S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Meezan Bank Statement-UnlockedDocument3 paginiMeezan Bank Statement-UnlockedMUHAMMAD USMAN IQBAL100% (3)

- PDFDocument33 paginiPDFSriram KrishnanÎncă nu există evaluări

- Account Statement From 01-11-2021 To 23-12-2021Document5 paginiAccount Statement From 01-11-2021 To 23-12-2021ANIL MANDIÎncă nu există evaluări

- Final Exam in Tax 2Document5 paginiFinal Exam in Tax 2elminvaldezÎncă nu există evaluări

- Calamba Steel Center v. CIR - DigestDocument2 paginiCalamba Steel Center v. CIR - Digestcmv mendozaÎncă nu există evaluări

- Annuity Calculator: Withdrawal PlanDocument2 paginiAnnuity Calculator: Withdrawal PlanThanga PandiÎncă nu există evaluări

- SBI Fee & ChargesDocument16 paginiSBI Fee & ChargesAks SomvanshiÎncă nu există evaluări

- Basic Documents and Transactions Related To Bank Deposits: Prepared By: Ray Allen H. Silva, CPADocument18 paginiBasic Documents and Transactions Related To Bank Deposits: Prepared By: Ray Allen H. Silva, CPAmhl scrnnnÎncă nu există evaluări

- My StatementDocument1 paginăMy StatementmayankÎncă nu există evaluări

- Direct Deposit and ACH Payment Enrollment Form 2-2-22Document2 paginiDirect Deposit and ACH Payment Enrollment Form 2-2-22ganesh pathakÎncă nu există evaluări

- Data PDFDocument1 paginăData PDFRaj SaumyaÎncă nu există evaluări

- Tax On Salary: Income Tax Law & CalculationDocument7 paginiTax On Salary: Income Tax Law & CalculationSyed Aijlal JillaniÎncă nu există evaluări

- Smart 2306Document2 paginiSmart 2306Billing ZamboecozoneÎncă nu există evaluări

- Cap & Gown OrderDocument2 paginiCap & Gown OrderΝίκος Μυρογιάννης-ΚούκοςÎncă nu există evaluări

- Module 4 .1 - Schedule of Withholding TaxesDocument2 paginiModule 4 .1 - Schedule of Withholding Taxeskrisha milloÎncă nu există evaluări

- PR 7 Diagnostic ExamDocument8 paginiPR 7 Diagnostic ExamMendoza Ron NixonÎncă nu există evaluări

- Qantas Airways: Name: Institution Affiliation: DateDocument8 paginiQantas Airways: Name: Institution Affiliation: DatePhuong NhungÎncă nu există evaluări

- Mobile Payments How To GuideDocument1 paginăMobile Payments How To GuideDan BarronÎncă nu există evaluări

- Oluwale AdebayoDocument1 paginăOluwale Adebayowhitneydemetria007Încă nu există evaluări

- Excel SMS2 (Pt. Cemerlang)Document14 paginiExcel SMS2 (Pt. Cemerlang)Zahratul WardiyahÎncă nu există evaluări

- Mindanao I Geothermal Partnership vs. Commissioner of Internal Revenue, 844 SCRA 386, November 08, 2017Document12 paginiMindanao I Geothermal Partnership vs. Commissioner of Internal Revenue, 844 SCRA 386, November 08, 2017Vida MarieÎncă nu există evaluări

- July 2021 STRFDocument11 paginiJuly 2021 STRFYae'kult VIpincepe QuilabÎncă nu există evaluări

- Taxation Review Final Income TaxDocument4 paginiTaxation Review Final Income TaxGendyBocoÎncă nu există evaluări

- Tender Review and Documents ChecklistDocument2 paginiTender Review and Documents ChecklistsugamsehgalÎncă nu există evaluări

- StatementOfAccount 6354576294 02012024 172901Document5 paginiStatementOfAccount 6354576294 02012024 172901sugumarÎncă nu există evaluări

- Computation 2022 23Document3 paginiComputation 2022 23saumyabisht143Încă nu există evaluări

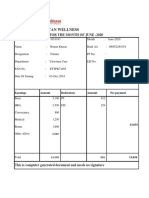

- Hindustan Wellness: Pay Slip For The Month of June - 2020Document3 paginiHindustan Wellness: Pay Slip For The Month of June - 2020ManishÎncă nu există evaluări

- Accommodation at Vivekananda Kendra Kanyakumari - Vivekananda Kendra HyderabadDocument7 paginiAccommodation at Vivekananda Kendra Kanyakumari - Vivekananda Kendra HyderabadPrabhat JainÎncă nu există evaluări

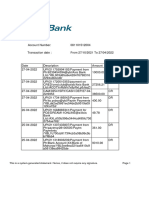

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureDocument27 paginiThis Is A System-Generated Statement. Hence, It Does Not Require Any SignaturemohitchakarnagarÎncă nu există evaluări

- GST Rahul 1 Project WorkDocument29 paginiGST Rahul 1 Project WorkRohan 70KÎncă nu există evaluări