S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- 1st Freshmen Tutorial Activity 1Document2 pagini1st Freshmen Tutorial Activity 1Stephanie Diane SabadoÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- Replacement Activity For Grace Company (Master Budget Preparation)Document5 paginiReplacement Activity For Grace Company (Master Budget Preparation)Stephanie Diane SabadoÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- 1st Freshmen Tutorial Activity 2Document3 pagini1st Freshmen Tutorial Activity 2Stephanie Diane SabadoÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Manual Payroll System: Production Cost AccountingDocument17 paginiManual Payroll System: Production Cost AccountingStephanie Diane SabadoÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Manual Purchase System: Vendor Purchasing Department Inentory Control ReceivingDocument14 paginiManual Purchase System: Vendor Purchasing Department Inentory Control ReceivingStephanie Diane SabadoÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

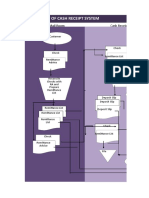

- Flowchart of Cash Receipt System: Mail Room Cash ReceiptsDocument17 paginiFlowchart of Cash Receipt System: Mail Room Cash ReceiptsStephanie Diane SabadoÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Packing Slip: Manual P System Vendor Purchasing DepartmentDocument20 paginiPacking Slip: Manual P System Vendor Purchasing DepartmentStephanie Diane SabadoÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Lumad GroupsDocument11 paginiLumad GroupsStephanie Diane Sabado100% (2)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Packing Slip: Manual P System Vendor Purchasing DepartmentDocument20 paginiPacking Slip: Manual P System Vendor Purchasing DepartmentStephanie Diane SabadoÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Act1 Cash ReceiptsDocument17 paginiAct1 Cash ReceiptsStephanie Diane SabadoÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Global Semi Trailer Sales Market Report 2017Document3 paginiGlobal Semi Trailer Sales Market Report 2017Shaun Martin0% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Lovepop Report PDFDocument15 paginiLovepop Report PDFShivam Bose50% (2)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- CBM RatioDocument9 paginiCBM RatioImran HossainÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Benefits of Planning in ManagementDocument7 paginiBenefits of Planning in ManagementMoazzam ZiaÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Chapter 6Document18 paginiChapter 6marieieiemÎncă nu există evaluări

- PT JayatamaDocument24 paginiPT Jayatamaputri apriliaÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Bain Interactive Interview Briefing PackDocument19 paginiBain Interactive Interview Briefing PackDavid MiguelÎncă nu există evaluări

- C03 Practise Questions - Basic Mathematics - C03 Fundamentals of Business MathematicsDocument7 paginiC03 Practise Questions - Basic Mathematics - C03 Fundamentals of Business MathematicsEshan FernandoÎncă nu există evaluări

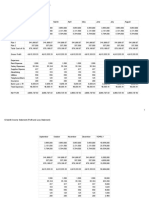

- 12-Month Income Statement Profit-And-Loss Statement - Sheet1Document2 pagini12-Month Income Statement Profit-And-Loss Statement - Sheet1api-462952636100% (1)

- Mumbai Kamgar M.G.S.S.Maryadit CKS: Apna Bazar Co-Op Department Store (Mulund)Document20 paginiMumbai Kamgar M.G.S.S.Maryadit CKS: Apna Bazar Co-Op Department Store (Mulund)Gaurav SavlaniÎncă nu există evaluări

- Plantmatic (An Entrepreneur Ship Project)Document23 paginiPlantmatic (An Entrepreneur Ship Project)Muhammed GhazanfarÎncă nu există evaluări

- Bcoe 143Document9 paginiBcoe 143Yashita KansalÎncă nu există evaluări

- Sacramento State NCAA 2020Document80 paginiSacramento State NCAA 2020Matt BrownÎncă nu există evaluări

- Chapter 7 Aa 1 SolDocument18 paginiChapter 7 Aa 1 SolStephanie SundiangÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Soal Latihan Excel Solver Dan LindoDocument3 paginiSoal Latihan Excel Solver Dan LindoSuryaAdhiSaputra100% (1)

- BAb 6 Warren AKUNTANSI UNTUK PERUSAHAAN DAGANGDocument76 paginiBAb 6 Warren AKUNTANSI UNTUK PERUSAHAAN DAGANGbambangÎncă nu există evaluări

- Accounting - Self Study Guide For Staff of Micro Finance InstitutionsDocument9 paginiAccounting - Self Study Guide For Staff of Micro Finance Institutionsஆக்ஞா கிருஷ்ணா ஷர்மாÎncă nu există evaluări

- Signify Annual Report 2018 PDFDocument182 paginiSignify Annual Report 2018 PDFAman AgarwalÎncă nu există evaluări

- Test Bank SCFDocument114 paginiTest Bank SCFAnnabelle RafolsÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Case 06 Financial Detective 2016 F1763XDocument6 paginiCase 06 Financial Detective 2016 F1763XJosie KomiÎncă nu există evaluări

- Internal Revenue Vs TMXDocument2 paginiInternal Revenue Vs TMXmarwinjsÎncă nu există evaluări

- Thrift Store Business Plan ExampleDocument33 paginiThrift Store Business Plan ExampleKim So-Hyun0% (2)

- Lead Tracking TemplateDocument12 paginiLead Tracking TemplatevenkateshsjÎncă nu există evaluări

- ASNPO at A Glance BDODocument21 paginiASNPO at A Glance BDORemi AboÎncă nu există evaluări

- Shoaib StatementDocument88 paginiShoaib StatementshaikhÎncă nu există evaluări

- 2017 SPS Elmer and Nelly Dela Cruz BookkeeppingDocument39 pagini2017 SPS Elmer and Nelly Dela Cruz BookkeeppingLester Jao SegubanÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Alibaba IPO Financial ModelDocument54 paginiAlibaba IPO Financial ModelPRIYANKA KÎncă nu există evaluări

- Cost12 Study03 PDFDocument12 paginiCost12 Study03 PDFVINCENT GAYRAMON100% (1)

- Caf 06 Principles of Taxation QBDocument115 paginiCaf 06 Principles of Taxation QBSajid Ali100% (2)

- Fabm 2-6Document39 paginiFabm 2-6Janine Balcueva82% (11)