S-ar putea să vă placă și

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Case Study On Strategic Management 2Document8 paginiCase Study On Strategic Management 2Mamta SharmaÎncă nu există evaluări

- Functions of Accounting Department: 1. BookkeepingDocument3 paginiFunctions of Accounting Department: 1. BookkeepingMadhusudhan TantriÎncă nu există evaluări

- Limited Liabilities Partnership FirmDocument14 paginiLimited Liabilities Partnership FirmPraveen JoeÎncă nu există evaluări

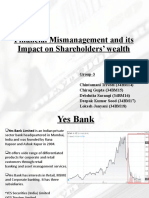

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 paginiGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodÎncă nu există evaluări

- Name: Kimberly Anne P. Caballes Year and CourseDocument12 paginiName: Kimberly Anne P. Caballes Year and CourseKimberly Anne CaballesÎncă nu există evaluări

- Profit Maximization Vs Stockholders' Wealth MaximizationDocument10 paginiProfit Maximization Vs Stockholders' Wealth MaximizationMarienell YuÎncă nu există evaluări

- Lesson Plan - Business OwnershipDocument3 paginiLesson Plan - Business OwnershipJennifer Dela RosaÎncă nu există evaluări

- Analysis of Audited Financial Statements of San Miguel Corporation 2021Document28 paginiAnalysis of Audited Financial Statements of San Miguel Corporation 2021Marquez, Jazzmine K.Încă nu există evaluări

- TYBAF Project TopicsDocument2 paginiTYBAF Project Topicsseema mundaleÎncă nu există evaluări

- Lagrimas, Sarah Nicole S. - Bio Assets PDFDocument9 paginiLagrimas, Sarah Nicole S. - Bio Assets PDFSarah Nicole S. LagrimasÎncă nu există evaluări

- SMC Financial Statements 2012Document104 paginiSMC Financial Statements 2012Christian D. OrbeÎncă nu există evaluări

- Deloitte-FAS Corporate Finance BrochureDocument12 paginiDeloitte-FAS Corporate Finance BrochureKen TO100% (1)

- AF CHP 9Document27 paginiAF CHP 9Jeffry AshariÎncă nu există evaluări

- Board or Shareholders - Resolution-08092018Document1 paginăBoard or Shareholders - Resolution-08092018Meenakshi Ogra MukherjeeÎncă nu există evaluări

- LIT1 Task 1Document6 paginiLIT1 Task 1Nate OtikerÎncă nu există evaluări

- FRM Mcq'sDocument69 paginiFRM Mcq'sAakash Kathuria0% (3)

- Afisco Insurance Corporation v. CA 302 SCRA 1Document2 paginiAfisco Insurance Corporation v. CA 302 SCRA 1Kayee KatÎncă nu există evaluări

- Ambit Strategy Thematic TenBaggers5 05jan2016 PDFDocument28 paginiAmbit Strategy Thematic TenBaggers5 05jan2016 PDFVikas TiwariÎncă nu există evaluări

- 07.ind As 102Document35 pagini07.ind As 102Pranjul AgrawalÎncă nu există evaluări

- Problems in AccountingDocument4 paginiProblems in AccountingRaul Soriano CabantingÎncă nu există evaluări

- Unit 3 CDocument14 paginiUnit 3 Cmusic niÎncă nu există evaluări

- IDX Annually 2013Document141 paginiIDX Annually 2013Sheren reginaÎncă nu există evaluări

- "Financial Statement Analysis of Bank of Maharashtra": A Project Report OnDocument65 pagini"Financial Statement Analysis of Bank of Maharashtra": A Project Report OnShashi RanjanÎncă nu există evaluări

- Financial Statements Are Prepared According To A Number of AccountingDocument1 paginăFinancial Statements Are Prepared According To A Number of AccountingTaimur TechnologistÎncă nu există evaluări

- Ias 16Document21 paginiIas 16Arshad BhuttaÎncă nu există evaluări

- Quiz Valuation Prelim: C. Statement 1 Is False, Statement 2 Is TrueDocument2 paginiQuiz Valuation Prelim: C. Statement 1 Is False, Statement 2 Is TrueUNKNOWNN50% (2)

- ACCO 30103 CORPLIQ-Statement of Affairs and Deficiency Statement 04-2022Document3 paginiACCO 30103 CORPLIQ-Statement of Affairs and Deficiency Statement 04-2022Zyrille Corrine GironÎncă nu există evaluări

- Discussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument3 paginiDiscussion Problems: Manila Cavite Laguna Cebu Cagayan de Oro DavaoTatianaÎncă nu există evaluări

- Affidavit of Loss Stock and Transfer BookDocument1 paginăAffidavit of Loss Stock and Transfer BookA&L Consulting100% (1)

- It FinalsDocument11 paginiIt FinalsHea Jennifer AyopÎncă nu există evaluări