S-ar putea să vă placă și

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Profiling Form - AwraDocument2 paginiProfiling Form - AwraBlaceÎncă nu există evaluări

- The 53 Questions:: 1. Was The Plan of Salvation Made After The Fall?Document54 paginiThe 53 Questions:: 1. Was The Plan of Salvation Made After The Fall?BlaceÎncă nu există evaluări

- Christ Centered LifeDocument2 paginiChrist Centered LifeBlaceÎncă nu există evaluări

- How To Survive With GodDocument5 paginiHow To Survive With GodBlaceÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Superstocks Final Advance Reviewer'sDocument250 paginiSuperstocks Final Advance Reviewer'sbanman8796% (24)

- Byju'S Global Expansion: International Business ProjectDocument13 paginiByju'S Global Expansion: International Business ProjectGauravÎncă nu există evaluări

- Important InformationDocument193 paginiImportant InformationDharmendra KumarÎncă nu există evaluări

- Pradhan Mantri Awas Yojana PDFDocument17 paginiPradhan Mantri Awas Yojana PDFKD Ltd.Încă nu există evaluări

- Maruti Suzuki Strives To Consistently Improve The Environmental Performance of Its Manufacturing OperationsDocument6 paginiMaruti Suzuki Strives To Consistently Improve The Environmental Performance of Its Manufacturing OperationsandljnnjdsÎncă nu există evaluări

- Ten Principles of UN Global CompactDocument2 paginiTen Principles of UN Global CompactrisefoxÎncă nu există evaluări

- HBA - 25 Lakhs Order PDFDocument4 paginiHBA - 25 Lakhs Order PDFkarik1897Încă nu există evaluări

- 11th 12th Economics Q EM Sample PagesDocument27 pagini11th 12th Economics Q EM Sample PagesKirthika RajaÎncă nu există evaluări

- TOEFLDocument15 paginiTOEFLMega Suci LestariÎncă nu există evaluări

- Comparative Cost AdvantageDocument4 paginiComparative Cost AdvantageSrutiÎncă nu există evaluări

- Nabl 500Document142 paginiNabl 500Vinay SimhaÎncă nu există evaluări

- Cambridge International Advanced Subsidiary and Advanced LevelDocument8 paginiCambridge International Advanced Subsidiary and Advanced LevelNguyễn QuânÎncă nu există evaluări

- Veit Tunel 1Document7 paginiVeit Tunel 1Bladimir SolizÎncă nu există evaluări

- 2.01 Economic SystemsDocument16 pagini2.01 Economic SystemsRessie Joy Catherine FelicesÎncă nu există evaluări

- Commissioner of Internal Revenue vs. Primetown Property Group, Inc.Document11 paginiCommissioner of Internal Revenue vs. Primetown Property Group, Inc.Queenie SabladaÎncă nu există evaluări

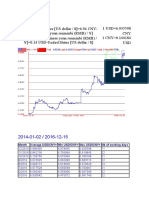

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDocument3 paginiMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyÎncă nu există evaluări

- Rhula Mozambique Weekly Media Review - 17 February To 24 February 2017Document90 paginiRhula Mozambique Weekly Media Review - 17 February To 24 February 2017davidbarskeÎncă nu există evaluări

- N 1415 Iso - CD - 3408-5 - (E) - 2003 - 08Document16 paginiN 1415 Iso - CD - 3408-5 - (E) - 2003 - 08brunoagandraÎncă nu există evaluări

- Etoro Aus Capital Pty LTD Product Disclosure Statement: Issue Date: 31 July 2018Document26 paginiEtoro Aus Capital Pty LTD Product Disclosure Statement: Issue Date: 31 July 2018robert barbersÎncă nu există evaluări

- Fees and ChecklistDocument3 paginiFees and ChecklistAdenuga SantosÎncă nu există evaluări

- 8 Trdln0610saudiDocument40 pagini8 Trdln0610saudiJad SoaiÎncă nu există evaluări

- In Re: Rnnkeepers Usa Trust. Debtors. - Chapter LL Case No. 10 13800 (SCC)Document126 paginiIn Re: Rnnkeepers Usa Trust. Debtors. - Chapter LL Case No. 10 13800 (SCC)Chapter 11 DocketsÎncă nu există evaluări

- Economic Development Complete NotesDocument36 paginiEconomic Development Complete Notessajad ahmadÎncă nu există evaluări

- Institutional Investor - 07 JUL 2009Document72 paginiInstitutional Investor - 07 JUL 2009jumanleeÎncă nu există evaluări

- Company Analysis - Applied Valuation by Rajat JhinganDocument13 paginiCompany Analysis - Applied Valuation by Rajat Jhinganrajat_marsÎncă nu există evaluări

- Hhse - JSJ Ozark Bank GarnishmentDocument38 paginiHhse - JSJ Ozark Bank GarnishmentYTOLeaderÎncă nu există evaluări

- Public Expenditure PFM handbook-WB-2008 PDFDocument354 paginiPublic Expenditure PFM handbook-WB-2008 PDFThơm TrùnÎncă nu există evaluări

- Od124222428139339000 4Document2 paginiOd124222428139339000 4biren shahÎncă nu există evaluări

- An Iot Based Dam Water Management System For AgricultureDocument21 paginiAn Iot Based Dam Water Management System For AgriculturemathewsÎncă nu există evaluări

- Latitudes Not AttitudesDocument7 paginiLatitudes Not Attitudesikonoclast13456Încă nu există evaluări