S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- On How To Design A Low Voltage SwitchboardDocument11 paginiOn How To Design A Low Voltage SwitchboardsabeerÎncă nu există evaluări

- Textbook of Dental Anatomy, Physiology and Occlusion, 1E (2014) (PDF) (UnitedVRG)Document382 paginiTextbook of Dental Anatomy, Physiology and Occlusion, 1E (2014) (PDF) (UnitedVRG)Konstantinos Ster90% (20)

- Pamet and PasmethDocument4 paginiPamet and PasmethBash De Guzman50% (2)

- Content Map PE & Health 12Document12 paginiContent Map PE & Health 12RIZZA MEA DOLOSOÎncă nu există evaluări

- OM Mannual FOsDocument38 paginiOM Mannual FOsAbdulmuqtadetr AhmadiÎncă nu există evaluări

- Top 6 Beginner Work Out MistakesDocument4 paginiTop 6 Beginner Work Out MistakesMARYAM GULÎncă nu există evaluări

- Logiq e r7 SMDocument435 paginiLogiq e r7 SMAroÎncă nu există evaluări

- Idioms and PharsesDocument0 paginiIdioms and PharsesPratik Ramesh Pappali100% (1)

- T W H O Q L (Whoqol) - Bref: Skrócona Wersja Ankiety Oceniającej Jakość ŻyciaDocument6 paginiT W H O Q L (Whoqol) - Bref: Skrócona Wersja Ankiety Oceniającej Jakość ŻyciaPiotrÎncă nu există evaluări

- W01 M58 6984Document30 paginiW01 M58 6984MROstop.comÎncă nu există evaluări

- Chef Basics Favorite RecipesDocument58 paginiChef Basics Favorite Recipesbillymac303a100% (2)

- OBESITY - Cayce Health DatabaseDocument4 paginiOBESITY - Cayce Health Databasewcwjr55Încă nu există evaluări

- FiltrationDocument22 paginiFiltrationYeabsira WorkagegnehuÎncă nu există evaluări

- Market Pulse Q4 Report - Nielsen Viet Nam: Prepared by Nielsen Vietnam February 2017Document8 paginiMarket Pulse Q4 Report - Nielsen Viet Nam: Prepared by Nielsen Vietnam February 2017K57.CTTT BUI NGUYEN HUONG LYÎncă nu există evaluări

- Learning Activity Sheet General Chemistry 2 (Q4 - Lessons 7 and 8) Electrochemical ReactionsDocument11 paginiLearning Activity Sheet General Chemistry 2 (Q4 - Lessons 7 and 8) Electrochemical Reactionsprincess3canlasÎncă nu există evaluări

- Unmasking Pleural Mesothelioma: A Silent ThreatDocument11 paginiUnmasking Pleural Mesothelioma: A Silent ThreatCathenna DesuzaÎncă nu există evaluări

- Ancamine Teta UsDocument2 paginiAncamine Teta UssimphiweÎncă nu există evaluări

- Ams - 4640-C63000 Aluminium Nickel MNDocument3 paginiAms - 4640-C63000 Aluminium Nickel MNOrnella MancinelliÎncă nu există evaluări

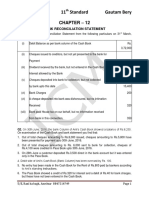

- BRS PDFDocument14 paginiBRS PDFGautam KhanwaniÎncă nu există evaluări

- Women and International Human Rights Law PDFDocument67 paginiWomen and International Human Rights Law PDFakilasriÎncă nu există evaluări

- URICA TestDocument3 paginiURICA TestCristy PagalanÎncă nu există evaluări

- Containers HandbookDocument26 paginiContainers Handbookrishi vohraÎncă nu există evaluări

- Factors That Contribute To Successful BakingDocument8 paginiFactors That Contribute To Successful BakingErrol San Juan100% (1)

- Sampoong Department Store - A Literary Critique (Mimetic Theory)Document2 paginiSampoong Department Store - A Literary Critique (Mimetic Theory)Ron Marc CaneteÎncă nu există evaluări

- HDFC Life Insurance (HDFCLIFE) : 2. P/E 58 3. Book Value (RS) 23.57Document5 paginiHDFC Life Insurance (HDFCLIFE) : 2. P/E 58 3. Book Value (RS) 23.57Srini VasanÎncă nu există evaluări

- Musa Paradisiaca L. and Musa Sapientum L.: A Phytochemical and Pharmacological ReviewDocument8 paginiMusa Paradisiaca L. and Musa Sapientum L.: A Phytochemical and Pharmacological ReviewDeviÎncă nu există evaluări

- Evidence-Based Strength & HypertrophyDocument6 paginiEvidence-Based Strength & HypertrophyAnže BenkoÎncă nu există evaluări

- Celitron ISS 25L - Product Spec Sheet V 2.1 enDocument9 paginiCelitron ISS 25L - Product Spec Sheet V 2.1 enyogadwiprasetyo8_161Încă nu există evaluări

- NCP Ineffective Breathing ActualDocument3 paginiNCP Ineffective Breathing ActualArian May Marcos100% (1)

- Allison Weech Final ResumeDocument1 paginăAllison Weech Final Resumeapi-506177291Încă nu există evaluări