S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Statements PDFDocument4 paginiStatements PDFSami Ullah Khan Larhi78% (9)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Consolidated Cash Flows and Changes in Ownership: Solutions Manual, Chapter 8Document81 paginiConsolidated Cash Flows and Changes in Ownership: Solutions Manual, Chapter 8Gillian Snelling100% (3)

- BA256 Final Exam Review CH 1 Through 7Document19 paginiBA256 Final Exam Review CH 1 Through 7Joey MannÎncă nu există evaluări

- Computer Best Store Accounts Receivable Subsidiary Ledgers: Date Explanation Ref. Debit Credit BalanceDocument60 paginiComputer Best Store Accounts Receivable Subsidiary Ledgers: Date Explanation Ref. Debit Credit BalanceArra StypayhorliksonÎncă nu există evaluări

- Basic Concepts of Guest Accounting - PT 2Document36 paginiBasic Concepts of Guest Accounting - PT 2Leonardo FloresÎncă nu există evaluări

- Objective QuestionsDocument11 paginiObjective Questionsshekarj50% (2)

- Study Material-2 PDFDocument215 paginiStudy Material-2 PDFAnkit KumarÎncă nu există evaluări

- Menu Finacle 10.XDocument63 paginiMenu Finacle 10.XNCSASTRO80% (5)

- Project T.Y.B.Sc.I.T by CalypsoDocument31 paginiProject T.Y.B.Sc.I.T by Calypso3easy3100% (2)

- FSW-Cash Flow 070218Document8 paginiFSW-Cash Flow 070218March AthenaÎncă nu există evaluări

- Configuring The Stock Transport Order: Reset Set Zero Count For Physical InventoryDocument26 paginiConfiguring The Stock Transport Order: Reset Set Zero Count For Physical Inventoryprasadj423Încă nu există evaluări

- ExamDocument18 paginiExamJanine SantiagoÎncă nu există evaluări

- Other Non-Current Financial AssetsDocument7 paginiOther Non-Current Financial AssetsNoella Marie BaronÎncă nu există evaluări

- Accounting Concepts: 1. Business Entity Concept or Separate Entity ConceptDocument4 paginiAccounting Concepts: 1. Business Entity Concept or Separate Entity ConceptTawanda Tatenda HerbertÎncă nu există evaluări

- AKM 2E Testbank Chapter 18Document50 paginiAKM 2E Testbank Chapter 18ANNISA AMALIA SALSABIILAÎncă nu există evaluări

- 40 FICO Tips-Very UsefulDocument10 pagini40 FICO Tips-Very UsefulRajesh KumarÎncă nu există evaluări

- 5 Worksheet FormatDocument1 pagină5 Worksheet FormatRJ DAVE DURUHAÎncă nu există evaluări

- Fabm1 & 2 - ReviewDocument77 paginiFabm1 & 2 - ReviewBernice Jayne MondingÎncă nu există evaluări

- CA CPT December 2012 Paper SolutionDocument14 paginiCA CPT December 2012 Paper Solutionvivekagarwal5425Încă nu există evaluări

- Confras Transes Module 1 and 2Document16 paginiConfras Transes Module 1 and 2Cielo MINDANAOÎncă nu există evaluări

- Branch AccountingDocument44 paginiBranch Accountingaruna2707100% (1)

- CTA2021 FAC48624 Term 3 Lecture Notes 13052021Document54 paginiCTA2021 FAC48624 Term 3 Lecture Notes 13052021Tatenda TakaindisaÎncă nu există evaluări

- Notes On Cash and Cash EquivalentsDocument1 paginăNotes On Cash and Cash EquivalentsMariz Julian Pang-aoÎncă nu există evaluări

- ST Pocket MoneyDocument4 paginiST Pocket MoneyLincoln LowÎncă nu există evaluări

- Basic Concepts 1Document42 paginiBasic Concepts 1puneet80% (5)

- Partnership Formation Partnership AccountingDocument14 paginiPartnership Formation Partnership AccountingJesseca JosafatÎncă nu există evaluări

- MCOM - Ac - Paper - IDocument542 paginiMCOM - Ac - Paper - IKaran BindraÎncă nu există evaluări

- Little Book of LegacyDocument20 paginiLittle Book of Legacyrhythems84Încă nu există evaluări

- Cambridge IGCSE: Accounting 0452/11Document12 paginiCambridge IGCSE: Accounting 0452/11Tamer AhmedÎncă nu există evaluări

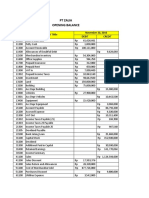

- PT. ZALIA - Aulia Rahmiyatul AzmaDocument49 paginiPT. ZALIA - Aulia Rahmiyatul AzmaFARAH KALTSUM HANIFAH100% (1)