S-ar putea să vă placă și

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- revision كورس سنه تانية اخيرDocument2 paginirevision كورس سنه تانية اخيرMagdy KamelÎncă nu există evaluări

- Financial Reporting and Accounting Standards: Chapter Learning ObjectivesDocument12 paginiFinancial Reporting and Accounting Standards: Chapter Learning ObjectivesMagdy KamelÎncă nu există evaluări

- Barclays Reveals2014-QuestionDocument10 paginiBarclays Reveals2014-QuestionMagdy KamelÎncă nu există evaluări

- Final Revision Part 2 Language (2st)Document21 paginiFinal Revision Part 2 Language (2st)Magdy KamelÎncă nu există evaluări

- Sheet (3) : Corporations: Dividends, Retained Earnings, and Income ReportingDocument28 paginiSheet (3) : Corporations: Dividends, Retained Earnings, and Income ReportingMagdy KamelÎncă nu există evaluări

- Faculty of Commerce Year: Statistics May 2020 Time: Three Hours - Date: 31/5/2020 The Questions Start With A Number: (7) RequiredDocument12 paginiFaculty of Commerce Year: Statistics May 2020 Time: Three Hours - Date: 31/5/2020 The Questions Start With A Number: (7) RequiredMagdy KamelÎncă nu există evaluări

- solution of math first امتحانDocument8 paginisolution of math first امتحانMagdy KamelÎncă nu există evaluări

- Second 22Document11 paginiSecond 22Magdy KamelÎncă nu există evaluări

- O o o o o o o O: 11) John Maynard KeynesDocument17 paginiO o o o o o o O: 11) John Maynard KeynesMagdy KamelÎncă nu există evaluări

- Public Administration - ExamDocument6 paginiPublic Administration - ExamMagdy KamelÎncă nu există evaluări

- 1Document42 pagini1Magdy KamelÎncă nu există evaluări

- Exam StatDocument11 paginiExam StatMagdy KamelÎncă nu există evaluări

- Intermediate Accounting Test Bank Chapter 18Document3 paginiIntermediate Accounting Test Bank Chapter 18Magdy Kamel33% (3)

- ResourceDocument7 paginiResourceMagdy KamelÎncă nu există evaluări

- Going Concern AssumptionDocument1 paginăGoing Concern AssumptionMagdy KamelÎncă nu există evaluări

- Second Semester 2020 Second Year University of Assuit Faculty of Commerce English Program " Corporation" "Test Bank"Document10 paginiSecond Semester 2020 Second Year University of Assuit Faculty of Commerce English Program " Corporation" "Test Bank"Magdy KamelÎncă nu există evaluări

- Assiut University - Faculty of CommerceDocument17 paginiAssiut University - Faculty of CommerceMagdy KamelÎncă nu există evaluări

- O False o FalseDocument9 paginiO False o FalseMagdy KamelÎncă nu există evaluări

- Dr. Nagla Shalaby Please Choose The Correct AnswerDocument3 paginiDr. Nagla Shalaby Please Choose The Correct AnswerMagdy KamelÎncă nu există evaluări

- ExDocument5 paginiExMagdy KamelÎncă nu există evaluări

- 104Document8 pagini104Magdy Kamel100% (1)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Norvald Monsen Cameral Accounting As An Alternative To Accrual Accounting WWW Icgfm OrgDocument10 paginiNorvald Monsen Cameral Accounting As An Alternative To Accrual Accounting WWW Icgfm OrgFreeBalanceGRP100% (5)

- 03 Financial Statement AnalysisDocument46 pagini03 Financial Statement Analysissimao.lipscombÎncă nu există evaluări

- Accounting For Lawyers Exam OutlineDocument37 paginiAccounting For Lawyers Exam OutlineJesse Danoff100% (1)

- CH 03Document48 paginiCH 03kevin echiverriÎncă nu există evaluări

- Dwnload Full Financial Accounting A Business Process Approach 3rd Edition Reimers Solutions Manual PDFDocument25 paginiDwnload Full Financial Accounting A Business Process Approach 3rd Edition Reimers Solutions Manual PDFjosephkvqhperez100% (11)

- Solution To Chapter 21Document25 paginiSolution To Chapter 21Sy Him100% (5)

- Week 4 Practice Questions 1Document17 paginiWeek 4 Practice Questions 1Gabriel Abdillah100% (1)

- Financial Modeling Using Excel Mergers and Acquisitions: WWW - Yerite.co - inDocument43 paginiFinancial Modeling Using Excel Mergers and Acquisitions: WWW - Yerite.co - inUJJWALÎncă nu există evaluări

- John A., CPA Tracy, Tage Tracy - How To Manage Profit and Cash Flow - Mining The Numbers For Gold (2004) PDFDocument242 paginiJohn A., CPA Tracy, Tage Tracy - How To Manage Profit and Cash Flow - Mining The Numbers For Gold (2004) PDFPatman MutomboÎncă nu există evaluări

- Akm E7-9 P7-3 P7-6 P7-13Document5 paginiAkm E7-9 P7-3 P7-6 P7-13tira sundayÎncă nu există evaluări

- Chapter 2 - Statement of Comprehensive IncomeDocument12 paginiChapter 2 - Statement of Comprehensive IncomeVictor TucoÎncă nu există evaluări

- Subject: Accountancy: Kendriya Vidyalaya Sangathan Guwahati RegionDocument170 paginiSubject: Accountancy: Kendriya Vidyalaya Sangathan Guwahati RegionHimangi AgarwalÎncă nu există evaluări

- PPT2 AnsDocument5 paginiPPT2 Anskristelle0marisseÎncă nu există evaluări

- Solutions Lecture 1Document7 paginiSolutions Lecture 1jojoinnit100% (2)

- CF EstimationDocument97 paginiCF Estimationdanish khanÎncă nu există evaluări

- Practice ques-CVP AnalysisDocument5 paginiPractice ques-CVP AnalysisSuchita GaonkarÎncă nu există evaluări

- Solutions To Chapter 11 - Exercises 1 - 13Document36 paginiSolutions To Chapter 11 - Exercises 1 - 13Claire BarbaÎncă nu există evaluări

- Iaasb Isa 810 RevisedDocument31 paginiIaasb Isa 810 RevisedGlenn TaduranÎncă nu există evaluări

- Adoption of New StandardsDocument6 paginiAdoption of New StandardsRievaÎncă nu există evaluări

- BBA (MOM) - 109 Financial AccountingDocument2 paginiBBA (MOM) - 109 Financial AccountingGaurav JainÎncă nu există evaluări

- Financial Statement Analysis Group Exercise: InstructionsDocument1 paginăFinancial Statement Analysis Group Exercise: InstructionsJays DomeÎncă nu există evaluări

- Finance Applications and Theory 4Th Edition Cornett Solutions Manual Full Chapter PDFDocument42 paginiFinance Applications and Theory 4Th Edition Cornett Solutions Manual Full Chapter PDFheulwenvalerie7dr100% (12)

- Working Capital Management - 131218Document39 paginiWorking Capital Management - 131218bhumika manwaniÎncă nu există evaluări

- CH 14 Var Vs Abs CostingDocument60 paginiCH 14 Var Vs Abs CostingShannon BánañasÎncă nu există evaluări

- Marcus AgDocument4 paginiMarcus AgMosesÎncă nu există evaluări

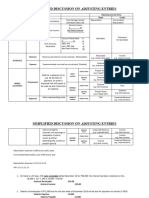

- Kinds of Adjusting Entries 1Document2 paginiKinds of Adjusting Entries 1Marc Justine Gamiao GoÎncă nu există evaluări

- Study Guide FAC3704Document241 paginiStudy Guide FAC3704Takudzwa Benjamin100% (1)

- FR Question BankDocument348 paginiFR Question BankSajjad Hosen Pavel50% (2)

- Capital Budgeting - FinmarDocument3 paginiCapital Budgeting - FinmarnerieroseÎncă nu există evaluări

- FINMAN Cash-Flow-Analysis-Practice-Problem-2Document2 paginiFINMAN Cash-Flow-Analysis-Practice-Problem-2stel mariÎncă nu există evaluări