor any

Before taking any action, auditor any fraud.

person other than retiring

concerned should be provided an Statement in prescribed auditor. If the application is made by the C.G.

opportunity of being heard. and

form

Rule 7 Copy of notice to be sent Tribunal is satisfied that any change of the

(Rule 8 : ADT-3)

Application to CG immediately to concerned auditor is required

auditor.

To Company & ROC Tribunal shall within 15 days of receipt of

should be made within 30 days

(Also to CAG – in case of Auditor has a right of such application, make an order

Govt. Companies) representation

of passing of Board Resolution (reasonable length) that he shall not function as an auditor

Indicating the reasons and

in Form ADT-2. Copy of notice and representation C.G. may appoint another auditor in his place.

and other facts relating to needs to be sent to every person

Within 60 days of approval by CG, An auditor against whom final order has

resignation. to whom notice of AGM was given.

been passed by the Tribunal u/s 140(5)

Sec. 140(3): Fine for non-

convene a general meeting Auditor may demand for reading

compliance, Ranging from shall not be eligible to be appointed as an

the representation in meeting.

Rs. 50,000 (Not exceeding auditor of any company for a period of 5

to Pass Special Resolution. Representation need not be

years from the date of passing of the order

Audit Fees) – Rs. 5,00,000 sent or read out at meeting, if

on application of company or and

Opportunity Board Application General the auditor shall also be liable for action u/s

Resolution to CG Meeting other person, Tribunal pass

Compiled by: CA. Pankaj Garg such order. 447.

Compiled by: CA. Pankaj Garg Page 7

Sec. 141 – Eligibility, Qualifications and Disqualifications of Auditor

Sec. 141 (1) & 141 (2) – Sec. 141(3) - Persons not eligible for appointment & Rule 10 Sec. 141(4) –

Eligibility to be appointed as Auditor Vacation of office

A person shall be eligible (a) Body Corporate other than LLP If after appointment

(b) Officer or Employee of the company

for appointment as an auditor (c) Partner/Employee of Officer/Employee of the company An auditor

(d) (i) person/ is holding any security * or Company /

only if he is a CA. relative/ interest in the subsidiary /

Incurs any disqualification

A Firm whereof Majority of Partners (ii) partner is indebted > 5 Lacs in the holding /

(iii) has given a guarantee in associate, or

Mentioned in Sec. 141(3)

Practicing in India connection with indebtedness subsidiary of same holding.

of 3rd person > 1 Lac in the

* no disqualification if relative holds any security in the company of face He shall vacate the office

are Qualified

value upto 1 Lac.

(e) Person or firm having business relationship with Company / Subsidiary / And such vacation shall be

may be appointed

Holding / Associate / Subsidiary of Such Holding or Associate Company treated as casual vacancy

(f) A Person whose relative is a director or is in employment of the company as a

by its firm name as auditor

Director or KMP.

A Firm including LLP Compiled by:

(g) A person who is in full time employment elsewhere

Or CA. Pankaj Garg

If appointed as Auditor

A person holding appointment as auditor or more than 20 companies other

than OPC, dormant companies, Small Companies and private companies

Only partners who are CA having paid up capital < 100Cr.

(h) A person who has been convicted of an offence involving fraud and a period of

Shall be authorized to 10 years has not elapsed.

(i) Any person who directly or indirectly renders any service referred to in

Act and sign on behalf of firm. Sec. 144 to company or its holding company or its subsidiary company.

Compiled by: CA. Pankaj Garg Page 8

Powers / Rights & Duties of Company Auditor (Sec. 143)

RIGHTS OF AUDITOR – Sec. 143(1) DUTIES of AUDITOR

at all times 1. Loans and advances are properly secured and terms are prejudicial .

2. Book entries are prejudicial.

Right of

Access

to books of Account & Vouchers

Inquire into Propriety 3. Shares, debentures and other securities are sold at a price less than acquisition cost in case of non

whether kept at Regd. Office or at any banking and non investment company.

other place. Matters – Sec. 143(1) 4. Loans and advances made are shown as deposits.

5. Personal expenses charged to revenue account.

6. Cash has actually been received on shares allotted for cash, if not received, correct position shown

From the officers of the company in books and balance sheet.

Right to

Obtain

As considers necessary

Info.

Reporting over Accounts &

For performance of his duties. Financial Statements That to the best of auditor information & knowledge, the accounts & financial statements give a true and fair view of

– Sec. 143(2) the state of the company affairs as at the end of its financial year & profit & loss and cash flow for the year.

1. Obtained all necessary information for the audit.

Duties of Auditor Supplementary Test Audit 2. Proper books of accounts have been maintained. Reasons for

of Govt. Cos. – Sec. Audit – Sec. 143(7) 3. Branch audit report has been received and manner of dealing with it. reservations –

143(5) – Sec. 143(6) 4. Balance Sheet and P & L Account agree with the books of accounts. Sec. 143(4)

5. Financial statements comply with AS.

CAG – direct the Within 60 days of CAG may For every

6. Comments on financial transactions having any adverse effect on functioning of company.

auditor the manners days of receipt of If considers matter

7. Directors disqualified u/s 164(2).

in which accounts Audit Report necessary 8. Qualifications w.r.t. maintenance of accounts. reported with a

are to be audited. Reporting u/s 143(3) 9. Adequacy and operative effectiveness of IFC with reference to F.S. qualification

Auditor report shall CAG have a Right by an order 10. Other matters as prescribed. (Rule 11)

Rule 11

include: Auditor shall

1. Disclosure of impact of pending litigations on financial position.

Directions issued To order for cause test audit 2. Provisions for Material Forseeable losses on long term contracts made. state the

by CAG. supplementary 3. Any delay in transferring amounts to IEPF. reasons thereof

Action taken audit of F.S. of accounts of 4. Disclosures w.r.t. holdings and dealings in SBNs.

thereon Govt. companies

Its impact on Bu such persons as Compiled by: Fraud involving prescribed amount Rule 13

Fraud > 1Cr.

Accounts and F.S. authorized by him Committed by officers or employees

CA. Pankaj Garg

Reported to Audit Committee / BOD within 2 days

Should be report to CG in prescribed

Sec. 143(8) Audit of Branch Accounts (will be discussed manner (Rule 13) Seeking their reply within 45 days

separately)

Sec. 143(9) Every Auditor shall comply with Auditing If reply receive, forward his report, reply and comments on

Frauds below prescribed amount reply to CG within 15 days

Standards

Reporting u/s 143(12)

Sec. 143(10) CG may prescribe the SA in consultation Should be reported to Audit If reply not recd., forward his report to CG along with a

with NFRA Committee or BOD note that reply not recd.

Sec. 143(11) CG may direct that auditor’s report shall

include a statement on such matters as Details of Such Frauds need to be

disclosed in Board’s report. Nature of Fraud with description Approx. amount involved

specified in order issued by it. (CARO, 2016)

Parties involves remedial action taken

Compiled by: CA. Pankaj Garg Page 9

Other Provisions (Sec. 142, 144, 145, 146 & 147)

Sec. 142 – Remuneration Sec. 144 – Auditor not to Sec. 145 – Signing of Sec. 146 – Sec. 147 – Punishment for

of Auditors render certain services Audit Reports Attending of Contravention

General meetings

Over the Company & Officer in

default – 147(1)

Authority to Fix Other Services that may be Shall be in accordance with

Violation of Sec. 139-146

remuneration rendered Sec. 141(2) Company – Fine from Rs. 25,000

Shall be General meeting As approved by the BOD to Rs. 5 Lacs.

or in such manner as or Audit Committee. Officer in default–Imprisonment

may be determined All Notice & other upto 1 year or fine from Rs.

therein. Services that cannot be rendered directly or indirectly to communication of 10,000 to Rs. 1 Lac or Both

May be BOD in case of Co, Holding or Subsidiary general meetings

Over the Auditor – 147(2)

first auditor if appointed Accounting & Book Keeping. shall be forwarded Violation of Sec. 139, 143, 144,

to Auditor. 145.

by BOD Internal Audit

Fine from ₹25,000 to (₹5 Lacs or

Unless exempted 4 times the remuneration,

Design & Implementation of Financial Information System.

auditor shall whichever is less).

Actuarial Services. In case of Willful default –

Elements of remuneration attend either Imprisonment upto 1 year and

Investment advisory. himself or through fine from ₹50,000 to (₹25 Lacs

Shall include all or 8 times the remuneration,

Investment Banking his authorized whichever is less).

expenses incurred in

Outsourced Financial representative any

connection with audit general meeting,

Management Services

and any facility extended Auditor shall have If auditor convicted u/s 147(2)

Other Prescribed.

to auditor. right to be heard

he shall be liable to

Does not include at such meeting on

remuneration paid for part of business Refund the remuneration

Compiled by: CA. Pankaj Garg and

any other service. which concerns

Pay for damages

him as auditor.

Compiled by: CA. Pankaj Garg Page 10

Cost Records and Cost Audit (Section 148 of Companies Act, 2013 & Companies (Cost Records and Audit), Rules, 2014

Cost Records Cost Audit

Sec. 148(1) Rule 3 of Companies (Cost Requirement Cost Auditor Cost Audit report

C.G. may by order Records & Audit) Rules, 2014

Companies including foreign Sec. 148(2) Rule 4 of Companies (Cost Sec. 148(3)

In respect of such Sec. 148(5) & 148(6)

companies Records & Audit) Rules, 2014 Cost Audit shall be conducted

companies C.G. may be order Cost Auditor shall submit

his report to

Cost Records are required to by Cost Accountant

Engaged in Engaged in direct for the be audited BOD

Appointed by BOD

production of goods Company shall

production of audit of cost If overall annual turnover in prescribed manner

prescribed goods Or

providing services records of No person appointed u/s 139 within 30 days of date of

Or From all products and

as specified As an auditor receipt of report

providing prescribed

services

services companies

Shall be appointed as cost furnish such report to CG

Regulated Sector Non covered u/s

Regulated In immediate preceding

direct that 148(1) auditor along with full information &

Sector Financial Year

Telecommunication Iron Rule 6 of Companies (Cost explanation.

Electricity Steel having Records & Audit) Rules, 2014 Rule 6 of Companies

particulars relating to In case of

Petroleum Rubber

prescribed net Cost Auditor shall be appointed (Cost Records & Audit)

Regulated Non Regulated

Sugar Cement within 180 days of commencement Rules, 2014

Material Drugs and Pharma etc.

worth or Sector Sector

of every financial year. Cost Auditor shall submit

turnover >50 Cr. >100 Cr.

Labour Fertilisers Before appointment written Cost Audit Report

or consent & certificate be obtained.

Other items of cost Having turnover > 35 Cr. in a manner AND Company Shall inform the cost in Form CRA-3.

auditor of his appointment.

Cost Auditor shall forward

Company Shall file a notice with CG

Shall be included in During immediate preceding Aggregate Turnover of Duly Signed Report to BOD

specified in that in Form CRA-2 within 30 days of

financial year Individual product or service

order Board meeting or within 180 days

the books of accounts of commencement of FY whichever Within 180 days from

shall include cost records in closure of FY.

>25 Cr. >35 Cr. is earlier.

their books of accounts

Cost Auditor appointed as such Report along with

Requirement of Cost Audit shall not apply to a company shall continue till expiry of 180 information & explanation to

days of closure of FY or till

Exemption –

Every Company under these Rules shall In respect of each of

Rule 4(3)

Whose revenue from exports in foreign exchange exceeds 75% submission of cost audit report. Shall be furnished to CG in

its Financial year

Rule 5

of its total revenue Cost statements shall be approved

or

Form CRA-4 in XBRL Format

by BOD before being signed by any

which is operating from SEZ.

Maintain Cost records in Form CRA - 1 director on behalf of Board for

or Compiled by: CA. Pankaj Garg

Engaged in generation of electricity for captive consumption submission to cost auditor.

Compiled by: CA. Pankaj Garg Page 11

Branch Audit [Sec. 143(8) and Rule 12] and Payments controlled by Companies Act, 2013

Branch Audit Payments controlled by Companies Act, 2013

Branch Office – Branch office, in relation to a company, means any Sec. 181 Contribution to Charitable Funds

Sec. 2(14) establishment described as such by the company. BOD can contribute to the bona fide charitable and other funds any

Persons Eligible amount in any FY.

Indian Company Auditor

to be appointed If aggregate of such contribution exceeds 5% of average net profits of

Branch Other person qualified for appointment

as Branch 3 immediately preceding FY, prior permission of company is required.

as auditor as per Sec. 141.

Auditor Sec. 182 Political Contribution

Foreign Company Auditor

– Sec. 143(8) Government company or any other company which has been in

Branch Other person qualified for appointment existence for less than 3 FY cannot contribute any amount directly or

as auditor as per Sec. 141. indirectly to any political party.

Other person qualified for appointment In other cases, contribution in any FY can be made if a resolution

as auditor in accordance with the Laws authorising the making of such contribution is passed at a Board

of that country, Meeting.

Duties of Branch Prepare a report on the accounts of the branch Every company shall disclose in its P&L A/c total amount contributed

by it under this section during the FY to which the account relates.

Auditor examined by him

Contribution shall not be made except by an A/c payee cheque drawn

– Sec. 143(8) and

on a bank or an A/c payee bank draft or use of electronic clearing

send it to the auditor of the company who shall deal

system through a bank account.

with it in his report in such manner as he considers

Sec. 183 Contribution to National Defence Fund

necessary.

Section 183 permits the Board or any person or authority exercising

Duties & powers (1) The duties and powers of the company’s auditor the powers of the Board or company to make contributions to the

of the company’s with reference to the audit of the branch and the National Defence Fund or any other Fund approved by the CG for the

auditor with branch auditor, if any, shall be as contained in sub- purpose of National Defence to any extent as it thinks fit.

reference to the sections (1) to (4) of section 143. Every company shall disclose in its profit and loss account the total

audit of the (2) The branch auditor shall submit his report to the amount or amounts contributed by it to the National Defence Fund

branch and the company’s auditor. during the financial year to which the amount relates.

branch auditor (3) The provisions regarding reporting of fraud by the

– Rule 12 auditor shall also extend to such branch auditor to Compiled by: CA. Pankaj Garg

the extent it relates to the concerned branch.

Compiled by: CA. Pankaj Garg Page 12

Audit of Limited Liability Partnerships (LLP Audit) – Sec. 34 of LLP Act, 2008 & Rule 24 of LLP Rules, 2009

Statutory provisions Relating to Statutory provisions Relating to Audit Advantages/Purpose/Need of Audit

Books

Rule 24 of LLP Rules, 2009 (a) Detection of errors & frauds

1 Requirement of Audit

(b) Verification of financial statements

1. Books of Accounts – Sec. 34 (c) Resolving disputed among the partners

LLP shall maintain prescribed books LLP whose turnover does not exceed, in any FY, ₹40 Lacs, or

in relation to accounting matters.

relating to its affairs for each year. whose contribution does not exceed ₹25 Lacs shall not be

(d) Arranging finance from banks & F.I.

Books may be maintained on cash or required to get its accounts audited.

(e) Improved management of the LLP

accrual basis and as per double entry If partners decide to get the accounts of such LLP audited, the

(f) Settlement of accounts between partners

system. accounts shall be audited in accordance with these rules.

at time of admission, death, retirement,

Books shall be maintained at regd. office 2 Eligibility for auditor

for prescribed period.

insolvency, insanity, etc

A person shall not be qualified for appointment as an auditor of a

Rule 24 of LLP Rules, 2009

LLP unless he is a CA in practice. Auditor’s duties w.r.t. Audit of LLP

The books of account shall contain:

3 Period of Appointment

(a) particulars of all sums of money

received and expended; Auditor of LLP shall be appointed for each financial year of the

(a) Obtain instructions in writing as to work to be

(b) a record of the assets and liabilities; LLP for auditing its accounts.

performed.

(c) statements of cost of goods purchased, 4 Appointment of auditor by designated partner (b) Read the LLP agreement & note the following

inventories, WIP, finished goods & COGS; The designated partners may appoint an auditor: Nature of the business of LLP

and Capital contributed by each partner

(a) at any time for the first FY but before the end of first FY,

(d) other particulars which partners may Interest in respect of capital contributions

(b) at least 30 days prior to the end of each FY (other than the

decide.

first FY), Duration of partnership

Books shall be preserved for 8 years from

Drawings allowed to the partners

the date on which they are made. (c) to fill a casual vacancy, including in the case when the

Salaries, commission etc payable to partners

2. Statement of Account and Solvency turnover or contribution of a LLP exceeds the limits, or

Rights & duties of partners

Every LLP shall, within a period of 6 (d) to fill up the vacancy caused by removal of an auditor.

Method of settlement of A/cs between partners at

months from the end of each FY, prepare 5 Appointment of auditor by partner time of admission, retirement, admission etc.

a Statement of Account & Solvency for Partners may appoint an auditor where the designated partners Any loans advanced by the partners

the said FY and such statement shall be have power to appoint and have failed to appoint. Profit sharing ratio

signed by the designated partners of the (c) Auditor should report (a) Whether the records reflects

6 Tenure of Auditor

LLP. true and fair view (b) Whether he obtains all

Auditor shall hold office in accordance with the terms of his

Statement of Account and Solvency shall information & explanation (c) whether any

appointment and shall continue to hold such office till the period

be filed with the Registrar in Form 8 restriction/limitation imposed upon him.

within a period of 30 days from the end (a) the new auditors are appointed, or

(d) If minute book is being maintained, auditor shall refer it

of 6 months of the financial year. (b) they are re-appointed. for any resolution passed regarding the accounts.

Compiled by: CA. Pankaj Garg Page 13

Guidance Note on Reporting u/s 143(3)(f) and 143(3)(h) of Companies Act, 2013

Reporting u/s 143(3)(f) of Companies Act, 2013 Reporting u/s 143(3)(h) of

Companies Act, 2013

The auditor’s report shall state …………………………………….

The auditor’s report shall state

(f) the observations or comments of the auditors on financial transactions or matters which have any adverse

…………………………………….

effect on the functioning of the company”.

(i) any qualification, reservation or adverse

remark relating to the maintenance of

The words “observations” or “comments” as appearing in Sec. 143(3) are construed to have the same meaning as accounts and other matters connected

referring to “emphasis of matter paragraphs, situations leading to modification in the auditor’s report”.

therewith;

For the sake of clarity, it may be noted that neither the auditor’s observations nor the comments made by him

have any adverse effect on the functioning of a company. These observations or comments made by the auditor

might contain matters which might have an adverse effect on the functioning of a company. The words “qualification”, “adverse remark”

The Act does not specify the meaning of phrase 'adverse effect on the functioning of the company'. The expression and “reservation” should be considered to be

should not be interpreted to mean that any event affecting the functioning of the company, observed by the similar to the terms “qualified opinion”,

auditor, should be reported upon even though it does not affect the F.S.

“adverse opinion” and “disclaimer of opinion”,

respectively, referred to in SA 705.

The auditor would need to report u/s

Impact of this clause over objective and Scope of Audit

143(3)(h) any matter that causes a

There is no change in the objective and scope of an audit of F.S. because of inclusion of clause (f) in Sec. 143(3).

The auditor expresses his opinion on the true and fair view presented by the F.S. through his report which may be

qualification, adverse remark or disclaimer of

modified in certain circumstances. opinion on the F.S. since such matters will or

However, the auditor would now have to evaluate the subject matters leading to modification of the audit report or EOM possibly will have an effect on the books of

in the auditor’s report to make judgement as to which of them has an adverse effect on the functioning of the company. account maintained by the company.

Only such matters which, in the opinion of the auditor, have an adverse effect on the functioning of the company should Reporting u/s 143(3)(h) will be required if

be reported under this clause. the auditor makes any observation u/s

Conversely, such qualifications or adverse opinions or disclaimer of opinion or EOM, which do not deal with matters 143(3)(b) relating to whether proper books of

that have adverse effect on the functioning of the company, need not be reported under this clause. account as required by law have been kept.

Reporting u/s 143(3))(h) will not be required

Examples of EOM which may have an adverse effect Examples of EOM matter which may not have an adverse effect if there are no modifications and there are no

on the functioning of the company on the functioning of the company such observations u/s 143(3)(b) regarding

The going concern assumption is appropriate but Situation where there is an emphasis of matter: books of account kept by the company.

there are several factors leading to a material 1. on managerial remuneration which is subject to the approval of A matter reported under EOM paragraph in

uncertainty that may cast a significant doubt about the Central Government; the audit report need not be considered for

Company’s ability to continue as a going concern; or 2. relating to accrual of a contractually receivable claim based on reporting u/s 143(3)(h) as an EOM is not in

a material uncertainty regarding the outcome of a management estimate where the ultimate realisation could be

the nature of a qualification, reservation

litigation wherein an unfavourable decision could different from the amount accrued;

result in a significant outflow of resources for the 3. on frauds that have been dealt with in the financial statements of (disclaimer) or adverse remark.

company, etc. the company and would not have any continuing effect on the

financial statements. Compiled by: CA. Pankaj Garg

Compiled by: CA. Pankaj Garg Page 14

Guidance Note on IFC over Financial Reporting and Guidance Note on reporting of Fraud u/s 143(12)

Guidance Note on IFC over Financial Reporting Guidance Note on Reporting of Fraud u/s 143(12)

1 Meaning of Internal Financial Control – Sec. 134 of Companies Act, 2013 1 Duty to report on frauds – Sec. 143(12)

Policies and procedures adopted by the company for ensuring: If auditor in the course of the performance of his duties, has reason to

Orderly & efficient conduct of its business, including adherence to Company policies, believe that an offence of fraud involving prescribed amount, is being or

Safeguarding of its assets, has been committed in company, by its officers or employees, the auditor

Prevention and detection of frauds and errors, shall report the matter to the C.G., within prescribed time and manner.

Accuracy and completeness of the accounting records, and 2 Manner of Reporting - Fraud amounting to ₹1 Cr. or more

Timely preparation of reliable financial information. If auditor has reason to believe that an offence of fraud, which involves or

2 Meaning and concept of Internal Controls over financial Reporting (ICFR) is expected to involve individually an amount of ₹1 Cr. or above, is being

or has been committed against company by its officers or employees, the

A Process designed to provide reasonable assurance regarding the reliability of financial reporting

auditor shall report the matter to the C.G. in following manner:

and the preparation of F.S. for external purposes in accordance with GAAPs.

Report the matter to Board/Audit Committee, immediately but not later

Company’s IFC over financial reporting includes those policies & procedures which pertain to the than 2 days of his knowledge of fraud, seeking their reply within 45 days;

maintenance of the records that, in reasonable detail, accurately and fairly reflect the transactions on receipt of such reply, the auditor shall forward his report and the reply

and dispositions of the assets. of Board/Audit Committee along with his comments to the C.G. within 15

It provides reasonable assurance that transactions are recorded as necessary to permit days from date of receipt of such reply;

preparation of F.S. in accordance with GAAPs, and receipts and expenditures of the company are In case reply not received, auditor shall forward his report to C.G. along

being made only in accordance with authorizations of mngt and director of the company. with a note containing details of his report that was forwarded to Board/

Audit Committee for which he has not received reply;

It provides reasonable assurance regarding prevention or timely detection of unauthorized

Report shall be sent to the Secretary, MCA in a sealed cover by Regd. Post

acquisition, use or disposition of the company’s assets that could have a material effects on F.S. with AD or by Speed Post followed by an e-mail in confirmation of the same;

3 Reporting Requirements Report shall be on letter-head of the auditor containing postal address, e-

Sec. 134 In the case of a listed company, the Directors’ Responsibility states that directors, mail address, contact details and be signed by the auditor with his seal and

have laid down IFC to be followed by the company and that such controls are shall indicate his Membership Number; and

adequate and operating effectively. Report shall be in the form of a statement as specified in Form ADT-4.

Sec. 143 The auditor’s report should also state whether the company has adequate IFC 3 Manner of Reporting - Fraud amounting to less than ₹1 Cr.

system in place and the operating effectiveness of such controls. Section 143(12) prescribes that in case of a fraud involving lesser than the

specified amount [i.e. less than ₹1 Cr.], the auditor shall report the matter

Sec. 177 Audit committee may call for comments of auditors about internal control systems

to the audit committee constituted u/s 177 or to the Board in other cases

before their submission to the Board and may also discuss any related issues with within such time and in such manner as may be prescribed.

the internal and statutory auditors and the management company. In this regard, Rule 13(3) of the CAAR, 2014 states that in case of a fraud

Sch. IV The independent directors should satisfy themselves on the integrity of financial involving amount less than ₹1 Cr., the auditor shall report the matter to

information and ensure that financial controls and systems of risk management are Audit Committee constituted u/s 177 or to the Board immediately but not

robust and defensible. later than 2 days of his knowledge of the fraud and he shall report the

Rule 8 of matter specifying the following:

The director’s report should contain details in respect of adequacy of internal

Companies (a) Nature of Fraud with description; Compiled by:

(Accounts) financial controls with reference to the financial reporting. (b) Approximate amount involved; and

Rules, 2014 CA. Pankaj Garg

(c) Parties involved.

Compiled by: CA. Pankaj Garg Page 15

S-ar putea să vă placă și

- Auditors Qualification 2.1Document39 paginiAuditors Qualification 2.1Sayraj Siddiki AnikÎncă nu există evaluări

- 10 Company AuditDocument14 pagini10 Company AuditSurendar SirviÎncă nu există evaluări

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorDe la EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorÎncă nu există evaluări

- Liabilities of AuditorDocument39 paginiLiabilities of AuditorMenuka SiwaÎncă nu există evaluări

- Auditing SEM-6: Company AuditDocument21 paginiAuditing SEM-6: Company AuditShilpan ShahÎncă nu există evaluări

- Term Paper On Formation of A CompanyDocument28 paginiTerm Paper On Formation of A CompanyAbbas Ansari100% (1)

- Copy of Different Types of Audit ReportDocument8 paginiCopy of Different Types of Audit ReportRonak SinghÎncă nu există evaluări

- CA Final Securities Law Charts - by CA Swapnil PatniDocument13 paginiCA Final Securities Law Charts - by CA Swapnil PatniAman JainÎncă nu există evaluări

- Facts of The Case: The CBI, Hyderabad, Laid Charge Sheet AgainstDocument6 paginiFacts of The Case: The CBI, Hyderabad, Laid Charge Sheet AgainstmadhuÎncă nu există evaluări

- Theory Notes of Cost & Management Accounting-Executive-RevisionDocument94 paginiTheory Notes of Cost & Management Accounting-Executive-RevisionSuvarna RamakrishnanÎncă nu există evaluări

- Rights, Duties and Liabilities of An AuditorDocument8 paginiRights, Duties and Liabilities of An AuditorShailee ShahÎncă nu există evaluări

- Crimimal Trials Under CRPCDocument26 paginiCrimimal Trials Under CRPCPintu Rao100% (1)

- PDFDocument17 paginiPDFRAJAT DUBEYÎncă nu există evaluări

- Internal Control - Internal Audit & Internal Checks by - Good PDFDocument8 paginiInternal Control - Internal Audit & Internal Checks by - Good PDFsarvjeet_kaushal0% (1)

- Vouching Meaning: Vouching Means The Examination of Documentary Evidence in Support of Entries ToDocument4 paginiVouching Meaning: Vouching Means The Examination of Documentary Evidence in Support of Entries ToShubhangi GuptaÎncă nu există evaluări

- Unit 3&4Document11 paginiUnit 3&4chethanraaz_66574068Încă nu există evaluări

- Best Judgement AssessmentDocument6 paginiBest Judgement AssessmentGautam JayasuryaÎncă nu există evaluări

- On Winding UpDocument9 paginiOn Winding UpSarthak SinghÎncă nu există evaluări

- Case Laws On Service TaxDocument97 paginiCase Laws On Service TaxshantX100% (1)

- Offences and Prosecution Under Income Tax ActDocument8 paginiOffences and Prosecution Under Income Tax Actnahar_sv1366Încă nu există evaluări

- MRTP ActDocument18 paginiMRTP ActSourabh SinghÎncă nu există evaluări

- Powers of Directors General Powers Vested Under Section 179Document7 paginiPowers of Directors General Powers Vested Under Section 179yogesh_96Încă nu există evaluări

- Cost AuditDocument4 paginiCost AuditsanyamÎncă nu există evaluări

- Recovery of Debts and Bankruptcy Act 1993 ("DRT ACT") : BY Adhi Chakravarthy - ADocument42 paginiRecovery of Debts and Bankruptcy Act 1993 ("DRT ACT") : BY Adhi Chakravarthy - AAdhi ChakravarthyÎncă nu există evaluări

- The Industrial Employment Standing OrderDocument11 paginiThe Industrial Employment Standing Orderniveditha krishnaÎncă nu există evaluări

- Types of Income Tax AssessmentDocument3 paginiTypes of Income Tax AssessmenttayaisgreatÎncă nu există evaluări

- Lecture 8 - Winding Up of A CompanyDocument24 paginiLecture 8 - Winding Up of A CompanyManjare Hassin RaadÎncă nu există evaluări

- Guidance On Tax Audit Under Section 44ABDocument5 paginiGuidance On Tax Audit Under Section 44ABSukumar BasuÎncă nu există evaluări

- Dividend Under Companies Act, 2013: CS Divesh GoyalDocument12 paginiDividend Under Companies Act, 2013: CS Divesh GoyalAbhinay KumarÎncă nu există evaluări

- Income Tax Law PracticeAll Units RB2Document20 paginiIncome Tax Law PracticeAll Units RB2Surya LakshmiÎncă nu există evaluări

- Hint: Certificate Is Valid, Moosa Goolam Ariff Vs Ebrahim Goolam AriffDocument13 paginiHint: Certificate Is Valid, Moosa Goolam Ariff Vs Ebrahim Goolam AriffM Tariqul Islam MishuÎncă nu există evaluări

- Divisible ProfitDocument14 paginiDivisible ProfitVeeresh SharmaÎncă nu există evaluări

- Law 05 Company Law 02 Classification of Companies Notes 20170314 ParabDocument20 paginiLaw 05 Company Law 02 Classification of Companies Notes 20170314 ParabarshiÎncă nu există evaluări

- GrtituttyDocument2 paginiGrtituttyNiranjani Duvva Jakkula100% (2)

- Banker's Books Evidence Act 1891Document3 paginiBanker's Books Evidence Act 1891Syed Mustafa AliÎncă nu există evaluări

- Different Modes of Wind UpDocument3 paginiDifferent Modes of Wind UpHarini BÎncă nu există evaluări

- Divisible Profit: DividendDocument10 paginiDivisible Profit: Dividendsameerkhan855Încă nu există evaluări

- Cost AuditDocument10 paginiCost AuditHasan AhmmedÎncă nu există evaluări

- Duty DrawbackDocument35 paginiDuty DrawbackTuhin SaxenaÎncă nu există evaluări

- Special CourtsDocument3 paginiSpecial CourtsGauri Sanjeev ChauhanÎncă nu există evaluări

- Unit 2 - Income From Business or ProfessionDocument13 paginiUnit 2 - Income From Business or ProfessionRakhi DhamijaÎncă nu există evaluări

- Practical AuditingDocument77 paginiPractical AuditingVijay KumarÎncă nu există evaluări

- Advance TaxDocument17 paginiAdvance TaxdevdattdÎncă nu există evaluări

- Checklist For Issue of CCDDocument1 paginăChecklist For Issue of CCDrikitasshahÎncă nu există evaluări

- Company AuditDocument56 paginiCompany Audithiral mitaliaÎncă nu există evaluări

- Mercy Daviz Project Report Secretarial Audit RevisedDocument60 paginiMercy Daviz Project Report Secretarial Audit Revisedmercydaviz100% (1)

- Incorporation of A CompanyDocument26 paginiIncorporation of A CompanySonu Avinash SinghÎncă nu există evaluări

- CH 4 VouchingDocument19 paginiCH 4 VouchingHimanshu UtekarÎncă nu există evaluări

- The Law of Limitation Act 1963Document10 paginiThe Law of Limitation Act 1963mahiÎncă nu există evaluări

- Offences and Penalties Under Goods and Service Tax Act 2017 - An AnalysisDocument16 paginiOffences and Penalties Under Goods and Service Tax Act 2017 - An AnalysisRupal GuptaÎncă nu există evaluări

- GST Drona Material PDFDocument124 paginiGST Drona Material PDFAruna RajappaÎncă nu există evaluări

- Companies (Court) Rules, 1959Document82 paginiCompanies (Court) Rules, 1959tarun.mitra19854923100% (1)

- Departmental Enquiry - ScribdDocument2 paginiDepartmental Enquiry - ScribdSunil Chowdhary100% (1)

- 3.formation of CompanyDocument17 pagini3.formation of CompanyHarsha KharidehalÎncă nu există evaluări

- Maternity Benefit Act 1961Document12 paginiMaternity Benefit Act 1961sachin100% (1)

- Incorporation of CompaniesDocument9 paginiIncorporation of CompaniesAnonymous adXh0LO50% (2)

- Read With Companies (Declaration and Payment of Dividend) Rules, 2014Document27 paginiRead With Companies (Declaration and Payment of Dividend) Rules, 2014nsk2231Încă nu există evaluări

- Chapter - 10 "Company Audit" Section - Wise Index of Chapter X of Companies Act, 2013 Along With Corresponding RulesDocument12 paginiChapter - 10 "Company Audit" Section - Wise Index of Chapter X of Companies Act, 2013 Along With Corresponding RulesfahadÎncă nu există evaluări

- Ch. 6 - The Company Audit CA Study NotesDocument14 paginiCh. 6 - The Company Audit CA Study NotesUnpredictable TalentÎncă nu există evaluări

- Clause 49 Listing AgreementDocument10 paginiClause 49 Listing AgreementAarti MaanÎncă nu există evaluări

- Texhong Textile GroupDocument23 paginiTexhong Textile GroupHatcafe HatcafeÎncă nu există evaluări

- Pors 1 04-Dec-2012 Policy & OthersDocument110 paginiPors 1 04-Dec-2012 Policy & OthersKartik GoyalÎncă nu există evaluări

- AT Quizzer 6 - Fraud ConsiderationDocument10 paginiAT Quizzer 6 - Fraud Considerationlyndon delfinÎncă nu există evaluări

- Reports Linde Annual 2012 GBDocument28 paginiReports Linde Annual 2012 GBRandolph NewtonÎncă nu există evaluări

- ACC3600 NOTES Revised PDFDocument54 paginiACC3600 NOTES Revised PDFKimberly ScullyÎncă nu există evaluări

- Corporate Governance in Ford Motor CompanyDocument14 paginiCorporate Governance in Ford Motor CompanyLarisa Samciuc100% (3)

- External Audit ScopeDocument2 paginiExternal Audit ScopeBennice 8Încă nu există evaluări

- Electosteel Casting Annual Report 2016-2017Document235 paginiElectosteel Casting Annual Report 2016-2017Poonam AggarwalÎncă nu există evaluări

- Becg Corporate Governance:: Notes Complied by Dr. Dhimen Jani Mba, CBS, Pgdibo, PHD MBA Sem. 1Document32 paginiBecg Corporate Governance:: Notes Complied by Dr. Dhimen Jani Mba, CBS, Pgdibo, PHD MBA Sem. 112Twinkal ModiÎncă nu există evaluări

- International Flower Auction Bangalore (IFAB) Limited6Document31 paginiInternational Flower Auction Bangalore (IFAB) Limited6satstarÎncă nu există evaluări

- DilmahDocument55 paginiDilmahDumindaM0% (1)

- Advert AnnualDocument1 paginăAdvert AnnualKabile MwitaÎncă nu există evaluări

- Data Breach Response PlanDocument9 paginiData Breach Response PlanITÎncă nu există evaluări

- Corporate Governanace PPT - PDF-1Document53 paginiCorporate Governanace PPT - PDF-1kahar karishmaÎncă nu există evaluări

- Tata GroupDocument46 paginiTata Groupharsh_199100% (1)

- BDODocument18 paginiBDOReigel Solidum0% (2)

- The Role of Auditors With Their Clients and Third PartiesDocument45 paginiThe Role of Auditors With Their Clients and Third PartiesInamul HaqueÎncă nu există evaluări

- Annual Report 2014Document156 paginiAnnual Report 2014madkiiingÎncă nu există evaluări

- GSK Annual Report 2011Document52 paginiGSK Annual Report 2011bhagyashreefenuÎncă nu există evaluări

- Corporate Governance Factbook Chapter 4Document128 paginiCorporate Governance Factbook Chapter 4kako083Încă nu există evaluări

- Risk Management Policy and FrameworkDocument35 paginiRisk Management Policy and FrameworkPeter TemuÎncă nu există evaluări

- Gov ReviewerDocument7 paginiGov ReviewerAlyssa Grace LecarosÎncă nu există evaluări

- Corporate GovernanceDocument72 paginiCorporate GovernanceNiket RaikangorÎncă nu există evaluări

- Articles of Association: Business Angel NetworkDocument9 paginiArticles of Association: Business Angel NetworkGrigore IoanaÎncă nu există evaluări

- The Nigerian Code of Corporate Governance 2018: Highlights and ImplicationsDocument21 paginiThe Nigerian Code of Corporate Governance 2018: Highlights and ImplicationsrkolarskyÎncă nu există evaluări

- 5 Chapter 2Document173 pagini5 Chapter 2ShrutiÎncă nu există evaluări

- Faqs On Minimum Remuneration To Neds and Independent DirectorsDocument10 paginiFaqs On Minimum Remuneration To Neds and Independent DirectorsShubgamÎncă nu există evaluări

- Annual Report of Lafarge Surma Cement 2012 BangladeshDocument161 paginiAnnual Report of Lafarge Surma Cement 2012 BangladeshAnonymous okVyZFmqqXÎncă nu există evaluări

- Cost Records and Cost AuditDocument21 paginiCost Records and Cost AuditJimitÎncă nu există evaluări