S-ar putea să vă placă și

- CTC Calculation SheetDocument1 paginăCTC Calculation SheetSathvika SaaraÎncă nu există evaluări

- FA Question Bank TT1-1Document14 paginiFA Question Bank TT1-1rock SINGHALÎncă nu există evaluări

- Soft OfferDocument3 paginiSoft OfferRicardo CagnoniÎncă nu există evaluări

- Real Estate AppraiserDocument2 paginiReal Estate Appraiserapi-77241843Încă nu există evaluări

- 4.02 Business Banking Check Parts (B) - 2Document7 pagini4.02 Business Banking Check Parts (B) - 2TrinityÎncă nu există evaluări

- Corporate Restructuring Short NotesDocument31 paginiCorporate Restructuring Short NotesSatwik Jain57% (7)

- Wholesale Juice Business PlanDocument26 paginiWholesale Juice Business PlanPatrick Cee AnekweÎncă nu există evaluări

- Cash Flow Estimation and Capital BudgetingDocument29 paginiCash Flow Estimation and Capital BudgetingShehroz Saleem QureshiÎncă nu există evaluări

- BBS 4th Year Final WorkDocument48 paginiBBS 4th Year Final WorkNamuna Joshi88% (8)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionDe la EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionÎncă nu există evaluări

- 98 2 Fin Homework Part 04Document6 pagini98 2 Fin Homework Part 04Yan Ho YeungÎncă nu există evaluări

- Class 11 Accounts SP 1Document6 paginiClass 11 Accounts SP 1UdyamGÎncă nu există evaluări

- Fe - Accountancy Xi Set ADocument6 paginiFe - Accountancy Xi Set AAntariksh SainiÎncă nu există evaluări

- Mid Term Accounts - SubjectiveDocument4 paginiMid Term Accounts - Subjectivekarishma prabagaranÎncă nu există evaluări

- Faculty of Commerce: Code No. 10001Document4 paginiFaculty of Commerce: Code No. 10001Madasu BalnarsimhaÎncă nu există evaluări

- Assigment BBM Finacial AccountingDocument6 paginiAssigment BBM Finacial Accountingtripathi_indramani5185Încă nu există evaluări

- Sutlej Public SR Sec School Annual Examination (Session 2021-22) Class Xi Commerce Subject: Accountancy TIME: 2 Hours MM 40Document4 paginiSutlej Public SR Sec School Annual Examination (Session 2021-22) Class Xi Commerce Subject: Accountancy TIME: 2 Hours MM 40mnmehta1990Încă nu există evaluări

- Revision Test FinalDocument4 paginiRevision Test FinalRitaÎncă nu există evaluări

- Good Shepherd International School, Ooty: Winter Holiday Homework 2018 - 19Document4 paginiGood Shepherd International School, Ooty: Winter Holiday Homework 2018 - 19Aaryaman ModiÎncă nu există evaluări

- Acc Xi Class Test-I 2022Document4 paginiAcc Xi Class Test-I 2022shaurya kapoorÎncă nu există evaluări

- Cbse Class 11 Accountancy Sample Paper Set 2 QuestionsDocument6 paginiCbse Class 11 Accountancy Sample Paper Set 2 QuestionsNishtha 3153Încă nu există evaluări

- 11 Accounts Final First Assessment 1Document4 pagini11 Accounts Final First Assessment 1khush marooÎncă nu există evaluări

- Question Bank For AccountsDocument12 paginiQuestion Bank For AccountsSwati DubeyÎncă nu există evaluări

- AtibhaDocument7 paginiAtibhaAangry VermaÎncă nu există evaluări

- PAC All CAF Subjects Mocks With Solutions Regards Saboor AhmadDocument164 paginiPAC All CAF Subjects Mocks With Solutions Regards Saboor AhmadTajammal CheemaÎncă nu există evaluări

- Delhi Pubic School, Nacharam Accountancy - Xi Question BankDocument9 paginiDelhi Pubic School, Nacharam Accountancy - Xi Question BanklasyaÎncă nu există evaluări

- Blossems Convent School CLASS: 11 Commerce Group Subject: Accoutancy Holidays AssignmentDocument3 paginiBlossems Convent School CLASS: 11 Commerce Group Subject: Accoutancy Holidays AssignmentPawanpreet KaurÎncă nu există evaluări

- Sample Paper Xi Acc 2022 23Document7 paginiSample Paper Xi Acc 2022 23rehankatyal05Încă nu există evaluări

- Class 11 Accounts Half Yearly SPDocument9 paginiClass 11 Accounts Half Yearly SPRakesh AgarwalÎncă nu există evaluări

- AFM Question Bank-Unit 2: Book KeepingDocument3 paginiAFM Question Bank-Unit 2: Book KeepingSachin D SalankeyÎncă nu există evaluări

- Test Paper Ca FoundDocument5 paginiTest Paper Ca FoundSarangapani KaliyamoorthyÎncă nu există evaluări

- Class 11 AccountsDocument3 paginiClass 11 Accountssamarthj.9390Încă nu există evaluări

- Class Xi Acc QPDocument7 paginiClass Xi Acc QP8201ayushÎncă nu există evaluări

- Test 4Document6 paginiTest 4Jayant MittalÎncă nu există evaluări

- 5664accountancy XIDocument9 pagini5664accountancy XIAryan VishwakarmaÎncă nu există evaluări

- Karnataka Ist PUC Accountcancy Sample Question Paper 4 PDFDocument4 paginiKarnataka Ist PUC Accountcancy Sample Question Paper 4 PDFNeha BaligaÎncă nu există evaluări

- Xi Accountancy 80 Marks General InstructionsDocument5 paginiXi Accountancy 80 Marks General InstructionsJash ShahÎncă nu există evaluări

- Sample Paper-2016 Subject: Class 11: Part - A (Financial Accounting - I)Document4 paginiSample Paper-2016 Subject: Class 11: Part - A (Financial Accounting - I)Šhûbh Šhôûřyâ KâšhyâpÎncă nu există evaluări

- Class XI Acc SM Arya Annual 2023-24Document5 paginiClass XI Acc SM Arya Annual 2023-24pandeyansh962Încă nu există evaluări

- Model Paper, Accountancy, XIDocument13 paginiModel Paper, Accountancy, XIanyaÎncă nu există evaluări

- शिक्षा निदेिालय राष्ट्रीय राजधािी क्षेत्र ददल्ली Directorate of Education, GNCT of DelhiDocument4 paginiशिक्षा निदेिालय राष्ट्रीय राजधािी क्षेत्र ददल्ली Directorate of Education, GNCT of DelhiAshish ChÎncă nu există evaluări

- XI-com PPR 21-1-23Document2 paginiXI-com PPR 21-1-23Obaid KhanÎncă nu există evaluări

- Nava Bharath National School Annur Annual Examination - 2021 AccountancyDocument5 paginiNava Bharath National School Annur Annual Examination - 2021 AccountancypranavÎncă nu există evaluări

- Class 11 Accountancy Worksheet - 2023-24Document17 paginiClass 11 Accountancy Worksheet - 2023-24Yashi BhawsarÎncă nu există evaluări

- Section "B" (Short-Answer Questions) (30 Marks) : Government Boys Degree College (M) Gulistan-E-Johar, KarachiDocument4 paginiSection "B" (Short-Answer Questions) (30 Marks) : Government Boys Degree College (M) Gulistan-E-Johar, KarachiArshad KhanÎncă nu există evaluări

- 11 Accountancy SP 2Document17 pagini11 Accountancy SP 2Vikas Chandra BalodhiÎncă nu există evaluări

- Nov - 19 - Question and AnswersDocument15 paginiNov - 19 - Question and AnswersVidhi AgrawalÎncă nu există evaluări

- CA Foundation MTP 2020 Paper 1 QuesDocument6 paginiCA Foundation MTP 2020 Paper 1 QuesSaurabh Kumar MauryaÎncă nu există evaluări

- © The Institute of Chartered Accountants of India: TH ST THDocument15 pagini© The Institute of Chartered Accountants of India: TH ST THGaurav KumarÎncă nu există evaluări

- Show Your Working Clearly.: AccountancyDocument8 paginiShow Your Working Clearly.: AccountancyYash SardaÎncă nu există evaluări

- Session Ending Examination 2019Document7 paginiSession Ending Examination 2019madhudevi06435Încă nu există evaluări

- Question 1Document3 paginiQuestion 1Mohammad Tariq AnsariÎncă nu există evaluări

- Acc Full Test 3Document6 paginiAcc Full Test 3Periyanan VÎncă nu există evaluări

- LHU8Q Olopr DaisyAcountXIDocument35 paginiLHU8Q Olopr DaisyAcountXIDido MuczÎncă nu există evaluări

- Sample Paper For Class 11 Accountancy Set 1 QuestionsDocument6 paginiSample Paper For Class 11 Accountancy Set 1 Questionsrenu bhattÎncă nu există evaluări

- Accountancy: General InstructionsDocument5 paginiAccountancy: General InstructionsSwami NarangÎncă nu există evaluări

- UT 1 AccountsDocument4 paginiUT 1 Accountskarishma prabagaranÎncă nu există evaluări

- 11 AccDocument6 pagini11 AccPushpinder KumarÎncă nu există evaluări

- Question Bank BKDocument8 paginiQuestion Bank BKVivek JaiswarÎncă nu există evaluări

- 11 Sample Papers Accountancy 2020 English Medium Set 1 PDFDocument13 pagini11 Sample Papers Accountancy 2020 English Medium Set 1 PDFpriyaÎncă nu există evaluări

- Bcoc 131Document5 paginiBcoc 131Anamika T AnilÎncă nu există evaluări

- Questions Bank Accounts ClassDocument5 paginiQuestions Bank Accounts ClassRidhesh SharmaÎncă nu există evaluări

- 650d55c860e827001812a329 - ## - Accountancy Master Test - 2 - Questions - 650d55c860e827001812a329Document4 pagini650d55c860e827001812a329 - ## - Accountancy Master Test - 2 - Questions - 650d55c860e827001812a329sushil262004Încă nu există evaluări

- BPS Class XI Pre Board Examination Question Papers Jan 2015 All Subjects Scce CommerceDocument53 paginiBPS Class XI Pre Board Examination Question Papers Jan 2015 All Subjects Scce CommercelembdaÎncă nu există evaluări

- Part - A (: Time Allowed: 3 Hours Maximum Marks: 90Document4 paginiPart - A (: Time Allowed: 3 Hours Maximum Marks: 90NameÎncă nu există evaluări

- Accountancy XI Half Yearly WorksheetDocument8 paginiAccountancy XI Half Yearly WorksheetDeivanai K CSÎncă nu există evaluări

- 4 MarksDocument4 pagini4 MarksEswari GkÎncă nu există evaluări

- Bài TTDocument3 paginiBài TTPhạm Như HuỳnhÎncă nu există evaluări

- 2015 Pru Life UK Annual Report PDFDocument61 pagini2015 Pru Life UK Annual Report PDFMichael S LeysonÎncă nu există evaluări

- Company ProfileDocument15 paginiCompany ProfileAslam HossainÎncă nu există evaluări

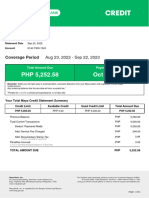

- MayaCredit SoA 2023SEPDocument3 paginiMayaCredit SoA 2023SEPjepoy palaruanÎncă nu există evaluări

- Philippine National Construction Corporation Executive Summary 2019Document5 paginiPhilippine National Construction Corporation Executive Summary 2019reslazaroÎncă nu există evaluări

- Income Tax and VATDocument498 paginiIncome Tax and VATshankar k.c.100% (2)

- Compare Savings Accounts & ISAs NationwideDocument1 paginăCompare Savings Accounts & ISAs NationwideVivienneÎncă nu există evaluări

- Class TestDocument6 paginiClass TestMayank kaushikÎncă nu există evaluări

- Investment Arbitration and Country Risk 1711783556Document28 paginiInvestment Arbitration and Country Risk 17117835568nqcpq9tq9Încă nu există evaluări

- Responsibility Accounting LNDocument7 paginiResponsibility Accounting LNzein lopezÎncă nu există evaluări

- AR 2009 EngDocument252 paginiAR 2009 EngmorgunovaÎncă nu există evaluări

- Nova Chemical CorporationDocument28 paginiNova Chemical Corporationrzannat94100% (2)

- 12 Asian Cathay Finance V Sps Gravador and de VeraDocument9 pagini12 Asian Cathay Finance V Sps Gravador and de VeraAnne VallaritÎncă nu există evaluări

- Finmar - Chapter 12 - 14Document24 paginiFinmar - Chapter 12 - 14AlexanÎncă nu există evaluări

- Central Bank: The Guardian of CurrencyDocument6 paginiCentral Bank: The Guardian of CurrencyBe YourselfÎncă nu există evaluări

- Nike CaseDocument10 paginiNike CaseDanielle Saavedra0% (1)

- MAA716 - T2 - 2012 v2Document11 paginiMAA716 - T2 - 2012 v2ssusasi4769Încă nu există evaluări

- 7Document31 pagini7Chinzorig Tsevegjav100% (1)

- How To Secure BIR Importer Clearance CertificateDocument6 paginiHow To Secure BIR Importer Clearance CertificateEmely SolonÎncă nu există evaluări

- Revenue Memorandum Circular No. 09-06: January 25, 2006Document5 paginiRevenue Memorandum Circular No. 09-06: January 25, 2006dom0202Încă nu există evaluări

- Andres Pou: Miami - Dade Community CollegeDocument2 paginiAndres Pou: Miami - Dade Community CollegeChandra SimsÎncă nu există evaluări