S-ar putea să vă placă și

- Cryptocurrency and the Incompatibility with the Current Banking System: CRYPTOCURRENCYDe la EverandCryptocurrency and the Incompatibility with the Current Banking System: CRYPTOCURRENCYÎncă nu există evaluări

- Money Laundering CH4Document79 paginiMoney Laundering CH4saliyarumesh2292Încă nu există evaluări

- Money Laundering Methods & PreventionDocument7 paginiMoney Laundering Methods & Preventionvaishnav reddy100% (1)

- New Trends in Money Laundering. From The Real World To CyberspaceDocument9 paginiNew Trends in Money Laundering. From The Real World To CyberspaceAlberta RieraÎncă nu există evaluări

- Remittances, Payments, and Money Transfers: Behaviors of South Asians and IndonesiansDocument83 paginiRemittances, Payments, and Money Transfers: Behaviors of South Asians and Indonesiansprabin ghimireÎncă nu există evaluări

- Macau's New AML Rules Impact U.S.-Based CasinosDocument4 paginiMacau's New AML Rules Impact U.S.-Based CasinosSpyp PadyÎncă nu există evaluări

- The Dot-ConDocument66 paginiThe Dot-ConMohammadOmarFaruqÎncă nu există evaluări

- Dubai's Golden SandsDocument17 paginiDubai's Golden SandsscrbdfanÎncă nu există evaluări

- Aml& CFTDocument2 paginiAml& CFTTeerath KumarÎncă nu există evaluări

- ZYDUSLIFE 30052022203428 DLOFCoverLetterExchangesdt30052022Document81 paginiZYDUSLIFE 30052022203428 DLOFCoverLetterExchangesdt30052022Swarup JadhavÎncă nu există evaluări

- PD Digital Currency v.14 14.12.17Document51 paginiPD Digital Currency v.14 14.12.17Li ZhenÎncă nu există evaluări

- The Hawala SystemDocument11 paginiThe Hawala SystemnewtomiÎncă nu există evaluări

- FCA Review of Trade Based Money LaunderingDocument52 paginiFCA Review of Trade Based Money LaunderingvarunnatarajanÎncă nu există evaluări

- Statement of Facts - USA Vs Ilya Lichtenstein & Heather Rhiannon MorganDocument20 paginiStatement of Facts - USA Vs Ilya Lichtenstein & Heather Rhiannon MorganhyenadogÎncă nu există evaluări

- Money Laundering Using CryptocurrencyDocument12 paginiMoney Laundering Using CryptocurrencyWaleed KhanÎncă nu există evaluări

- HawalaDocument38 paginiHawalaKhundongbam SureshÎncă nu există evaluări

- Derivative Strategies: Research Paper OnDocument13 paginiDerivative Strategies: Research Paper OnSapna KesurÎncă nu există evaluări

- MintMark23 4Q FinalDocument10 paginiMintMark23 4Q FinalAmericanNumismaticÎncă nu există evaluări

- Parallel EconomyDocument30 paginiParallel EconomyaakashkagarwalÎncă nu există evaluări

- Follow The Money Tracing Terrorist AssetsDocument78 paginiFollow The Money Tracing Terrorist AssetsStefan STÎncă nu există evaluări

- BCC Bitconnect Lending PlanDocument8 paginiBCC Bitconnect Lending PlanJenny SharmaÎncă nu există evaluări

- Forensics Training Masterclass Module - 1Document27 paginiForensics Training Masterclass Module - 1jndayizigiye17Încă nu există evaluări

- Fatf PDFDocument42 paginiFatf PDFHEMANT SARVANKARÎncă nu există evaluări

- Raza ZarrabDocument55 paginiRaza ZarrabJon TurkÎncă nu există evaluări

- ZAAD Charging ProposalDocument28 paginiZAAD Charging ProposalHoyaalay67% (3)

- Money Laundring Khanani and KaliaDocument6 paginiMoney Laundring Khanani and KaliaHassanAhmadÎncă nu există evaluări

- Terrorist Use of CryptocurrenciesDocument22 paginiTerrorist Use of CryptocurrenciesSimone D. Casadei BernardiÎncă nu există evaluări

- Money LaunderingDocument3 paginiMoney LaunderingJasmin MirandaÎncă nu există evaluări

- CounterfeitingDocument4 paginiCounterfeitingPEDRO ANTONIO LORZAÎncă nu există evaluări

- Corruption of Foreign Public Officials ActDocument15 paginiCorruption of Foreign Public Officials Actjonkhan84Încă nu există evaluări

- Frauds & Scams in BanksDocument15 paginiFrauds & Scams in Banksakshay virkarÎncă nu există evaluări

- Money Laundering Terrorist Financing Art Antiquities MarketDocument60 paginiMoney Laundering Terrorist Financing Art Antiquities MarketLynda AlbertsonÎncă nu există evaluări

- Uncover India's Biggest Political Scandal - HawalaDocument5 paginiUncover India's Biggest Political Scandal - HawalaAyush JainÎncă nu există evaluări

- FEND Off Fentanyl Act TextDocument21 paginiFEND Off Fentanyl Act TextDaily Caller News FoundationÎncă nu există evaluări

- Case Evidence and Details LebowitzLPR 2 3 PDFDocument19 paginiCase Evidence and Details LebowitzLPR 2 3 PDFAnonymous xm0nAXZÎncă nu există evaluări

- 3.30 Hawley Letter To Mayorkas CBP OneDocument2 pagini3.30 Hawley Letter To Mayorkas CBP OneFox NewsÎncă nu există evaluări

- Hawala Money Transfer System ExplainedDocument9 paginiHawala Money Transfer System ExplainedasdfÎncă nu există evaluări

- Cryptocurrency JudgmentDocument180 paginiCryptocurrency Judgmentmrinal lalÎncă nu există evaluări

- AML by HossamDocument4 paginiAML by HossamAsim RajputÎncă nu există evaluări

- Combating Money Laundering in Nigeria - A Legal Perspective On The Role of Central and Commercial Banks, ChitengiDocument84 paginiCombating Money Laundering in Nigeria - A Legal Perspective On The Role of Central and Commercial Banks, ChitengiCHITENGI SIPHO JUSTINE, PhD Candidate- Law & Policy100% (1)

- Thomas Traficante Criminal ComplaintDocument16 paginiThomas Traficante Criminal ComplaintThe Livingston County NewsÎncă nu există evaluări

- Bitcoin ManipDocument89 paginiBitcoin ManipAnonymous NKPsAVwÎncă nu există evaluări

- INL Guide To Open DataDocument9 paginiINL Guide To Open DataH RÎncă nu există evaluări

- SGV Anti-Money Laundering (AML) and Counter Terrorist Financing (CTF) Seminar Series For The Year 2020Document4 paginiSGV Anti-Money Laundering (AML) and Counter Terrorist Financing (CTF) Seminar Series For The Year 2020jayrenielÎncă nu există evaluări

- MarketPeak Academy Business Model-Feb 2022Document49 paginiMarketPeak Academy Business Model-Feb 2022Upendra YadavÎncă nu există evaluări

- The Obstacles To Regulating The Hawala - A Cultural Norm or A TerrDocument57 paginiThe Obstacles To Regulating The Hawala - A Cultural Norm or A TerrBrendan LanzaÎncă nu există evaluări

- WoodfordDocument4 paginiWoodfordDestiny RiveraÎncă nu există evaluări

- BLP Presentaion Group 4Document24 paginiBLP Presentaion Group 4Bhavya UdiniaÎncă nu există evaluări

- A 美国大麻投资报告 (100P) U S Cannabis Investment Report 2016 PDFDocument118 paginiA 美国大麻投资报告 (100P) U S Cannabis Investment Report 2016 PDFDanny ZhangÎncă nu există evaluări

- Money Laundering and Central Bank Governance in The European UnionDocument37 paginiMoney Laundering and Central Bank Governance in The European UnionairwanÎncă nu există evaluări

- Leading Asset Manager Uses AutoRek To Improve AML Transaction Monitoring ProcessesDocument5 paginiLeading Asset Manager Uses AutoRek To Improve AML Transaction Monitoring ProcessesrockonsmileÎncă nu există evaluări

- TestimonyDocument27 paginiTestimonyMichaelPatrickMcSweeneyÎncă nu există evaluări

- Fiat Money: Confusing The Form of Money With Its Social ContentDocument26 paginiFiat Money: Confusing The Form of Money With Its Social ContentfelipejvcÎncă nu există evaluări

- Tanzania Governance Review 2014 :the Year of Escrow'Document160 paginiTanzania Governance Review 2014 :the Year of Escrow'Policy ForumÎncă nu există evaluări

- Request For Consultation - Victims ReplyDocument8 paginiRequest For Consultation - Victims ReplyDr. Jonathan Levy, PhDÎncă nu există evaluări

- Joseph Saveri Law Firm, Inc.: Counsel For Individual and Representative Plaintiffs Shane Cheng and Terell SterlingDocument55 paginiJoseph Saveri Law Firm, Inc.: Counsel For Individual and Representative Plaintiffs Shane Cheng and Terell Sterlingmichaelkan1Încă nu există evaluări

- Ramachandran Homeland Security Testimony - 01.20.22Document21 paginiRamachandran Homeland Security Testimony - 01.20.22The Brennan Center for JusticeÎncă nu există evaluări

- Worldwide Select I 00 AlmaDocument130 paginiWorldwide Select I 00 AlmaRyan WalkerÎncă nu există evaluări

- Seminar7 Group Discussion1cDocument55 paginiSeminar7 Group Discussion1cMytee TarasonÎncă nu există evaluări

- Economic SystemDocument3 paginiEconomic SystemNakama HouseÎncă nu există evaluări

- Economic SystemDocument3 paginiEconomic SystemNakama HouseÎncă nu există evaluări

- The Potential of Coffee PDFDocument100 paginiThe Potential of Coffee PDFNakama HouseÎncă nu există evaluări

- The Potential of Coffee PDFDocument100 paginiThe Potential of Coffee PDFNakama HouseÎncă nu există evaluări

- Vehicle Project Proposal..11Document3 paginiVehicle Project Proposal..11Nakama House85% (13)

- Chicken PRoject UGANDA SPACE PROPOSALDocument19 paginiChicken PRoject UGANDA SPACE PROPOSALBenes Hernandez Dopitillo0% (3)

- Vehicle Project Proposal..11Document3 paginiVehicle Project Proposal..11Nakama House85% (13)

- GENDER - Agriculture. 1Document6 paginiGENDER - Agriculture. 1Nakama HouseÎncă nu există evaluări

- Training Manual and Handling GuideDocument5 paginiTraining Manual and Handling GuideNakama HouseÎncă nu există evaluări

- Quiz - Quiz 2 Partnership Dissolution and Liquidation AnswersDocument15 paginiQuiz - Quiz 2 Partnership Dissolution and Liquidation AnswersKent Zirkai CidroÎncă nu există evaluări

- TRM N61 V JC OMTKD7Document8 paginiTRM N61 V JC OMTKD7Mukesh Kumar DubeyÎncă nu există evaluări

- Siam Cement's $921M foreign exchange lossDocument5 paginiSiam Cement's $921M foreign exchange lossKesarapu Venkata ApparaoÎncă nu există evaluări

- МСА 2016-2017 частина 2Document644 paginiМСА 2016-2017 частина 2Валентина ЖдановаÎncă nu există evaluări

- CBA FM PE - Life Insurance - Group2Document7 paginiCBA FM PE - Life Insurance - Group2Janna Glaiza FernandezÎncă nu există evaluări

- Board of Directors StructureDocument3 paginiBoard of Directors StructureMoamar Dalawis IsmulaÎncă nu există evaluări

- FMAP DirectoryDocument78 paginiFMAP DirectoryZeshan Choudhry100% (1)

- Twelve Cases of AccountingDocument152 paginiTwelve Cases of AccountingregiscardosoÎncă nu există evaluări

- GST Payment Challan Form NEFT DetailsDocument2 paginiGST Payment Challan Form NEFT DetailsSunil KalraÎncă nu există evaluări

- Ebook Corporate Finance A Focused Approach 5Th Edition Ehrhardt Solutions Manual Full Chapter PDFDocument43 paginiEbook Corporate Finance A Focused Approach 5Th Edition Ehrhardt Solutions Manual Full Chapter PDFquachhaitpit100% (9)

- The Following Is The Unadjusted Trial Balance For Rainbow LodgeDocument3 paginiThe Following Is The Unadjusted Trial Balance For Rainbow LodgeCharlotteÎncă nu există evaluări

- Insurance Act 2049 SummaryDocument26 paginiInsurance Act 2049 Summarysujata dawadiÎncă nu există evaluări

- Ninjavan PayslipDocument3 paginiNinjavan PayslipGerry Boy BailonÎncă nu există evaluări

- Important Banking Financial Terms For RBI Grade B Phase II NABARD DA Mains IBPS PO Mains PDFDocument21 paginiImportant Banking Financial Terms For RBI Grade B Phase II NABARD DA Mains IBPS PO Mains PDFk vinayÎncă nu există evaluări

- Insurance Industry: United Arab EmiratesDocument44 paginiInsurance Industry: United Arab EmiratesHaris MansoorÎncă nu există evaluări

- 4ac1 01 Que 20231103Document20 pagini4ac1 01 Que 20231103Sadat RahmanÎncă nu există evaluări

- Akuntansi Chapter 4Document23 paginiAkuntansi Chapter 4Alfian Rizal MahendraÎncă nu există evaluări

- Investment Declaration Form 2012-13 PDFDocument1 paginăInvestment Declaration Form 2012-13 PDFnovalhemantÎncă nu există evaluări

- Acc Assignment Merge UpdatedDocument9 paginiAcc Assignment Merge UpdatedDEEVEYAH A/P S.RAMASI / UPMÎncă nu există evaluări

- Insurance NotesDocument61 paginiInsurance NotesIvyGwynn214Încă nu există evaluări

- Week5.Millan - Chapter 7 - Posting To The LedgerDocument13 paginiWeek5.Millan - Chapter 7 - Posting To The LedgerAngel BambaÎncă nu există evaluări

- Financial Planning Tools and ConceptsDocument3 paginiFinancial Planning Tools and ConceptsBea H.Încă nu există evaluări

- Institute and Faculty of Actuaries: Subject SA2 - Life Insurance Specialist ApplicationsDocument5 paginiInstitute and Faculty of Actuaries: Subject SA2 - Life Insurance Specialist Applicationsdickson phiriÎncă nu există evaluări

- Lesson No 4 Banking: 1. Which of The Following Banking Services Does The Customer Normally Have To Pay For?Document4 paginiLesson No 4 Banking: 1. Which of The Following Banking Services Does The Customer Normally Have To Pay For?Gamers CannabitÎncă nu există evaluări

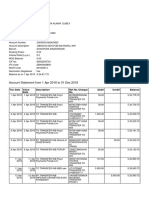

- Member Statements-04302021Document2 paginiMember Statements-04302021bÎncă nu există evaluări

- Indian Meteorological Society Form For Enrollment Proposal For Individual MembershipDocument1 paginăIndian Meteorological Society Form For Enrollment Proposal For Individual Membershipcaptainnkumar1043Încă nu există evaluări

- Analisis Tingkat Kesehatan Bank Dengan Menggunakan Metode Camel Pada PT - Bank Syariah Mandiri (PERIODE 2001-2010) SkripsiDocument98 paginiAnalisis Tingkat Kesehatan Bank Dengan Menggunakan Metode Camel Pada PT - Bank Syariah Mandiri (PERIODE 2001-2010) SkripsiARYA AZHARI -Încă nu există evaluări

- Wealth-Lab Developer 6.9 Performance: Strategy: Channel Breakout VT Dataset/Symbol: AALDocument1 paginăWealth-Lab Developer 6.9 Performance: Strategy: Channel Breakout VT Dataset/Symbol: AALHamahid pourÎncă nu există evaluări

- AccountStatement-1Document1 paginăAccountStatement-1hraza5263Încă nu există evaluări

- Niif Pymes 2015Document30 paginiNiif Pymes 2015Allan VelasquezÎncă nu există evaluări