S-ar putea să vă placă și

- NOTESDocument8 paginiNOTESShruthi sÎncă nu există evaluări

- What Is FortfaitingDocument3 paginiWhat Is FortfaitingRAMESHBABUÎncă nu există evaluări

- The Concept of Forfeiting in Export Finance: You Are HereDocument3 paginiThe Concept of Forfeiting in Export Finance: You Are HereAmit AgrawalÎncă nu există evaluări

- ForfeitingDocument18 paginiForfeitingvandana_daki3941Încă nu există evaluări

- ForfaitingDocument14 paginiForfaitingArun SharmaÎncă nu există evaluări

- Factoring & ForfaitingDocument2 paginiFactoring & ForfaitingYashÎncă nu există evaluări

- L9 Project Financing AlternativesDocument54 paginiL9 Project Financing AlternativesNilesh MandlikÎncă nu există evaluări

- Factoring and ForfaitingDocument3 paginiFactoring and ForfaitingSushant RathiÎncă nu există evaluări

- Forfeiting vs Factoring: Key Differences in International Trade ReceivablesDocument3 paginiForfeiting vs Factoring: Key Differences in International Trade ReceivablesjosetonyeduthanÎncă nu există evaluări

- Trade 4Document5 paginiTrade 4krissh_87Încă nu există evaluări

- Chapter - 1: MeaningDocument84 paginiChapter - 1: MeaningManoj KumarÎncă nu există evaluări

- Trade Finance GuideDocument2 paginiTrade Finance GuideMBASTUDENTPUPÎncă nu există evaluări

- Factoring and Forfaiting ExplainedDocument30 paginiFactoring and Forfaiting ExplainedSuman AcharyaÎncă nu există evaluări

- Factoring Vs ForfeitingDocument27 paginiFactoring Vs ForfeitingShruti AshokÎncă nu există evaluări

- Case StudyDocument4 paginiCase Studyakshita ramdas100% (1)

- What Is A Letter of Credit?Document29 paginiWhat Is A Letter of Credit?Varun DagaÎncă nu există evaluări

- International Finance: Financing of International TradeDocument4 paginiInternational Finance: Financing of International TradeEkta GuptaÎncă nu există evaluări

- Export Finance-Countertrade and ForfaitingDocument26 paginiExport Finance-Countertrade and ForfaitingRajat LoyaÎncă nu există evaluări

- Finance Is That Branch of Economics That Deals With Management of Money and Assets InvolvingDocument12 paginiFinance Is That Branch of Economics That Deals With Management of Money and Assets InvolvingKomal ParikhÎncă nu există evaluări

- Export Credit and Financing in International TradeDocument22 paginiExport Credit and Financing in International Tradepromptpaper1Încă nu există evaluări

- II. Trade Finance Methods and Instruments: An Overview: A. IntroductionDocument11 paginiII. Trade Finance Methods and Instruments: An Overview: A. IntroductionSandeep SinghÎncă nu există evaluări

- International Trade Logistics Project: Made By: Group 9Document7 paginiInternational Trade Logistics Project: Made By: Group 9Prathamesh Rajaykumar DahakeÎncă nu există evaluări

- Guide To For Fa It IngDocument21 paginiGuide To For Fa It IngcristiansaitariuÎncă nu există evaluări

- Legal EnvironmentDocument12 paginiLegal EnvironmentJasleen ChawlaÎncă nu există evaluări

- Export & Import Financing: UnderstandDocument26 paginiExport & Import Financing: UnderstandNeeta SharmaÎncă nu există evaluări

- AniketDocument5 paginiAniketAjay PrajapatiÎncă nu există evaluări

- CH 18Document9 paginiCH 18MBASTUDENTPUPÎncă nu există evaluări

- Bank Guarantee Types and UsesDocument12 paginiBank Guarantee Types and UsesmydeanzÎncă nu există evaluări

- Factoring, Forfaiting & Bills DiscountingDocument3 paginiFactoring, Forfaiting & Bills DiscountingkrishnadaskotaÎncă nu există evaluări

- Assignment 1 Medium and Long Term FinancingDocument12 paginiAssignment 1 Medium and Long Term FinancingMohit SahajpalÎncă nu există evaluări

- Types of Mutual FundDocument5 paginiTypes of Mutual FundGourav BulandiÎncă nu există evaluări

- Export FinanceDocument8 paginiExport FinanceMushiur RahmanÎncă nu există evaluări

- FactoringDocument2 paginiFactoringsandeepborseÎncă nu există evaluări

- Commercial Banks: Financial Institution United Kingdom Investment Bank Federal Deposit Insurance CorporationDocument9 paginiCommercial Banks: Financial Institution United Kingdom Investment Bank Federal Deposit Insurance CorporationsyarifÎncă nu există evaluări

- LC Basics: Intro to Letters of CreditDocument4 paginiLC Basics: Intro to Letters of CreditNahid Ali Mosleh JituÎncă nu există evaluări

- Assignment OF M.F.I.S: Topic: Financial ServicesDocument11 paginiAssignment OF M.F.I.S: Topic: Financial ServicesmeghukhandelwalÎncă nu există evaluări

- Foreign Exchange Operations in Commercial BanksDocument16 paginiForeign Exchange Operations in Commercial BanksTara Gilani67% (3)

- Latter of Credit and Other FinaciDocument57 paginiLatter of Credit and Other FinaciHaresh RajputÎncă nu există evaluări

- Objectives of Receivables Management: Standards, Length of Credit Period, Cash Discount, Discount Period EtcDocument8 paginiObjectives of Receivables Management: Standards, Length of Credit Period, Cash Discount, Discount Period EtcRekha SoniÎncă nu există evaluări

- Factoring May Be Recourse or Non-RecourseDocument2 paginiFactoring May Be Recourse or Non-Recourseamar dihingiaÎncă nu există evaluări

- C3 Management of Foreign Accounts ReceivableDocument3 paginiC3 Management of Foreign Accounts ReceivableTENGKU ANIS TENGKU YUSMAÎncă nu există evaluări

- Factoring 1Document21 paginiFactoring 1Sudhir GijareÎncă nu există evaluări

- DerivativesDocument12 paginiDerivativesVenn Bacus RabadonÎncă nu există evaluări

- FactoringDocument32 paginiFactoringkalyaniduttaÎncă nu există evaluări

- A Guide To Receivables FinanceDocument7 paginiA Guide To Receivables FinancekevindsizaÎncă nu există evaluări

- Guide to International Finance ConceptsDocument11 paginiGuide to International Finance ConceptsShruti ReddyÎncă nu există evaluări

- Pge69 72Document6 paginiPge69 72Xuân Nhi LêÎncă nu există evaluări

- Topic:-Factoring Vs Forfaiting: Dr. Dileep Kumar SinghDocument20 paginiTopic:-Factoring Vs Forfaiting: Dr. Dileep Kumar SinghDileep SinghÎncă nu există evaluări

- Purpose of FinanceDocument10 paginiPurpose of FinanceManjith BoloorÎncă nu există evaluări

- Post ShipmentDocument3 paginiPost ShipmentBhanu MehraÎncă nu există evaluări

- CBM AssignmentDocument6 paginiCBM AssignmentNimit BhatiaÎncă nu există evaluări

- International Payment Methods and RisksDocument20 paginiInternational Payment Methods and Risksmatthew kobulnickÎncă nu există evaluări

- Unit 3 IelDocument10 paginiUnit 3 Ielrssharma3245Încă nu există evaluări

- Trade FinanceDocument31 paginiTrade Financesadafsharique100% (1)

- Financing of Foreign TradeDocument35 paginiFinancing of Foreign TradeRohith AnanthÎncă nu există evaluări

- Trade Finance: International Chamber of CommerceDocument7 paginiTrade Finance: International Chamber of Commerceosama aboualamÎncă nu există evaluări

- Group 2 - Forfaiting & Factoring-MBA (IB) - 2018-21Document12 paginiGroup 2 - Forfaiting & Factoring-MBA (IB) - 2018-21Kaushik HazarikaÎncă nu există evaluări

- Explaining the 3 Main Financing Options of an Export OrderDocument8 paginiExplaining the 3 Main Financing Options of an Export OrderDiana SumailiÎncă nu există evaluări

- Fixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2De la EverandFixed Income Securities: A Beginner's Guide to Understand, Invest and Evaluate Fixed Income Securities: Investment series, #2Încă nu există evaluări

- Comparative Study of BSNL and AritelDocument15 paginiComparative Study of BSNL and AriteldiviprabhuÎncă nu există evaluări

- PresentationDocument2 paginiPresentationdiviprabhuÎncă nu există evaluări

- C&B Mod IDocument32 paginiC&B Mod IdiviprabhuÎncă nu există evaluări

- Customer Satisfaction towards Honda Two Wheelers in TirupatiDocument10 paginiCustomer Satisfaction towards Honda Two Wheelers in TirupatiHussam MubashirÎncă nu există evaluări

- Bio Data Form - NewDocument2 paginiBio Data Form - NewBasil Baby-PisharathuÎncă nu există evaluări

- Consumers Behaviour TowardsDocument9 paginiConsumers Behaviour TowardsBilal RajaÎncă nu există evaluări

- PresentationDocument2 paginiPresentationdiviprabhuÎncă nu există evaluări

- Resume Samples PDFDocument13 paginiResume Samples PDFRanjeet Gupta100% (1)

- Intro HondaDocument3 paginiIntro HondadiviprabhuÎncă nu există evaluări

- Speech Van DamDocument3 paginiSpeech Van DamdiviprabhuÎncă nu există evaluări

- IJXCD1210 - A Book Review On The Future of IndiaDocument5 paginiIJXCD1210 - A Book Review On The Future of IndiadiviprabhuÎncă nu există evaluări

- Drishti 2015 Thank You NoteDocument1 paginăDrishti 2015 Thank You NotediviprabhuÎncă nu există evaluări

- BfsDocument3 paginiBfsdiviprabhuÎncă nu există evaluări

- Important Instructions To StudentsDocument2 paginiImportant Instructions To StudentsAmber NicholsÎncă nu există evaluări

- TRM ModIDocument16 paginiTRM ModIdiviprabhuÎncă nu există evaluări

- TRMMod IVDocument15 paginiTRMMod IVdiviprabhuÎncă nu există evaluări

- TreasuryDocument69 paginiTreasurydiviprabhuÎncă nu există evaluări

- Tax Management-Module 1 Problems On Residential Status and Incidence On TaxDocument2 paginiTax Management-Module 1 Problems On Residential Status and Incidence On TaxdiviprabhuÎncă nu există evaluări

- Financial Statement AnalysisDocument36 paginiFinancial Statement AnalysisRonak H PatelÎncă nu există evaluări

- Non-Circumvention, Non-Disclosure & Working Agreement: Commodity - Quantity Price: $Document19 paginiNon-Circumvention, Non-Disclosure & Working Agreement: Commodity - Quantity Price: $Camilo ManriqueÎncă nu există evaluări

- Business Finance Week 2Document18 paginiBusiness Finance Week 2Milo CuaÎncă nu există evaluări

- SRS Document of Flipkart: IntroductionDocument33 paginiSRS Document of Flipkart: IntroductionSaurabh SinghÎncă nu există evaluări

- Sample Business StatementDocument4 paginiSample Business StatementLy Hoang100% (3)

- Books of Prime EntryDocument14 paginiBooks of Prime EntryBareera WajidÎncă nu există evaluări

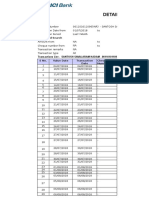

- OpTransactionHistory19 06 2019Document18 paginiOpTransactionHistory19 06 2019Poonam KapadiaÎncă nu există evaluări

- Chapter 7 - Test BankDocument94 paginiChapter 7 - Test Bankbekbek12100% (2)

- 10business Module4 AccountingDocument117 pagini10business Module4 Accountingchris100% (1)

- Banking, Inflation and Exchange Rates Notes and QuestionsDocument22 paginiBanking, Inflation and Exchange Rates Notes and QuestionsKelvinÎncă nu există evaluări

- HDFC Bank Project Nitin Kale PDFDocument62 paginiHDFC Bank Project Nitin Kale PDFMangesh Dasare100% (1)

- Chapter 7 Jan.22Document56 paginiChapter 7 Jan.22AaaÎncă nu există evaluări

- Nat WestDocument1 paginăNat WestЮлия П0% (1)

- Citibank Credit CardDocument6 paginiCitibank Credit CardgjvoraÎncă nu există evaluări

- Cat Solved Question Paper With Answer Key Varc Dilr QuantDocument21 paginiCat Solved Question Paper With Answer Key Varc Dilr QuantshailajaparkorcatÎncă nu există evaluări

- Wells Fargo Simple Business Checking: Important Account InformationDocument15 paginiWells Fargo Simple Business Checking: Important Account Informationsenia HidalgoÎncă nu există evaluări

- CreditDocument62 paginiCreditapi-262728967Încă nu există evaluări

- Banking Products and Operations - Unit 4Document57 paginiBanking Products and Operations - Unit 4Vaidyanathan RavichandranÎncă nu există evaluări

- Eye On China, Modi-Abe Summit Planned in Oct?: PLA Troops Non-Committal About RetreatDocument8 paginiEye On China, Modi-Abe Summit Planned in Oct?: PLA Troops Non-Committal About RetreatGauravÎncă nu există evaluări

- VISA Classic: Getting Yourself StartedDocument3 paginiVISA Classic: Getting Yourself Startedkarely jackson lopez100% (1)

- SWIFT FIN Payment Format Guide For European AcctsDocument19 paginiSWIFT FIN Payment Format Guide For European AcctsdestinysandeepÎncă nu există evaluări

- About Oriental Bank of CommerceDocument10 paginiAbout Oriental Bank of CommerceMandeep BatraÎncă nu există evaluări

- Official Notification - PGCIL RecruitmentDocument10 paginiOfficial Notification - PGCIL RecruitmentSupriya SantreÎncă nu există evaluări

- Government of Andhra Pradesh: Vijayawada Municipal CorporaitonDocument6 paginiGovernment of Andhra Pradesh: Vijayawada Municipal CorporaitonSrinivas SiripurapuÎncă nu există evaluări

- Improving Agribank's International Debit Card ServicesDocument32 paginiImproving Agribank's International Debit Card ServicesLe duc NghiaÎncă nu există evaluări

- Charges for Roaming Current Account at ICICI BankDocument3 paginiCharges for Roaming Current Account at ICICI Bankashishtiwari92100% (1)

- Classification 2Document24 paginiClassification 2Shaun WilsonÎncă nu există evaluări

- Indzara Personal Finance Manager 2010 v2Document8 paginiIndzara Personal Finance Manager 2010 v2AlexandruDanielÎncă nu există evaluări

- Ref - No. 11532934-16309213-3: Pintukumar Rameshbhai PatelDocument4 paginiRef - No. 11532934-16309213-3: Pintukumar Rameshbhai Patelpintukumar rameshbhaiÎncă nu există evaluări

- 2003 Annual Report Freddie MacDocument261 pagini2003 Annual Report Freddie Macnakoda121Încă nu există evaluări