S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Chapter 1 PFPDocument23 paginiChapter 1 PFPHarD's PaaTtelÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- CIRP RegulationsDocument100 paginiCIRP Regulationssoumikighosh10Încă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

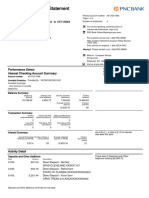

- PNC Checking Acc Statement (2)Document2 paginiPNC Checking Acc Statement (2)HermanÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- Chp8 3edition PDFDocument21 paginiChp8 3edition PDFAbarajithan RajendranÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Compound Interest ProblemsDocument16 paginiCompound Interest Problemsgnim12051Încă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Subprime - PrimerDocument14 paginiSubprime - PrimerShailendraÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- All Accounts Balance Details: S. No. Account Number Account Type Branch Rate of Interest (% P.a.) BalanceDocument2 paginiAll Accounts Balance Details: S. No. Account Number Account Type Branch Rate of Interest (% P.a.) Balanceshashwatsagar1729Încă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- YLlq 6 QSGFGF 0 Uyz 8Document2 paginiYLlq 6 QSGFGF 0 Uyz 8Praveen SainiÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Aie Credit WebquestDocument2 paginiAie Credit Webquestapi-267815068Încă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- Buy Your First HouseDocument13 paginiBuy Your First HouseAlonzo AventsÎncă nu există evaluări

- Kotak Lifetime Income V13Document11 paginiKotak Lifetime Income V13skverma3108Încă nu există evaluări

- Barican vs. IacDocument2 paginiBarican vs. IacKaryl Ann Aquino-CaluyaÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Business finance essentialsDocument17 paginiBusiness finance essentialsMark DavidÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Invoice INV-2291Document1 paginăInvoice INV-2291Trung ThaiÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- СHASE 20181218-statements-7322Document6 paginiСHASE 20181218-statements-7322Myt WovenÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Cooperative AssignmentDocument2 paginiCooperative AssignmentWhite WhiteyÎncă nu există evaluări

- Calculate BP2BT mortgage assistance and loan detailsDocument6 paginiCalculate BP2BT mortgage assistance and loan detailsCahya SujatmikoÎncă nu există evaluări

- BankCodeExposed 2Document624 paginiBankCodeExposed 2Property Wave100% (6)

- Section 609 of The Fair Credit Reporting Act LoopholeDocument7 paginiSection 609 of The Fair Credit Reporting Act LoopholeFreedomofMind97% (39)

- Part 01 - CH 03-Computing The TaxDocument51 paginiPart 01 - CH 03-Computing The TaxwdlzfrzÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- HW FIN201-Chapter9-Vong BophaDocument2 paginiHW FIN201-Chapter9-Vong BophaBopha vongÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Different Types of Loan Products Offered by Private Commercial Banks in Bangladesh - A Case Study On Modhumoti Bank LimitedDocument16 paginiDifferent Types of Loan Products Offered by Private Commercial Banks in Bangladesh - A Case Study On Modhumoti Bank LimitedSharmin Mehenaz TonneeÎncă nu există evaluări

- Financial Literacy and Money Management Among Tertiary Institution StudentsDocument11 paginiFinancial Literacy and Money Management Among Tertiary Institution StudentsJoulze Ann BartolabacÎncă nu există evaluări

- UntitledDocument485 paginiUntitledTowolawi AkeemÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Annuity QuestionsDocument6 paginiAnnuity QuestionsSankar Ranjan0% (1)

- Form - FR2046 - Selected Balance Sheet Items For Discount Window BorrowersDocument1 paginăForm - FR2046 - Selected Balance Sheet Items For Discount Window BorrowersPratus WilliamsÎncă nu există evaluări

- Module 2.2 - Bank Reconciliation and Proof of CashDocument24 paginiModule 2.2 - Bank Reconciliation and Proof of CashChelsea PagcaliwaganÎncă nu există evaluări

- Social Security How Benefits Are Calculated En-05-10070Document2 paginiSocial Security How Benefits Are Calculated En-05-10070bobinorlando0% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Pan-American International Insurance Corporation Nexgen UlDocument5 paginiPan-American International Insurance Corporation Nexgen UlesegarraÎncă nu există evaluări

- FTF 2023-02-04 1675555956991Document3 paginiFTF 2023-02-04 1675555956991Brayan Teodoro Santiago Pascual100% (4)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)